ECB it s time to focus on yields

The Greek parliament managed to pass a vote to agree to bailout reforms, albeit two hours after the deadline, but it now looks like a […]

The Greek parliament managed to pass a vote to agree to bailout reforms, albeit two hours after the deadline, but it now looks like a […]

The Greek parliament managed to pass a vote to agree to bailout reforms, albeit two hours after the deadline, but it now looks like a third bailout is in the bag for Greece. While there are still a few hoops to jump through to get the cash through to Athens, the immediate concern about another Greek default in the near term has significantly receded.

Greece still has many problems, it will take years, if not decades for confidence to return to the markets and growth to reappear. Some have called this a Pyrrhic victory for Germany and Greece’s creditors, but it actually looks like a fine victory for Angela Merkel and co. in my view, since they won’t have to pick up the pieces when this bailout expires in 3 years and another one is required.

Essentially, Greece is now on a three year cycle, which roughly corresponds with Europe’s political cycle. Short-termism has taken over, Greece is the new hot potato that Europe’s leaders want to throw to someone else as soon as possible.

Greece: the political hot potato in Europe

This leaves the ECB as the one constant in Greece’s life, as the IMF seems to work along similar political lines to the rest of Greece’s creditors. Today we hear from Mario Draghi at his regular ECB meeting. It has one of the most important jobs to do now that Athens has agreed to reforms: decide when the banks should re-open and capital controls lifted, it also needs to decide on re-capitalising Greek banks and whether or not to extend ELA funding in the coming weeks and months during this painful re-opening period.

The EUR remains doomed:

This is likely to be the focus of the ECB’s meeting, especially the press Q&A, since Greece is still such a big story. However, even positive news on Greece can’t save the EUR from more declines in our view. Essentially, with Greece so close to collapse, the ECB’s main job – to determine monetary policy, means that it is likely going to have to maintain a loose policy stance for some time to come.

This is an important development (even more so than Greece), as it highlights a schism in the major central banks’ policy stances. This week we have already heard from the BOE’s Carney and the Fed’s Yellen, who both hinted that a rate hike is likely. We expect Draghi to stand at the other end of the rate-setting spectrum, and maintain that rates will not rise for some time. Because FX is sensitive to monetary policy changes, it could have a major impact on the EUR.

Where could the EUR go next?

Just because Greece is out of the woods (a bridging loan has been agreed, which means that Greece will avoid default in the near term), does not mean that the EUR will rally. It has fallen to its lowest level during this latest crisis on the back of the Athenian agreement to reforms in return for bailout cash. A dovish Draghi is being priced into the EUR, and we think that there could be further to go.

Watch yields:

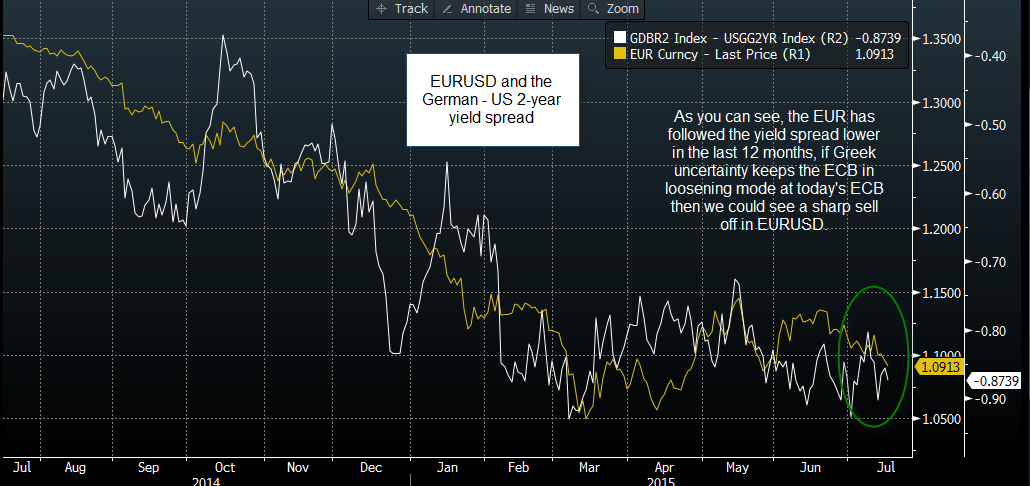

As you can see in the chart below, EURUSD moves in the same direction as the German – US 2-year bond yield. This is currently at -87 basis points, which is close to the lowest level since 2007. Although there is some policy divergence already priced in, we think the recent hawkish turn in Fed/ BOE communications could lead to even greater policy divergence and even more EUR weakness in the medium-term as the single currency is sold in favour of higher yielding currencies. Thus, figure two could continue to head south, falling to even more historic lows.

From a technical perspective, the EUR is looking extremely weak. We think that any bounce back to Thursday’s high of 1.0960 could trigger further weakness, support lies at 1.0880 and then 1.0820 – the low from end of May – in the short term. Below here opens the way to March/ April lows around 1.05.

Figure 1:

Source: City Index, Data: Bloomberg