August 13, 2019 2:30 AM

A tough start to the week as the S&P 500 sagged by 1.2% overnight, under the pressure of U.S.- China trade tensions, rising geopolitical concerns in Hong Kong and the threat of an “80’s” style South American debt crisis.

While concerns over Hong Kong eased this morning after the airport re-opened, it appears another debt crisis is seemingly inevitable in Argentina after the left-wing populist opposition candidate dominated Sunday’s primary election vote.

Markets quick to interpret this as a rejection of incumbent Conservative President Marci’s austerity measures, as the Argentinean currency, USD/ARS plunged by 30% overnight. A move in line with the devaluation that occurred during the Argentinian default of 2001.

With an eye also on the past, Argentinian credit default swaps are pricing in a 75% chance of a sovereign default. Due to Argentina’s strong linkages to other Latin American countries and keen to avoid another credit event, it is likely the IMF will step in as they did in 2001 and in 2014 to contain the damage before any real spill over occurs.

In the meantime, markets are left to work out the ramifications of the main game in town, which is the ability of global Central Bank easing’s to offset the impacts of the trade war-inspired global slowdown. Goldman Sachs the latest to predict a bigger hit to global growth from the trade war than originally expected and as a result, have revised down their U.S. Q4 GDP forecasts by 0.2% to 1.8%.

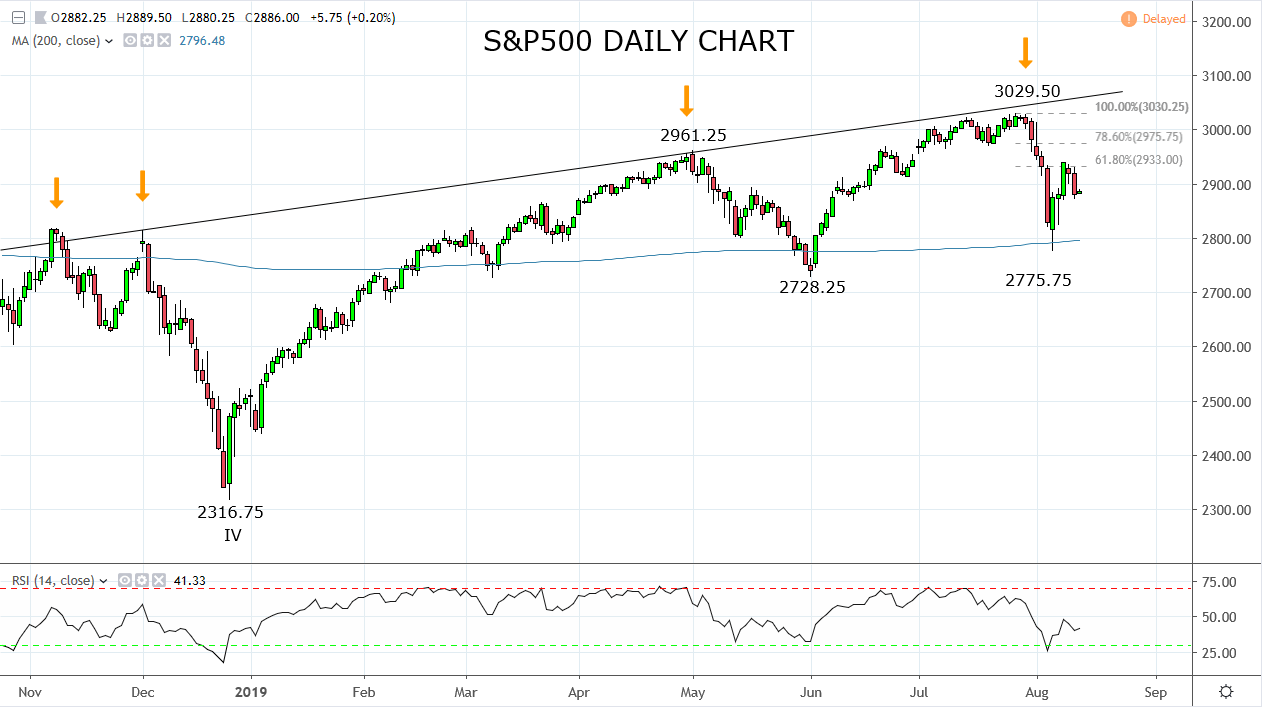

For equities this isn’t good news although it does fit with the technical view outlined in our last S&P500 update here https://www.cityindex.com.au/market-analysis/sp500-stalls-as-rate-cut-debate-continues/ which highlighted the potential for the critical 3030/3050 resistance area, to become a medium-term high.

The overnight fall, therefore, is in line with the view that a pullback of sorts is underway. However, whether the S&P500 continues to fall directly from here on in or has more sideways price action to complete ahead of a move towards 2730 remains to be seen.

In short, we remain with a bearish bias for the S&P500, leaning against the 78.6% Fibonacci retracement level at 2976. A close above 2976 would require a shift to a more neutral stance.

Source Tradingview. The figures stated are as of the 13th of August 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Disclaimer

TECH-FX TRADING PTY LTD (ACN 617 797 645) is an Authorised Representative (001255203) of JB Alpha Ltd (ABN 76 131 376 415) which holds an Australian Financial Services Licence (AFSL no. 327075)

Trading foreign exchange, futures and CFDs on margin carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange, futures or CFDs you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss in excess of your deposited funds and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange, futures and CFD trading, and seek advice from an independent financial advisor if you have any doubts. It is important to note that past performance is not a reliable indicator of future performance.

Any advice provided is general advice only. It is important to note that:

- The advice has been prepared without taking into account the client’s objectives, financial situation or needs.

- The client should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation or needs, before following the advice.

- If the advice relates to the acquisition or possible acquisition of a particular financial product, the client should obtain a copy of, and consider, the PDS for that product before making any decision.

Latest market news

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM