EasyJet shares dumped on cost revelations

Updated 1200 BST EasyJet shares descended sharply at Tuesday’s open after the market looked past a rare profit the airline made during the traditionally fallow […]

Updated 1200 BST EasyJet shares descended sharply at Tuesday’s open after the market looked past a rare profit the airline made during the traditionally fallow […]

Updated 1200 BST

EasyJet shares descended sharply at Tuesday’s open after the market looked past a rare profit the airline made during the traditionally fallow first-half season and focused instead on easyJet’s caution on third quarter revenues.

The second-largest budget airline in Europe said it expected a negative impact from disruption to flights in April from air traffic control strikes in France which caused it to cancel about 600 flights.

This would trim £25m from pre-tax profit, easyJet said this morning.

With full-year pre-tax profit forecasts currently pointing to £681m, a £25m hit would still leave underlying earnings just under 13% ahead of the year before.

Could there perhaps be an added magnitude of punishment being meted out to easyJet this morning beyond that warranted from its revenue warning?

After all, the shares have traded as much as 9% lower on Tuesday, slashing over £600m off EZJ’s market capitalisation, whereas on the face of it, the net effect of a £25m hit should be little more than the stated amount.

We notice the airline released a brief statement containing passenger stats last Thursday, the date of the UK election.

The statement did not appear to have been scheduled more than a week in advance.

It said in the statement that cancellations in April spiked enormously to 602 compared with April last year, when just 48 flights were called off.

The cancellations last month were “largely” due to air traffic control strikes in France, the airline said.

Investors will also have in mind that the benefit from fuel prices easyJet enjoyed from the second half of last year when oil prices reached multi-year lows, will soon tail off.

The oil price has since recouped some of last year’s loss, although the airline still stated this morning that its 12-month fuel bill would decrease by £95m to £120m.

The airline noted that full-year fuel cost ‘effects’ are expected to lead to a rise of 2.5%.

On the currency front, the news was slightly negative too. easyJet said it expected an additional £20m negative impact from adverse exchange rates.

Finally easyJet warned of a potentially higher bill from increased ‘navigation’ charges—AKA costs payable to Eurocontrol, the regional air traffic management service. The airline is currently disputing the increased charge, but if it fails to avoid the increase the impact on the full year could be £12m.

Whilst the diminishing fuel advantage will flatter the current year, the underlying impact of the above additional costs could leave the final tally for fiscal 2015 a much more modest £644m, barely 11% higher year-on-year, and in fact just an implied 7.4% higher, including the estimated currency effect.

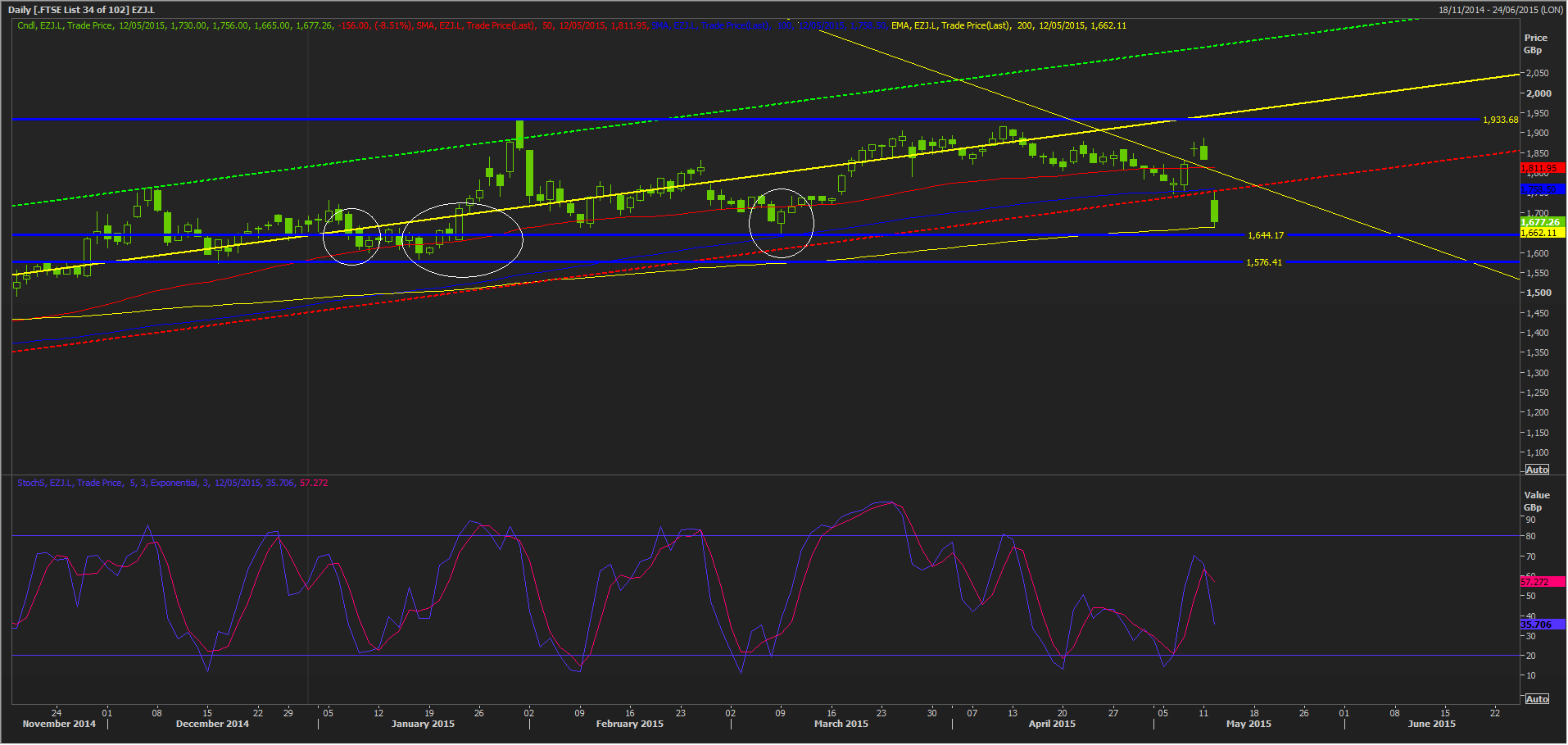

The stock could certainly have been prone to a correction of the kind seen today given that it was still less than 14% below its all-time high reached in January, and had added 47 percentage points more than the FTSE 100 in the last 24 months.

The airline taking a somewhat indirect route as regards apprising the market of its latest views on the costs situation has in the event been a ready excuse for investors to take some profit.

In an effort to defray this unforeseen squall of rising cost, easyJet announced on Tuesday it would modify its fleet of Airbus Group NV A320 jetliners to pack 186 passengers on each plane, six more than it does right now

It won’t make these modifications before May 2016.

Therefore a 2% reduction in per seat costs will not benefit revenues before estimated completion in the summer of 2018.

On balance, these underlying negatives take quite a bit of the shine off EZJ’s half-year achievements.

These include that it’s edged the bar slightly higher against its only true rival, Ryanair with a 70 basis point extension of its load factor lead to 89.7% vs. RYA, which was on 88% in December

EZJ has now maintained an average passenger yield advantage against its rival for almost every interim period since 2012.

Additionally, EZJ’s earnings landing in the black for the first half bodes especially well for the rest of the financial year, providing the best possible chance that its cost initiatives can forestall at least some of the hit and enable the airline to post a net profit rise.

Given the increasingly marginal advantages between the pair, I expect competition between the two to hinge more and more on their capability to select astute price inflection points in which to invest.

In that respect, spare ‘cash’ capacity could be an important final denominator.

Consensus places Ryanair’s free cash flow yield at 4.9% for the current year, versus 2.3% for easyJet.

However, for the next fiscal year beginning in September 2016, easyJet is expected to begin to edge ahead of RYA on the strength of its free-cash flow—EZJ FCF yield is seen at 3.2% whilst RYA’s is expected to slip to 3%.

None of this helps easyJet’s shares today.

The stock almost certainly has comfortable scope to fall further, toward more visibly durable support, implying 1644p, taking the loss on the day to more than 10%.

But given evident underlying operational momentum—including in flights, passenger yields, cost initiatives and a natural lead over Ryanair—which is arguably still in a recovery phase following significant difficulties two year ago—I regard EZJ as being in a consolidation phase, after which it will attract more conviction buyers.