Dissecting the record high in the USD CNH

The Chinese currency has fallen to a record low versus the USD on Monday, which has caught the attention of the FX world. Although the […]

The Chinese currency has fallen to a record low versus the USD on Monday, which has caught the attention of the FX world. Although the […]

The Chinese currency has fallen to a record low versus the USD on Monday, which has caught the attention of the FX world. Although the CNH – renminbi which is traded offshore, but moves fairly closely with CNY – has fallen steadily since mid-September, it appears to be gaining broad interest only now that it has reached a record low.

No one to catch the renminbi when it falls

In recent years, the Chinese authorities and People’s Bank of China (PBOC) have a history of stepping in to prop up the renminbi when it is weak due to fears about the inflationary impact of a weak currency. Thus, investors may have been waiting to jump on the back of any PBOC move before trying to sell USDCNH.

The fact that the PBOC has failed, so far, to step in and drive its currency higher, could suggest a new stance from Beijing. It may be keen on allowing the renminbi to trade freely now that it is a member of the IMF’s global basket of currencies, and secondly, it may choose to tolerate a weaker currency to boost growth.

So why aren’t the Chinese authorities intervening?

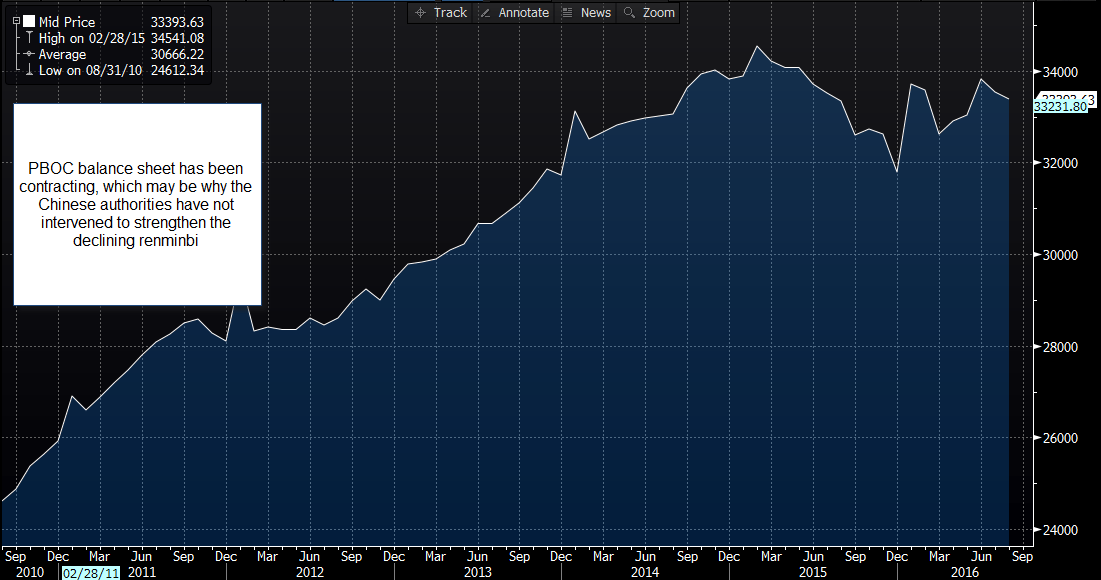

We think that this is down to the PBOC’s balance sheet (see figure 1). When it propped up the currency in recent years, it spent trillions of dollars of its FX reserves. This caused its balance sheet to contract by 10% since early 2015. Considering the Federal Reserve’s balance sheet has remained stable, and the ECB’s balance sheet is expanding, China looks like an anomaly.

Due to this, it may avoid spending anymore of its FX reserves to prop up the renminbi, lest it causes the PBOC’s balance sheet to contract further. A contracting balance sheet can suggest tighter monetary conditions, hence the Chinese authorities may be reluctant to tighten monetary conditions as its economy appears to be in recovery, after earlier fears of a slowdown and a hard landing.

Could currency wars return to the FX world?

At this stage there has been no pressure on Beijing from external authorities to strengthen the renminbi. Partly this is because the renminbi has only fallen versus the dollar, it is still fairly strong vs. the GBP, and has recently begun strengthening against the euro. In the past the US has attempted to call China a currency manipulator, however during US election season no one is currently in Congress to complain about the renminbi’s decline, but in a few weeks’ time newly elected US Congressmen and women might start to voice concerns about China’s currency and that is when the pair might start to see a sharp spike in volatility.

Washington may struggle to accuse Beijing

However, this time Washington may find it harder to accuse China of currency manipulation on the global stage because 1, the PBOC hasn’t stepped in trade in the physical market; 2, China’s economy has been weak, which can cause a natural decline in a currency; 3, it seems fair that the PBOC does not want to contract its balance sheet to try and prop up the renminbi when tighter monetary conditions could derail the recent economic recovery. Thus, the renminbi may be able to decline further against the greenback.

Right now, the decline in the renminbi is also a reflection of a strong dollar. Since we still see the dollar as the dominant force in the FX world in the coming months, this pair may climb further into record territory. The world may have to get used to a weaker renminbi, and it is worth watching the USDCNH rate closely in the coming days and weeks as it could signal a major shift in the FX market: Beijing may move towards a free-floating currency regime, which, over time, could have a dramatic impact on the dynamics of the FX world.

Figure 1:

Source: Bloomberg and City Index

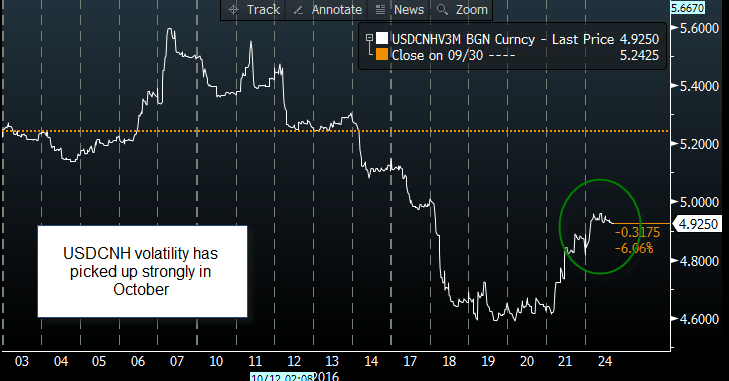

Figure 2:

Source: Bloomberg and City Index