The dollar has gained some bullish momentum against her weaker rivals over the past few days because of recent strength in US data. But given the 100% probability of a rate cut in July (according to the CME’s FedWatch tool), this means the dollar rallies could be sold, especially as the likelihood of a 50 basis point trim has risen to over 30% once again after it took a tumble in the aftermath of the US jobs report a couple of weeks ago.

Investors are clearly worried that the ongoing trade standoff between the US and China may hurt economic growth and require a looser monetary policy now rather than later. This is, in fact, something many Fed officials have tried to emphasise on, including Chairman Jay Powell. Indeed, Dallas Fed President Kaplan, who just a few weeks ago had argued against an immediate rate cut, has said he is now open to a “tactical adjustment” in the form of a “modest, restrained, limited move.” Rate cut calls will only grow when you have a President who has a very aggressive negotiation tactics. Donald Trump warned that: “We have a long way to go as far as tariffs where China is concerned… We have another $325 billion we can put a tariff on.”

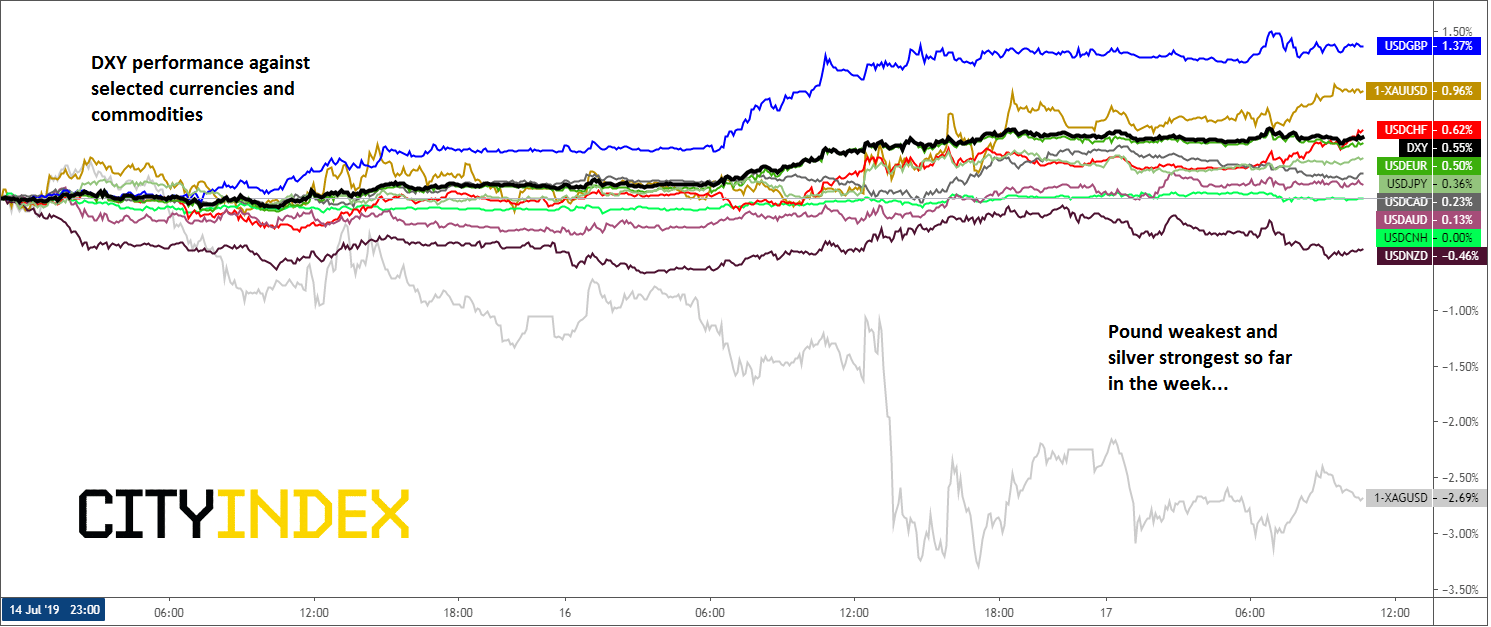

Meanwhile, recent US macroeconomic pointers such as employment, inflation and retail sales have not been too bad – in fact, better than expected – and the Dollar Index has responded positively. But the fact that traders are still 100% confident that a rate cut is forthcoming on the last day of this month, the greenback has not been able to move north against every currency or commodity. It has obviously performed well against the likes of the pound, which has been hit hard by rising fears over a no-deal Brexit, while the euro has huffed and puffed but essentially remained near the recent lows sub $1.13. But the commodity dollars, franc and yen have done much better against the buck, although even these look to have hit a ceiling for the time being.

However, as mentioned, the US dollar could struggle to sustain its recent rebound because of investors’ conviction about falling interest rates in the US. If so, it will most likely be the likes of silver and commodity dollars where we could see the greenback struggle the most against – especially if the upcoming publications of Canadian CPI (today) and/or retail sales (Friday), or Aussie jobs (early Thursday) manage to beat expectations. So, the USD/CAD and AUD/USD are the majors to watch, along with silver.

Source: Trading View and City Index

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM