Dollar resumes slide on weak data cautious Fed

After the Federal Reserve kept US interest rates unchanged as expected on Wednesday and reiterated its consistently cautious stance with regard to future rate increases, […]

After the Federal Reserve kept US interest rates unchanged as expected on Wednesday and reiterated its consistently cautious stance with regard to future rate increases, […]

After the Federal Reserve kept US interest rates unchanged as expected on Wednesday and reiterated its consistently cautious stance with regard to future rate increases, annualized Advance GDP data for Q1 came out on Thursday morning that disappointed already-low prior estimates. In the first quarter of the year, the US economy was estimated to have grown by only an annualized 0.5% against prior expectations of 0.7% growth.

Although this is only the first of three GDP reports, and there may well be revisions, the low Advance GDP estimate on Thursday underscores the Fed’s concerns about significantly slowing economic growth that has helped to deter further rate hikes since December. This report also exacerbates other weaker-than-expected economic numbers that were released earlier in the month, including key inflation price indices, retail sales, manufacturing, durable goods orders, and consumer confidence. Outside of a relatively strong US labor market, these indications of softness in the economy have helped contribute to sustained dovishness from the Fed and are weighing heavily on the US dollar.

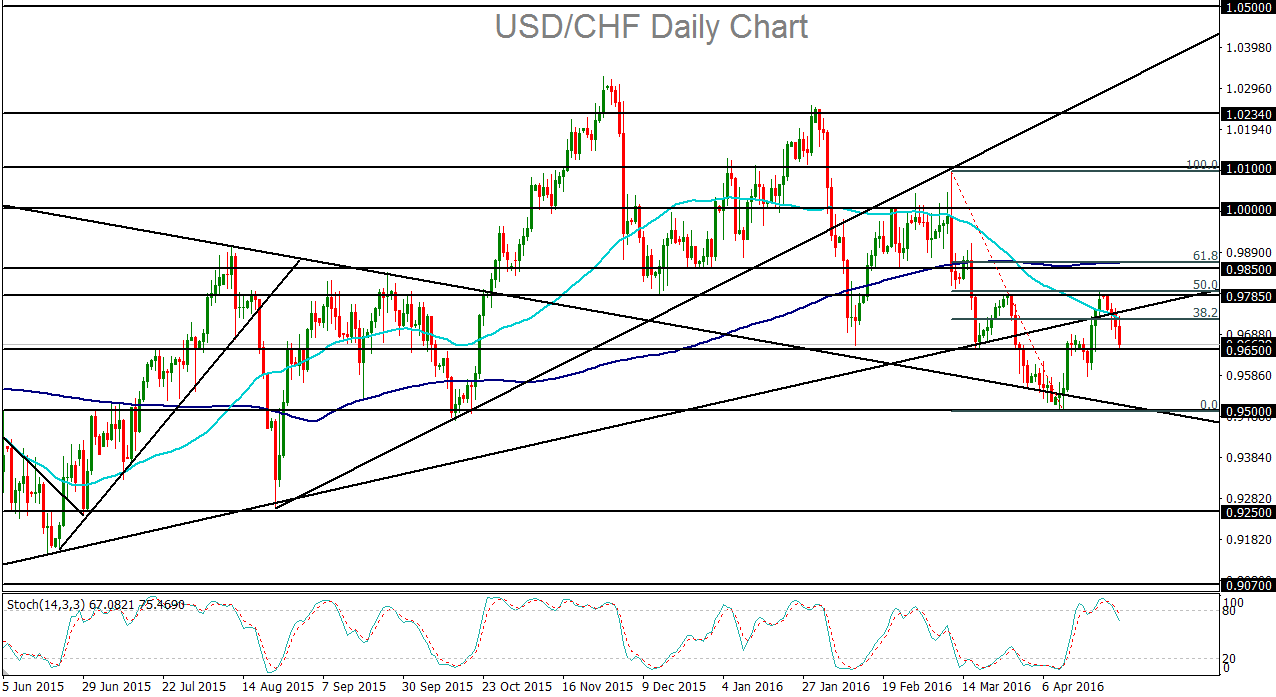

For the USD/CHF currency pair, this pressure on the dollar has resulted in an extended retreat from major resistance. At the start of the current trading week, the retreat began at a critical level for USD/CHF, turning the currency pair down right around the key 0.9785 resistance area, which is also around the 50% retracement level of the last major bearish run from March’s high to April’s low. That price level has served as a major support and resistance area since late 2015. From a slightly longer-term technical perspective, USD/CHF has been in a general decline since December, printing consistently lower highs and lower lows as the dollar has suffered from an increasingly dovish Fed after December due to continued weakness in economic conditions and inflation.

As noted, despite other areas of economic weakness, the labor market continues to show strength as a bright spot in the US economy. On Thursday, weekly unemployment claims come in generally as expected at 257,000, which is near 40+ year lows. Next week, the potentially critical Non-Farm Payrolls employment data for April will be released. Although its effect may be muted given the softness in other areas of the economy, it could still provide some surprises that could move the dollar significantly.

With continued bearish momentum on the current USD/CHF retreat, the next major downside target is at the 0.9500 support area, which is the level of April’s lows. In the event of a further breakdown below 0.9500, a continuation of the medium-term downtrend will have been confirmed, with a further downside target around the 0.9250 support area.