Following a late rebound on Wall Street and a rise in Asian stocks overnight, European bourses are heading towards a stronger start on the open. Investors are taking stock of the gradual reopening of economies whilst oil also picks up on greater fuel demands.

Optimism surrounding the gradual easing of lockdown restrictions and the impending economic recovery is outweighing rising US – Chinese tensions, which had dragged on sentiment in trading on Monday.

Italy and Spain are gradually reopening their economies, Germany is moving towards the second phase with large shops set to reopen, joining smaller shops which have already started trading. In the UK, blueprints of how Britain will ease out of lockdown have also been leaked, although more details are expected from Boris Johnson later in the week.

Oil back over $20pb

The rebound in oil has been largely driven by an increase in demand as governments ease lockdown restrictions. Data from the Cushing storage (largest oil storage tank in the world, responsible for 13% of total US storage) showed inventories rose 1.88mb last week, the smallest increase since mid-March and the surest indication that oil demand is slowly picking up.

The rebound in oil has been largely driven by an increase in demand as governments ease lockdown restrictions. Data from the Cushing storage (largest oil storage tank in the world, responsible for 13% of total US storage) showed inventories rose 1.88mb last week, the smallest increase since mid-March and the surest indication that oil demand is slowly picking up.

Whilst April was all about the collapse of demand and approaching storage capacity limits, expect May and June to be about rising demand and rising storage capacity as more oil is consumed. As economies reopen demand will gradually pick up. However, any rapid bounce back is looking highly unlikely, this will be a gradual advance, unless OPEC+ manages to pull together another production cut.

Attention will now turn to tomorrow’s API data and then EIA data, which could well confirm that a gradual recovery is underway.

Attention will now turn to tomorrow’s API data and then EIA data, which could well confirm that a gradual recovery is underway.

Service sector PMI bottom

The pound is pushing higher, snapping a three-day losing streak against the Dollar as the number of coronavirus daily deaths fall to levels last seen at the end of March as the UK awaits further details on the UK’s exit strategy.

Today the service sector PMI is expected to drop to 12.2 in April (final), reflecting a full month of lockdown. The very measures implemented to slow the spread of covid-19 caused services sector demand to evaporate. With the UK economy set to gradually reopen this should represent a bottom. With the market expecting a horrifying number, its unlikely to rock the boat much at these levels. A significantly worse reading (if possible?!) could.

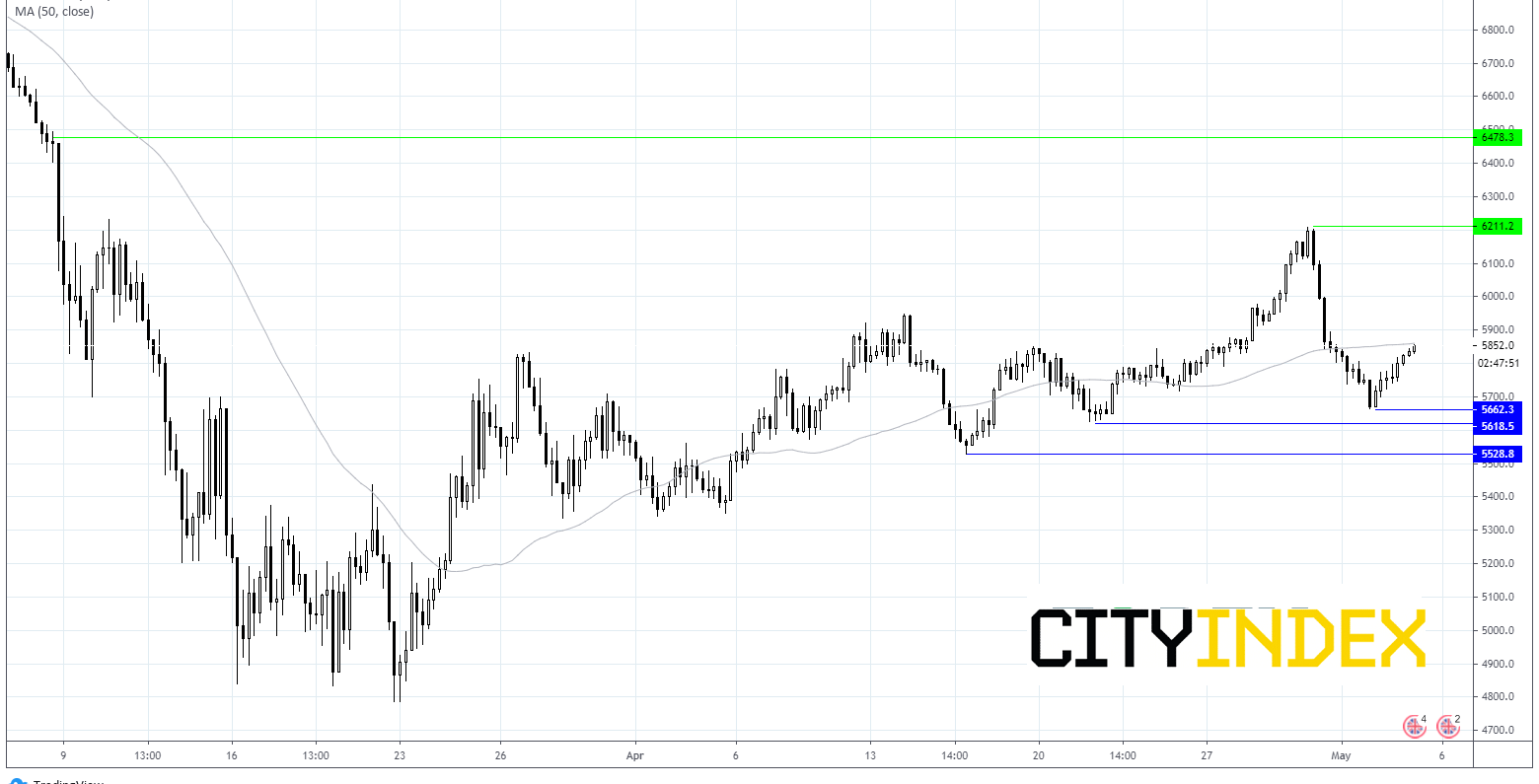

FTSE chart

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Indices articles

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM