Dovish BOE comments decent US GDP GBP USD 1 50

In an otherwise quiet day in the foreign exchange market, GBP/USD has seen a relatively big drop amidst dovish comments from BOE policymakers and decent […]

In an otherwise quiet day in the foreign exchange market, GBP/USD has seen a relatively big drop amidst dovish comments from BOE policymakers and decent […]

In an otherwise quiet day in the foreign exchange market, GBP/USD has seen a relatively big drop amidst dovish comments from BOE policymakers and decent US data.

During this morning’s European session, BOE Chief Economist Andy Haldane posted an annual report with his views on the Bank of England’s website. In those comments, Haldane highlighted that the risks to growth and inflation were skewed to the downside and crucially, that the Bank of England should be poised to either increase or decrease interest rates depending on how the data plays out. Of course, with most traders anticipating that the BOE will raise interest rates at some point next year, the suggestion that a rate cut could still be in play led to a kneejerk reaction lower in the pound.

In case you’re not intimately familiar with the ideological leanings of all the world’s central bankers, it’s worth noting that Haldane tends toward the dovish side of the spectrum, so these comments weren’t too out of character, but they were given more significance by an apparent dovish shift from BOE Governor Mark Carney in his speech to Parliament a few hours later. Dr. Carney sounded particularly vague about the timing of any interest rate increases, a dramatic change from comments a few months ago implying that the timeframe for tightening would become “come into sharper focus” by the end of this year.

GBP/USD bulls’ woes were exacerbated by decent data out of the world’s largest economy as the US came online. The just-released “preliminary” Q3 GDP figure came out at 2.1%, a tick above the 2.0% reading anticipated and well above last month’s initial estimate of 1.5% growth. Though the headline figure was slightly better than anticipated, the most important and sustainable component of GDP, personal consumption, was actually revised lower to 3.0% vs. 3.2% initially estimated. Like many US economic reports of late, today’s GDP reading is unlikely to meaningfully tip the scales for the Federal Reserve, which still appears on track to hike interest rates next month for the first time in nearly a decade.

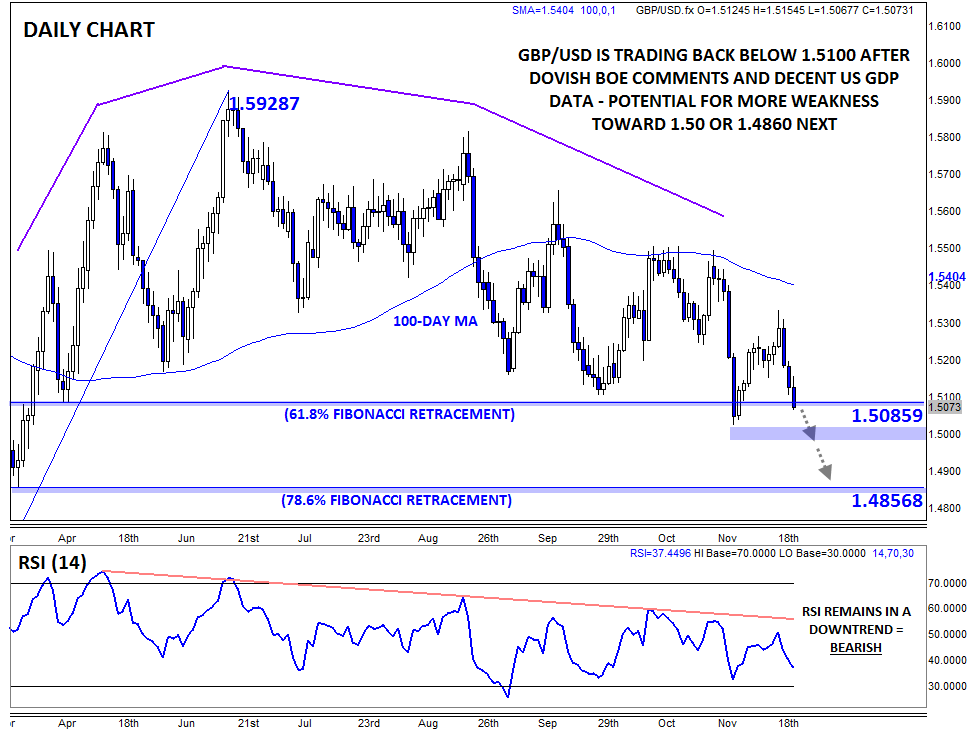

Technical View: GBP/USD

As we noted above, GBP/USD has been on the back foot so far today, with rates dropping through the 1.5100 handle earlier this morning. In addition to the longer-term rounded top pattern we noted last week, cable is now edging below 61.8% Fibonacci support at 1.5085. Moving forward, emboldened bears may look to target the psychologically-significant 1.50 level, which would represent a 7-month low for the pair, followed by the 78.6% Fibonacci retracement at 1.4860.