Store closures and easing credit book key to survival

Dixons Carphone is the latest barometer of Britain’s painful retail industry as it transitions to new consumer patterns and online purchases. There’s little doubt things remain ugly. Shares in the mobile phones and electricals store plummeted as much as 28% on Thursday, their biggest one-day drop since 2017. The £1.27bn group warned of “significant” losses in the phone business. It’s an echo of issues that emerged around two years ago tied to consumers upgrading handsets less often and shifting to cheaper contracts.

This time, the impact is expected to drag annual pre-tax profits some 30% below market forecasts to about £210m. That comes after Dixons reported 2019/20 core earnings largely in line with sharply reduced expectations. It aims to deal with consumer market changes by renegotiating contracts with mobile operators. It is also some way through a savings programme that will unify more branded stores, with 39% of standalone Dixons Carphone stores less than a mile from a branch of a 3-in-1 Megastore format.

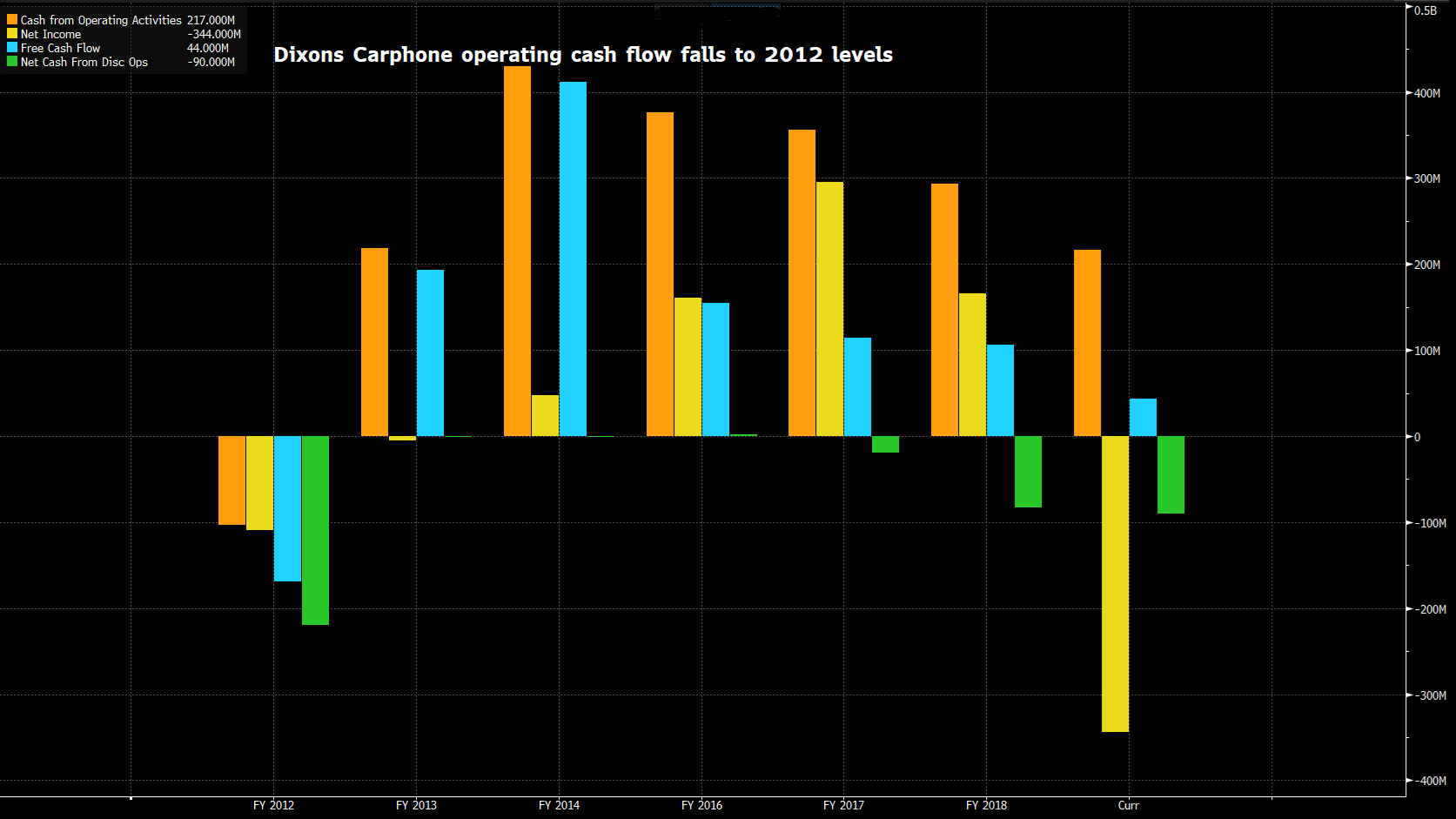

The group sees results improving over the next two years. Quantification of the extent of continuing challenges has actually been well-received by investors. By the middle of the UK session, the stock traded about 8% lower, 20 percentage points higher than its initial collapse. Some of this has an eye to the gruelling decline of around 73% the shares suffered over the last three years. Dixons is also differentiated from a host of troubled high street retail stories by cash. To be sure, cash from continuing businesses fell to £217m from £293m over the last financial year, in line with the biggest net income retreat in 10 years.

