Dixons Carphone shares may need a rest despite barnstorming sales

Dixons Carphone kept its cool during the Christmas sales while many retail rivals lost theirs, and the FTSE’s biggest consumer electronics chain was rewarded with […]

Dixons Carphone kept its cool during the Christmas sales while many retail rivals lost theirs, and the FTSE’s biggest consumer electronics chain was rewarded with […]

Dixons Carphone kept its cool during the Christmas sales while many retail rivals lost theirs, and the FTSE’s biggest consumer electronics chain was rewarded with best-in-class results.

The group, which is the result of a merger between two UK high street names completed last year, said sales at stores open over a year in the nine weeks to 3rd January, were 7% higher than the same period a year before.

This has enabled the company to edge up forecasts of the total profit it expects to make in its current financial year which ends in April.

The firm now expects pre-tax profit of £355m-£375m for 2014-15, compared to previous guidance of £354m.

Additionally, Dixons Carphone’s confident showing last year looks set to enable targeted £80m synergies to be realised a year earlier than planned.

Gross margins during the all-important Christmas retailing season were steady, the firm said, a not very oblique reference to how a number of retail peers had over-reached themselves at Christmas—largely with big discounts that trashed margins.

Still Dixons Carphone’s CEO, Sebastian James, noted the company had not escaped the perils of Christmas pricing pressure entirely.

“There is no doubt that the huge scale and success of our Black Friday promotion impacted the three weeks that followed”, he said.

However, he added that “customers respond positively to the deals that we had on Boxing Day where we saw growth from our record-breaking numbers last year in both the UK and Nordics. Our availability, pricing, service and marketing were all achieving very strong performance and customer metrics, and this translated into growth in market share in all our key territories over the period.”

Still, the group’s Chief Financial Officer, Humphrey Singer, conceded this morning in response to a media query that “Black Friday was bigger in sales terms than Boxing Day”.

That’s a potential admission that higher volumes were concentrated on a day of lower-margin revenues.

Like-for-like sales in DC’s flagship UK & Ireland division, where it also trades as Currys and PC World, were up 8%, topping consensus forecasts calling for a rise of 5%.

Same-store sales also rose in its northern Europe division, by 6%, versus market forecasts of 3%.

Sales in the more economically troubled southern half of Europe though, fell 4%.

The market has reacted in mixed fashion to DC’s sales figures.

The stock advanced as much as 4% earlier on Wednesday, but has since lost most of those gains.

It traded about 0.7% in the black as this article was going live, having dipped into the red for a spell.

Despite DC’s outstanding performance over Christmas, it looks like investors are still ambivalent about prospects for the stock after it was the top FTSE 100 performer of last year.

DC does lead its peer group on many metrics.

For instance, the market likes DC for growth more than Argos-owning Home Retail Group, with Home Retail rated on a 15.5x forward price/earnings ratio (the same as the peer group average) against 16.9 for Dixons Carphone.

But niggles about the sustainability of DC’s growth seem persistent, with PE continuing to slip if looked at on a trailing basis.

The firm managed 22.2x in the fiscal year to April 2014 (though that’s on a pro forma basis due to the merger and could be skewed by one-off effects).

PE is seen at 19.3x in the current year and 15.8x in 2016.

With most of its rivals expected to return more in forward dividend yield terms than DC’s 2%, and available for cheaper multiples, some investors may vote with their feet.

