Depressed coffee prices while Asian markets see structural shift

There is no doubt that tea is the hot beverage of choice across Asia – a cultural choice that will take a very long time […]

There is no doubt that tea is the hot beverage of choice across Asia – a cultural choice that will take a very long time […]

There is no doubt that tea is the hot beverage of choice across Asia – a cultural choice that will take a very long time to diminish. However it’s not a matter of tea versus coffee so much, but the actual rise of coffee consumption in addition to tea beverages that should be monitored by traders. Consumption per capita in emerging markets is still at around a third of developed markets. This is a per capita measure which ignores absolute demand changes.

Starbucks is a good measure for consumption patterns in developing markets, its recent earnings release paints an interesting picture. Comparable sales growth in China and the Asia Pacific (categorised as CAP) was 10% higher in the fourth quarter to September, compared with 7% growth in the Americas and a 1% decline in the regions surrounding Europe. The total number of transactions was 7% higher in CAP, beating all other regions in which Starbucks operates. The growth trend is being backed by investment with 132 net new stores added in the CAP region during the September quarter alone which is more than half the amount of new stores Starbucks is adding in its core Americas business.

Starbucks now operates more than 700 stores in China, which is just one of its key emerging markets. There are of course many other coffee players looking at expanding into emerging hubs to exploit untapped markets. Starbucks recently joined forces with Tata Global Beverages to commence its roll-out of stores in India. Total stores are expected to ramp up over the next few years after initial flagship sites are rolled out in places like Mumbai for example, where three stores were opened in October.

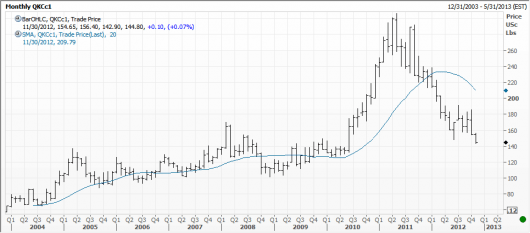

With the outlook for coffee consumption set to improve in emerging markets, one would expect the underlying price of coffee to improve. But it hasn’t, in fact coffee prices are trading at depressed levels, almost half the price they peaked at in late 2010-early 2011. See chart below sourced from Reuters. Much of the negativity in price is driven by short term market speculation. Macquarie Bank for example recently downgraded its coffee price assumptions, citing the potential for a strong harvest in Brazil this year to cause supply issues on the market.

We see this as too short sighted. Sure Brazil is a key producer and recent rains could see higher supply volumes, but data from U.S Commodity Futures Trading Commission (CFTC) suggests the commercial traders – those who physically deal in the supply and demand of coffee – are taking positions contrary to the speculators or non-commercial traders. Net long positions between commercial traders hit 15,100 contracts at the end of October compared to 8,400 at the end of September. Short positions exceeded long positions among the commercial traders category during the same time last year by around 13,800 contracts. The turnaround is significant in such a very short period of time.

The October net long position number is one of the largest net long positions for commercials in the past ten years. Past history is not always a good measure of future performance, but when going back over the last decade, net long positions above 10,000 among the commercial category more often than not were followed by rallies in the order of 3-5% in the following weeks.

Bottom line: The investment banks might have it right and the coffee market could continue to see supply growth but eventually the demand side of the equation will offset this. With coffee prices down so significantly and commercial traders increasingly betting they will go up in, we think the market should be watched closely over the next few weeks. We will provide an update in early 2013 on the demand and supply sides. Key instruments – Arabica and Robusta Coffee March 2013 contracts.