Dixons Carphone – cash from operations/free cash flow - 2012-2019

Source: Bloomberg

But the removal of cash flow from closed businesses over the financial year was the most since 2012. With cash generation back to around 2012 levels and the road to recovery still a long one, it’s too early to guarantee Dixons can avoid the fate of Debenhams, Maplin’s, Toys R US and others. For one thing, it will soon need to extend its cost savings programme from the current target of £200m, which now seems insufficient. But brand integration and the eventual run off of an £800m debtor book should be key to a projected £1bn cash flow over 5 years. Execution won’t be pain-free, including for the shares. Yet the prospect of success means Dixons is down though not yet out.

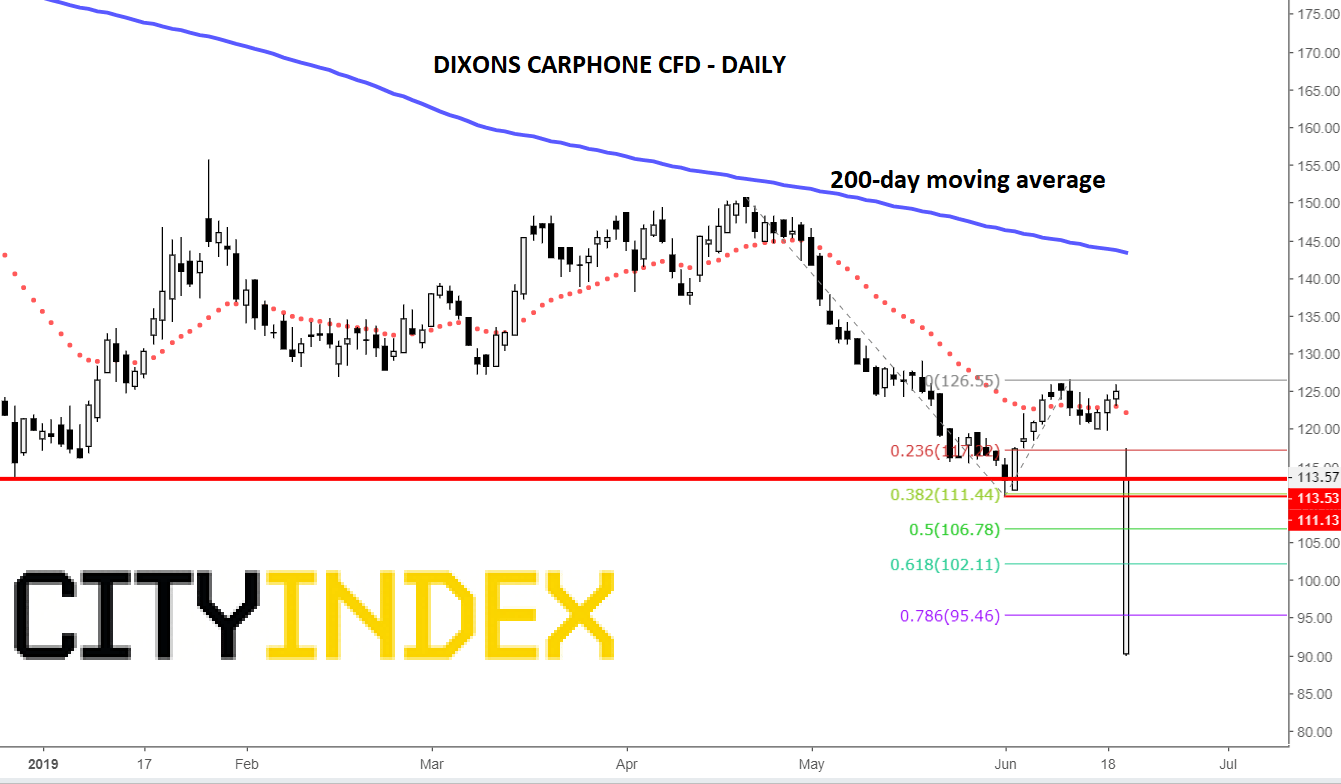

Chart thoughts

DC has now broken below December 2018 floors, which at the time represented the lowest prices in about five years; certainly the weakest since the group was formed by a merger of Carphone Warehouse and Dixons in 2014. In short, the stock has dipped into uncharted territory, bottoming just below 90p. Fibonacci principles map 95.5p. 102p, 106.8p and 111.4p as sensitive. Well the shares sprang back above the 113.5p December low later in the session. A close above is now crucial as theoretical supports aren’t guaranteed.

Dixons Carphone CFD – daily

Source: City Index

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM