Expectations are running high ahead of tomorrow's ECB monetary policy announcement. There seems little chance of Draghi quietly slowing down ahead of his departure in October. Instead all eyes will be on him to see if he can pull one last rabbit out of the hat and go out with a bang.

Expectations are for 10 basis point overnight deposit rate cut, with a sizable bond buying programme also on the cards. But are investors expecting too much? Anything short of these expectations could boost the euro.

What the data says?

The economic picture in the eurozone over the past few months has deteriorated. Eurozone GDP has slowed considerably to just 0.2% in Q2, down from a more solid 0.4% in Q1. Whilst employment and consumer consumption are holding up, the manufacturing sector is slumping.

PMI’s have languished below 50, the level that separates contraction from expansion for several months. Data from Germany, the once powerhouse of Europe, now more the Achilles heel, makes for grim reading. The manufacturing pmi has remained at 43 across several months, whilst industrial production continues to decline. Evidence is mounting that struggling manufacturers could tip Europe’s biggest economy into recession.

Inflation in the bloc, both headline CPI and core CPI have consistently missed the ECB’s 2% target.

The doves…

There is no denying that the picture is pretty gloomy. Weak growth, slumping manufacturing sector, subdued inflation have all increased expectations for looser monetary policy. Add into the picture Draghi’s comments from the last ECB meeting when he explicitly said that the central bank would act in September and Finland President Olli Rehn’s suggestion that the “stimulus package could overshoot investors expectations” and its easy to see why the markets are expecting a sizeable stimulus package and rate cut.

The hawks…

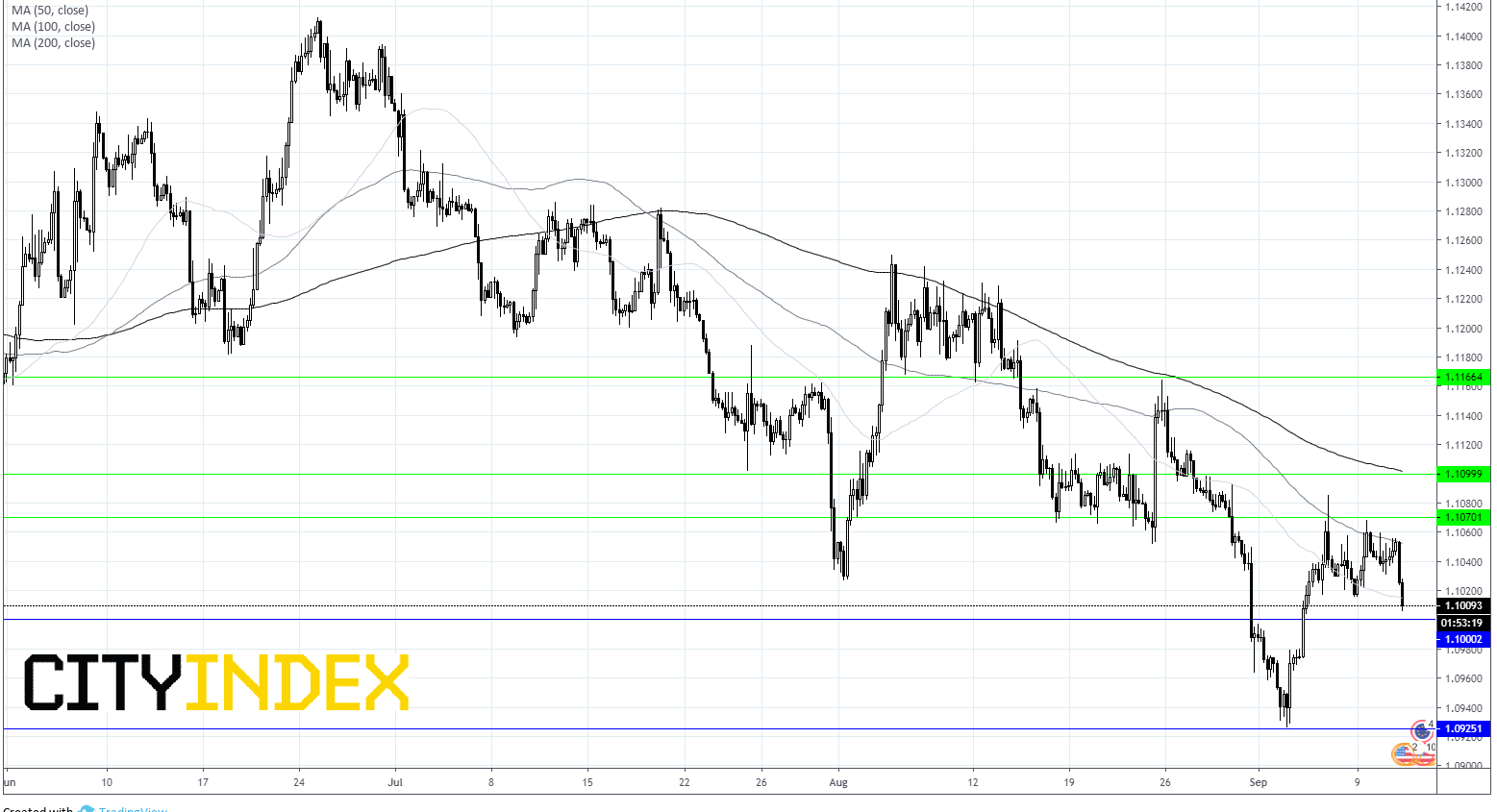

The EUR/USD is dropped 2-year lows, as expectations of heavy-handed stimulus was priced in. More recently the euro has edged cautiously higher as more hawkish policy makers have suggested that the markets’ forecasts have gone too far.

Expectations

Following the more hawkish comments the EUR/USD has liftedfrom the 2 year low and is pricing in a 10-basis point cut rather than 20 points previously expected.

The ECB are also expected to leave open the possibility of further cuts. Failure to do so could send the EUR surging back towards $1.11.

A deeper cut than 10 basis points and would exceed expectations and send the euro lower back toward last weeks’ two year low of $1.0926.

Regarding a new asset purchase programme, whilst some market participants believe the ECB will engage in a new programme this month, we expect Draghi to commit to restart in October with repurchases of €40 billion per month.

Conclusion

The euros reaction will depend on the depth of the rate cut, the commitment to do more and any mention of a bond buying programme. However, with so many dissenting voices in the ECB Draghi may struggle to deliver on such dovish market expectations potentially sending the euro higher.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Euro articles

April 2, 2024 03:02 PM

February 15, 2024 07:29 PM

January 4, 2024 07:14 PM

December 20, 2023 07:17 PM