Dollar Index points to further weakness for greenback

The dollar has had a volatile few days. Following the publication of the poor monthly US jobs report on Friday, it initially fell sharply before […]

The dollar has had a volatile few days. Following the publication of the poor monthly US jobs report on Friday, it initially fell sharply before […]

The dollar has had a volatile few days. Following the publication of the poor monthly US jobs report on Friday, it initially fell sharply before rebounding equally strongly – most notably against the yen. The USD/JPY’s v-shaped recovery can be explained away by the positively-correlated stock markets which have rallied significantly on hopes that the Federal Reserve will now delay raising interest rates until at least the start of next year in order to support the weakening economic recovery. The Bank of Japan’s decision to keep its policy unchanged overnight has disappointed a few people and this has halted the USD/JPY’s rally for now. The dollar’s performance against the euro and the pound has been mixed, though it has dropped sharply against some emerging market and commodity currencies, with the latter helped by a rallying price of oil and gold.

Taking everything into account, the Dollar Index – which is a measure of the value of the greenback relative to a basket of foreign currencies – has weakened slightly since Friday’s jobs data, which makes sense. It has been driven lower by the firmer EUR/USD in particular which carries a 57.6% weighting. Other currencies such as the Japanese yen (13.6%) and the British pound (11.9%) are also applying some pressure as they also make up a significant portion of the index. If the recent trend of weaker US macroeconomic data continues then the dollar could fall further as the market pushes rate hike expectations further out. Unfortunately, there won’t be much in the way of US data today but tomorrow we will have the FOMC’s last meeting minutes to provide us some direction about the timing of the first rate rise. That being said, the meeting was conducted before those poor jobs numbers were released and several policymakers have already spoken since, delivering mixed messages. Thus traders should take the minutes with a pinch of salt, especially if they convey a hawkish message. However if the Fed was already dovish at its September meeting, they will have likely turned even more dovish now. So the dollar’s likely negative reaction may be amplified tomorrow if we see some eye catching dovish remarks from the minutes.

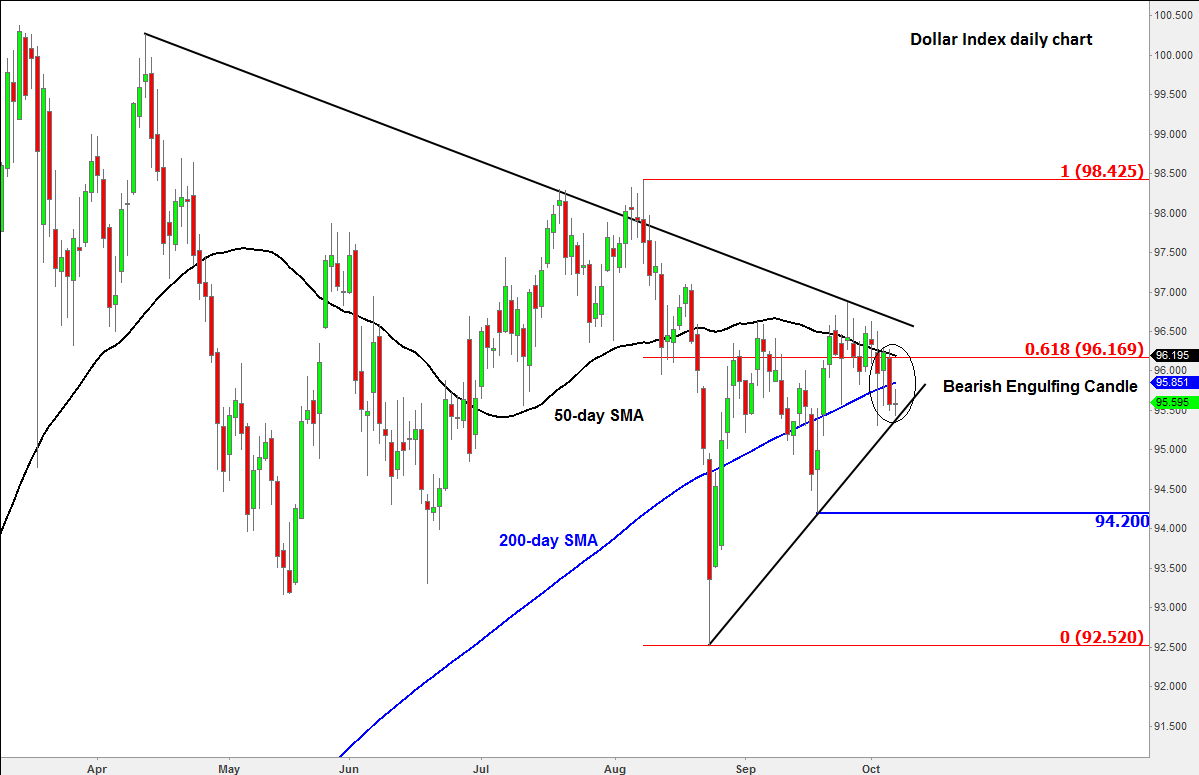

Meanwhile from a technical point of view, the Dollar Index found strong resistance yesterday from a key resistance area around 96.15/20. As can be seen from the chart, this where the 61.8% Fibonacci retracement level of the last downswing converges with the 50-day moving average. As a result of the sell-off, the Dollar Index formed what looks like a bearish engulfing candle on its daily chart and also closed below its 200-day moving average. The bearish engulfing candle suggests there was a shift from buying to selling pressure yesterday and points to further weakness. So far however there has been little or no follow-through in the selling pressure, possibly because traders may be wary of a bullish trend line that comes in just below these levels, around 95.00.

But if this trend line breaks down then a sharp sell-off could get underway. There is little further support seen until 94.20 ahead of the August low at just above 92.50. Meanwhile if the bulls manage to defend their ground here, they will still not be out of danger completely for as long as the downward-sloping trend line, which comes in around 96.50, remains intact.