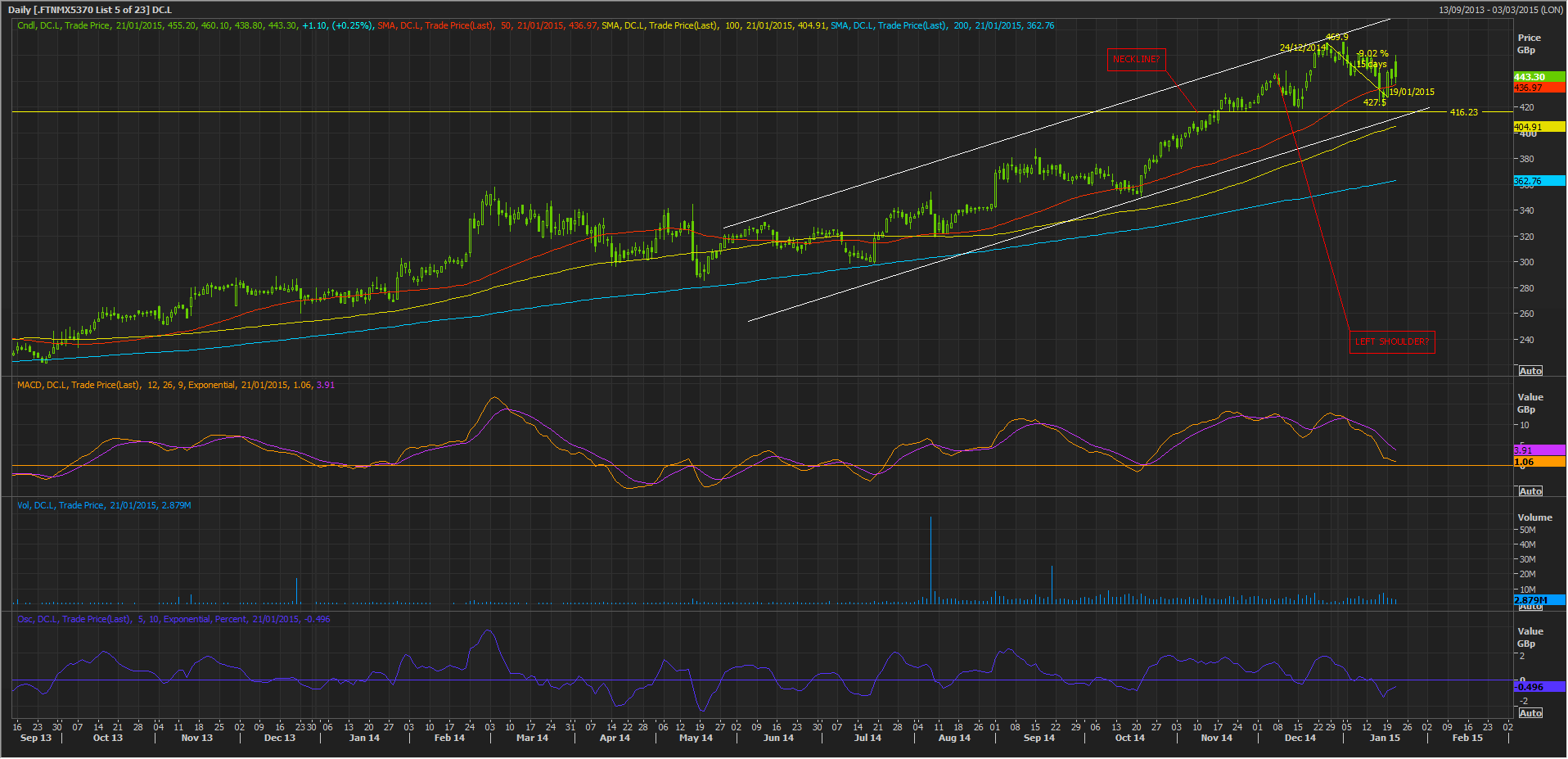

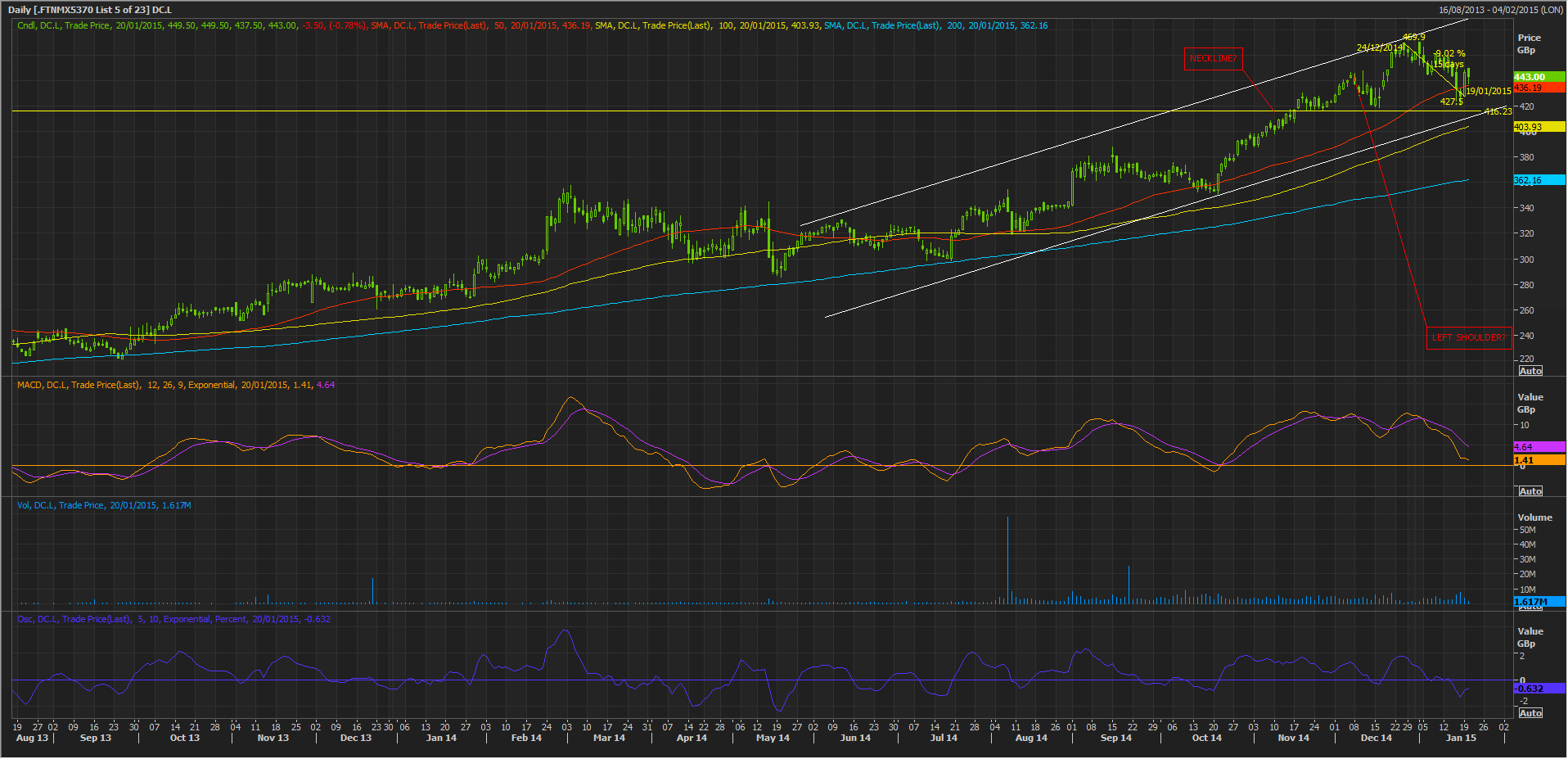

The ambivalent share price sentiment does little to nullify my suggestion yesterday that a theoretically bearish head-and-shoulders pattern is forming on the stock’s daily chart.

