ECB pin action prompts more easing by Sweden s Riksbank EUR SEK bulls unimpressed

Pin action – the act of forcing pins upon each other in bowling, so that they continue to knock over other pins Beyond the obvious […]

Pin action – the act of forcing pins upon each other in bowling, so that they continue to knock over other pins Beyond the obvious […]

Pin action – the act of forcing pins upon each other in bowling, so that they continue to knock over other pins

Beyond the obvious negative impact on the euro last week, last Thursday’s ECB meeting and press conference is also having a “pin action” effect on Europe-dependent countries.

Earlier today, Sweden’s Riksbank announced its most recent monetary policy decision. While the central bank left its main interest rate unchanged at -0.35%, it did opt to expand its bond buying program by 65B krone to 200B and extend its expiration by 6 months until June 2016. In the accompanying statement, the Riksbank noted that “monetary policy needs to be more expansionary in order to underpin the positive development in the Swedish economy and safeguard the robustness of the upturn in inflation.” Beyond today’s changes, the Riksbank also reiterated that it was prepared to expand stimulus further, even between its scheduled meetings if necessary.

In retrospect, it’s easy to draw a line from the increasingly likely prospect of more stimulus from the ECB later this year to a more expansionary monetary policy in Sweden. After all, eight of Sweden’s nine largest export markets are in Europe, and many of those are members of the Eurozone. Meanwhile, headline inflation remains subdued at just 0.1%, while the country’s measure of “core” inflation is running at 1.0%, well below the central bank’s 2.0% target.

With the Riksbank’s QE program still modest by the current global standards at just 5% of GDP (by contrast, the ECB’s current program will be roughly 9% of the Eurozone’s total GDP), more easing could be coming down the pipeline, sooner rather than later.

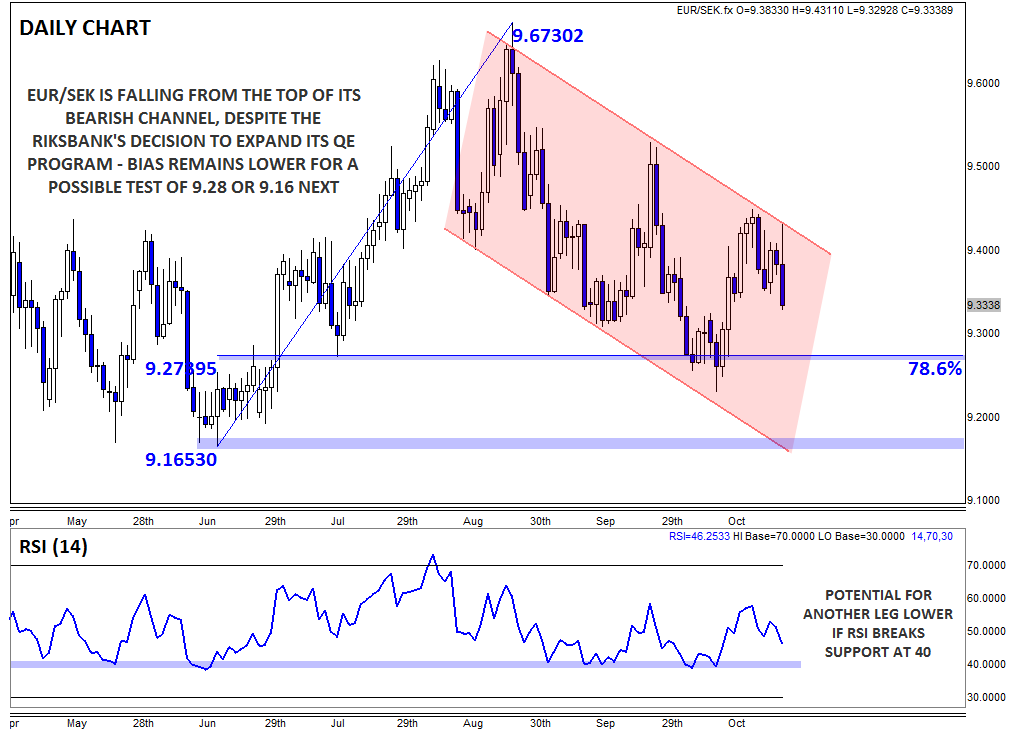

Technical View: EUR/SEK

Perhaps one of the most important drivers of the Riksbank’s decision was the fact that the Swedish krone has stopped depreciating against the euro. In the current slow growth, low inflation global environment, no country wants a strong currency, and the recent modest strength in the krone no doubt made Riksbank officials uncomfortable.

Unfortunately for them, traders have actually been buying the krone in the wake of the release, with EUR/SEK falling to 9.33 as of writing. The pair remains within a bearish channel off the late August high near 9.65, and rates may now have a date with previous support at the 78.6% Fibonacci retracement near 9.25. If that support level is broken, ideally accompanied by a breakdown in the RSI below its own support level at 40, a drop toward the 6-month low at 9.16 could be next. Only a break above the bearish channel (currently around 9.50) would shift the near-term bias back to neutral.