Deutsche Bank 8217 s long sell off continues

Deutsche Bank is not going to collapse (but its shares will fall further).

Deutsche Bank is not going to collapse (but its shares will fall further).

That might seem like stating the obvious, but with shares down by half so far this year, and the cost of insuring its debt against default for 5 years (using Credit Default Swaps), blowing some 80 basis points wider this month; it’s not an entirely flippant to point to make.

After all, even in one of the toughest years for all European lenders since the financial crisis, Deutsche’s issues are among the most acute.

True, it is subject to the same challenges as all major banks in the region: sluggish economic growth which keeps a cap on earnings, and zero real rates which constrict net interest margins. But, partly because Deutsche was still among the biggest five lenders in Europe by assets at last year end, those common issues appear amplified for investors.

Another free-floating anxiety for Europe’s weakest banks is that some final straw or other will force them to open the hatch, under regulatory duress, to a flood of new capital.

The group on Wednesday disclosed the sale of UK-based Abbey Life for about €1.1bn. The disposal is expected to lift the bank’s key capital ratio by 10 basis points after it notched 12.9% in fiscal 2015, behind Credit Suisse’s 15% and UBS’s 13.6%.

Deutsche’s non-core asset disposal plans obviously run a lot further than that, as do its cost reduction goals. But these are already well known to investors, and do not appear to have stabilised sentiment by negating cap hike fears entirely.

Deutsche’s unusual trailing negative return on equity, according to data compiled by Thomson Reuters, is a partial explanation for shareholders’ persisting negative view.

Deutsche’s terrible year was made worse this week when the U.S. Dept. of Justice’s opening gambit towards settlement of a mortgage-related case emerged.

Whilst the eventual sum DB ends up paying is unlikely to be the $14bn the DoJ demands, reported forecasts of $2bn-$8bn keep the uncertainty going.

Either way, this settlement, and, potentially, three other major legal headaches it faces around the world, will require a larger legal provision than the €5.5bn booked at the end of June.

The least-worst option might well be a German finance ministry rescue plan, as reported by Die Zeit magazine, though the ministry tersely stated that it saw “no reason to speculate on such plans”, given that the “report is wrong”.

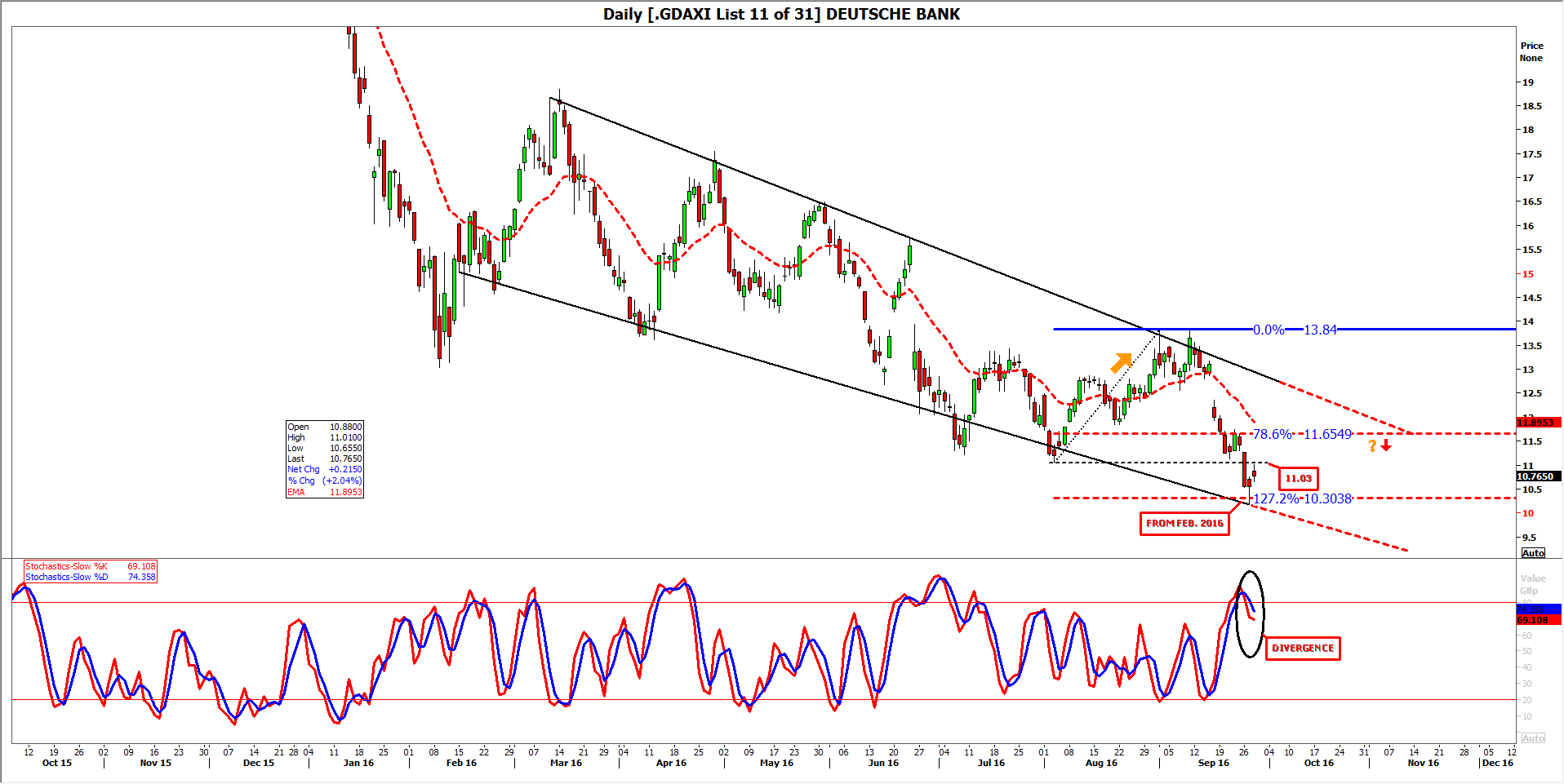

From a technical perspective, it has not escaped traders’ attention that the stock—on its best day since the DoJ’s demands emerged—did not touch €11.03.

That is the price where the shares in July commenced their latest attempt to end the latest leg of their 8-plus year decline.

Even if the shares can rally further this week, a strongly positive turn in fundamentals would still be needed to take out additional ‘overhead’ at €11.66, and the upper falling trend line in place since March, before another failure high at €13.80 (itself an attempt to take out €13.84 from 1st September).

Continued descent of the stock within this year’s channel looks like a more plausible scenario at this point.

Please click image to enlarge