EasyJet shares face profit taking after solid full year

EasyJet has done almost everything right this year judging by its full-year results out this morning. But the market is giving the figures a mixed […]

EasyJet has done almost everything right this year judging by its full-year results out this morning. But the market is giving the figures a mixed […]

EasyJet has done almost everything right this year judging by its full-year results out this morning.

But the market is giving the figures a mixed reception–shares have repeatedly dipped in and out of the red.

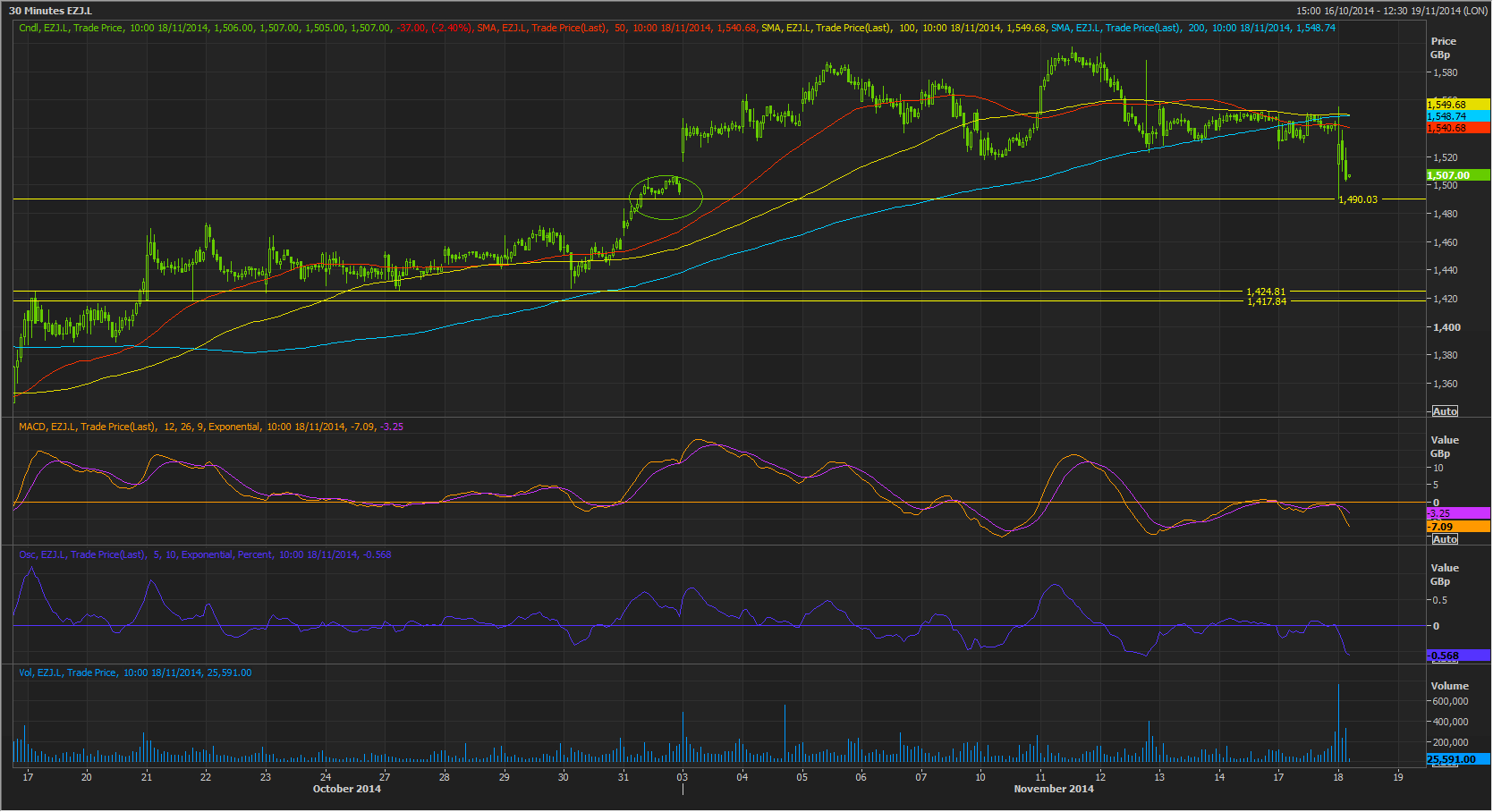

This needs to be put in context of a 26% rise from lows in August to a peak of 1550p last week.

A solid three-month stock advance along with a steady stream of positive news flow from the company since early autumn suggest the market was already well briefed about positive developments in the full-year.

Consequently, now is a reasonable time to take profits.

With daily momentum (see MACD and percentage price oscillator—the blue line) already inverting, it appears the active market came to a similar conclusion.

The airline has this morning met well-flagged expectations.

Almost everything is present and correct in these results—including total revenue per seat rising 1.2% (1.9% excluding currency effects) , load factor trending in the right direction and passenger numbers up a respectable 6.6%.

Even, so, the market will be aware of two mild-to-moderate sticking points.

Firstly, we note revenue per seat is forecast to be flat or just slightly higher excluding currency effects in the first half of next financial year.

This is possibly raising a few alarm bells—bearing in mind Ryanair has all but completed its turnaround plan in its bid to return to full-year profitability.

This comes after Ryanair this year gave a number of profit warnings and made it clear its former strategy of ‘low-cost at all costs’ (and tacit suggestion low-cost was favoured over quality) was no longer sustainable.

Ryanair said it would improve its much-criticised ‘customer service’ and that it planned to expand further into primary airports used by business travellers.

Such changes would align Ryanair more precisely in direct competition with easyJet, just as EZJ was attempting to narrow the gap between itself and its rival.

Air France-KLM and Lufthansa have also recently announced plans to compete more aggressively.

These factors, taken as a whole, raise the prospect of more concerted competition against easyJet from leaner and more battle-hardened rivals.

All this against a backdrop of currency and regional (AKA Eurozone) headwinds faced by EZJ and its peers in Europe.

With the strength easyJet has shown this year, there is little reason to expect its full-year 2015 operating performance to be any less solid, but it may be that the market is priming for a raised game from its rivals.

Potentially more troublesome for the stock today, we note, once again, there is no mention of the special dividend that was first announced a year ago.

The issue has evolved from a potential plus point, in terms of the EZJ investment case, into something of an ‘albatross’.

The airline first suggested it would pay a one-off dividend, totalling about £175m, in November 2013, but has mentioned little about the potential pay-out since.

Yes, the market will applaud easyJet’s recently bolstered dividend policy—especially now its average yield is well above Ryanair’s. (The Ireland-based airline does not have a pre-set dividend policy.)

However, pledging a special dividend and not delivering has created a little uncertainty, and perhaps, disappointment.

We think it is possible easyJet CEO Carolyn McCall may face questions about the special dividend during a conference call between management and analysts set begin at 11 this morning.

In the meantime, the stock is in a broad holding pattern, relatively close to October support, around 1490p.

Either way, the market seems inclined to sell from here and the next band of likely assistance appears to lie between 1417p-to-1424p.