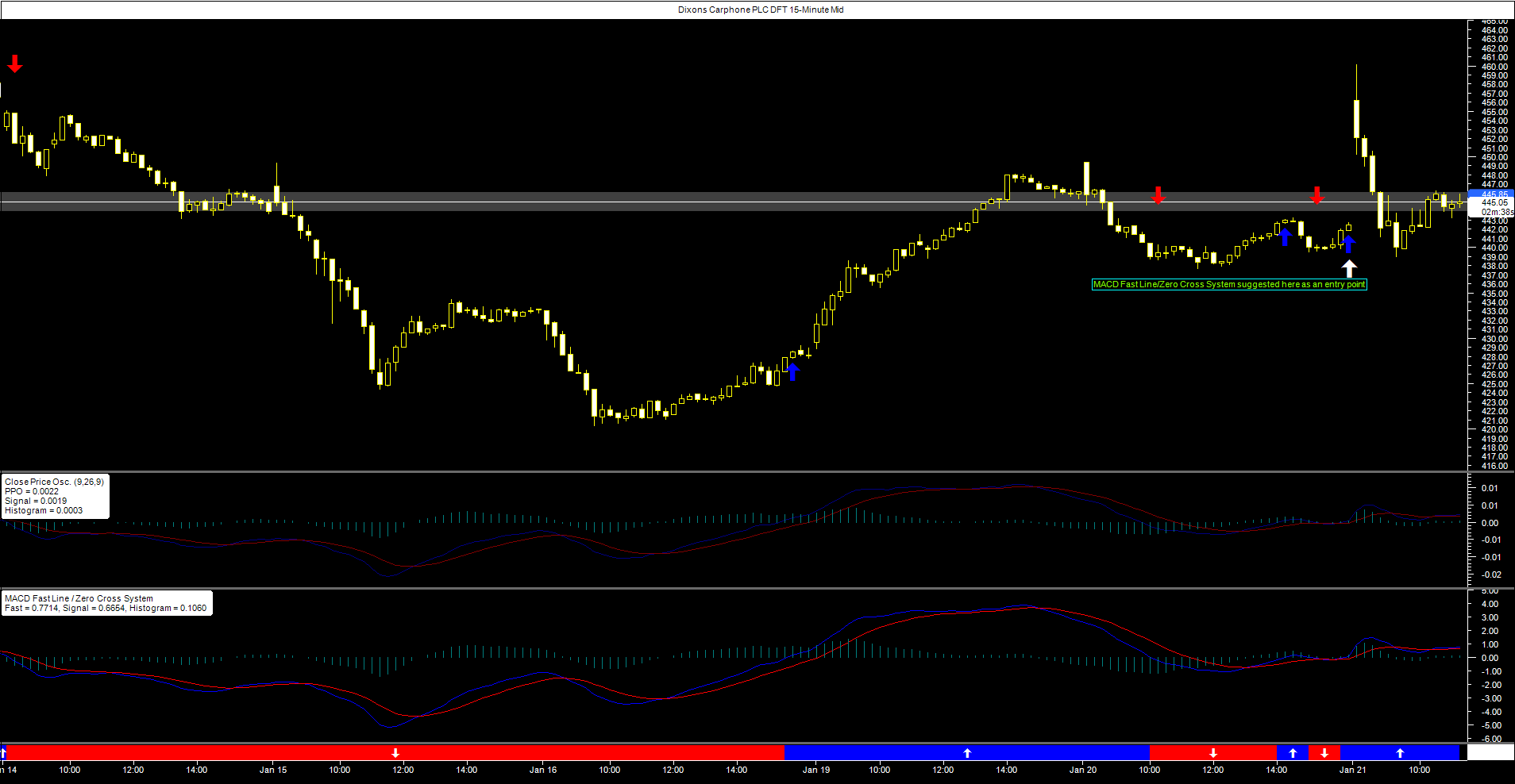

Still, if we zoom in tighter than the half-hourly time frame of Dixons Carphone Daily Funded Trade that we looked at yesterday, we may get a hint for the near term.

The ‘MACD Fast Line Zero Cross System’, included within City Index’s AT Pro platform flashed a ‘buy’ almost at the end of trading on Tuesday.

Following Moving Average Convergence-Divergence principles closely suggests the long entry ‘alert’ will not be revoked until one or both of the moving averages fall below their ‘zero’ divider.

{kind=link}