Draghi 8217 s Hand Forced by Mr Market

Regardless of whether the ECB has already decided on cutting interest rates this Thursday, ECB President Draghi now has little choice. In fact, Draghi is […]

Regardless of whether the ECB has already decided on cutting interest rates this Thursday, ECB President Draghi now has little choice. In fact, Draghi is […]

Regardless of whether the ECB has already decided on cutting interest rates this Thursday, ECB President Draghi now has little choice. In fact, Draghi is now forced by the markets to deliver a modest 25-bp rate cut in the refinancing rate to 0.50%.

Why would the ECB use up the last of its monetary policy armoury at a time when the impact of such action on shoring the beleaguered Eurozone economy may be minimal at best?

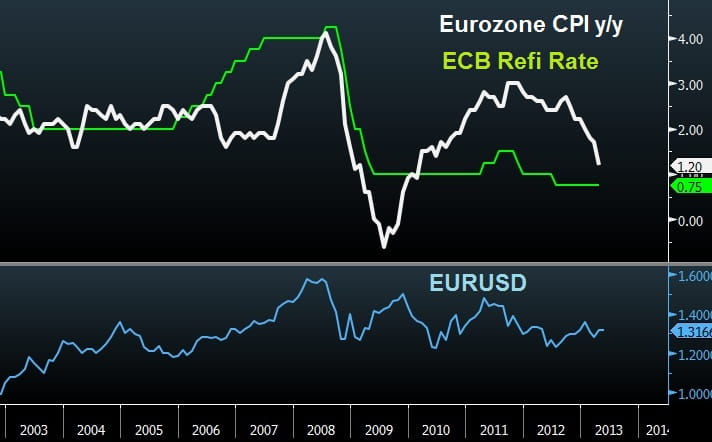

The unexpected dual contraction in German manufacturing and services sectors as well as a decline in Eurozone April annual CPI to 33-month lows (the biggest monthly point-drop since July 2009) are sufficient reasons. Recent data showing the 7th quarterly growth contraction in Spain as well a new record unemployment rate of 26.7% in the Eurozone’s 4th largest economy are also backing action from the ECB.

Contrasting Macro-Market Divergence

Despite the aforementioned corrosion in the Eurozone economy, market metrics have gone from good to great. Spain & Italian 10-year yields at 3-year lows, German bourses near 5-year highs and the euro has risen in 8 out of the last 12 months. The fall in sovereign yields may be among Draghi’s greatest accomplishments since taking the helm at the central bank 2 years ago. Such was a tremendous challenge as Italy attempted to issue bonds at a time when Italian banks were bleeding capital and the government faltered in pursuing austerity. Incomplete austerity policies and failed governments could not lift bond yields back above the danger territory of 7%. All of this due to Draghi’s commitment to save the euro with a yet untested program of Outright Monetary Transactions.

The contrast between stable market metrics and recession-stuck Eurozone offers little choice to the ECB but to opt for the rate cut route instead of the LTRO alternative. A 25-bp cut may be insignificant, but failure to cut would disappoint 80% of market participants expecting a rate cut, which may trigger a fresh euro rally to the detriment of the already struggling Eurozone, including a recession-bound Germany.

A Draghi rate cut would be more tactical than macroeconomic.

That is especially the case considering the FOMC will most likely downgrade its economic view and put to rest all speculation of tapering QE before year-end. A dovish Fed on Wednesday will have to be followed by a dovish ECB on Thursday.

There is an unfolding reality about to hit the hawks at the Fed. Not only the US central bank will not taper off its $85 bn in monthly purchases any time soon, but in fact, it may expand asset purchases.