ECB Drops Spread to 2008 Lows

The ECB slashes the lending-deposit rates spread to the lowest level since 2008 as an effort to lift emergency lending Today’s dual rate cuts (-25 […]

The ECB slashes the lending-deposit rates spread to the lowest level since 2008 as an effort to lift emergency lending Today’s dual rate cuts (-25 […]

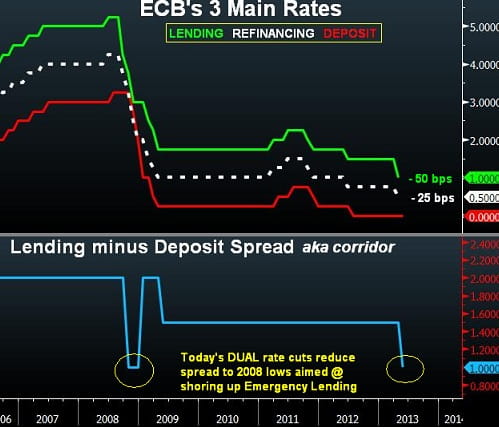

The ECB slashes the lending-deposit rates spread to the lowest level since 2008 as an effort to lift emergency lending

Today’s dual rate cuts (-25 bps in the refinancing rate to 0.50% and -50 bps in the lending rate to 1.00%) reduce the spread between the lending rate and the deposit rate to 1.0% from 1.50%.

The spread between the lending (emergency) rate and the deposit rates — known as the corridor rate– is now at its lowest since 2008 (Oct, Nov & Dec 2008), a time when the ECB rushed to reduce the cost of emergency loans (and catch up with the Fed’s aggressive easing) at the peak of the global financial crisis.

The ECB’s rate cutting decision targets the economy, rather than liquidity conditions, reflecting the decline in Eurozone CPI to 33-month lows (the biggest monthly point-drop since July 2009), the dual contraction in Germany’s manufacturing and services sectors, the seventh quarterly growth contraction in Spain as well a new record unemployment rate of 26.7% in the Eurozone’s fourth largest economy.

Today’s decisions focus on the banking sector, while any measures aimed at shorting up assistance to small & medium enterprises (SMEs) are likely to be taken in next month’s governing council meeting, which coincides with staff quarterly projections. By then, it would be clearer whether German GDP growth had posted a second quarterly negative decline, following the -0.6% in Q4 2012.

Euro: More Inaction

We expect further weakness towards the 1.2920-30 territory following the fourth failed attempt to follow up above the all-important 100-day moving average. The consolidation between $1.2850 and $1.3200 will likely prevail as the weakening position of the Fed hawks counters the loosening of austerity rules. Any prolonged declines are likely to encounter buying pressure at the important 1.2850s—the trend support extending from the low of July 2012.