January 6, 2021 2:13 PM

Dems Win Georgia Senate elections; What that means US Dollar and CNH

On Monday, we discussed the potential outcomes of the Georgia Senate races and what it means for the US Dollar. With Democratic candidates Raphael Warncok and Jon Ossoff winning the elections, the Senate is now split 50/50, which means any votes in the Senate that are tied will be decided by Vice President-elect Harris. This will give Democrats control of the House of Representatives, the Senate, and the White House. In the short-term, the US Dollar should continue lower. President-elect Joe Biden is looking to increase coronavirus stimulus, working with Congress to grant eligible US citizens $2,000 in direct aid vs the current $600. However, could this news already be priced in? Today’s early price action would have you think so. In the longer-term, his proposals to increase taxes many result in pushing the US Dollar Index (DXY) higher.

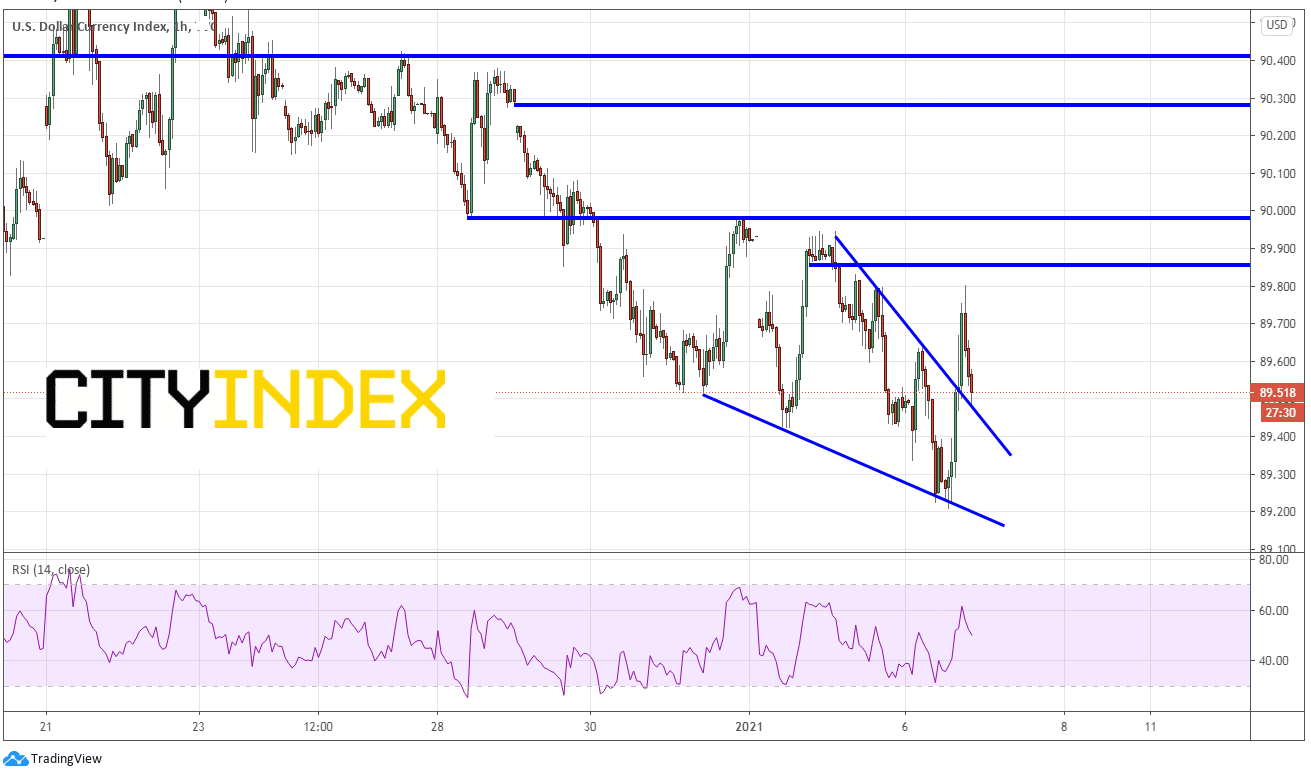

DXY

With the news of the unofficial Democrat winners, one would expect the S&P 500 raging higher today and the DXY would be lower. However, BOTH stocks and the US Dollar are higher. The DXY was lower overnight, so this appears to be a potential short squeeze as the market has been heading lower over the last few months. On a short-term 60-minute timeframe, the DXY has been in a descending wedge since Friday. Today, the index broke out of the top of the wedge and is near its target and horizontal resistance at 89.86. Sellers will be looking to take advantage of this pop to add to their position. The next resistance level is 90.00. Short-term support is at the downward sloping trendline of the wedge near 89.45.

Source: Tradingview, City Index

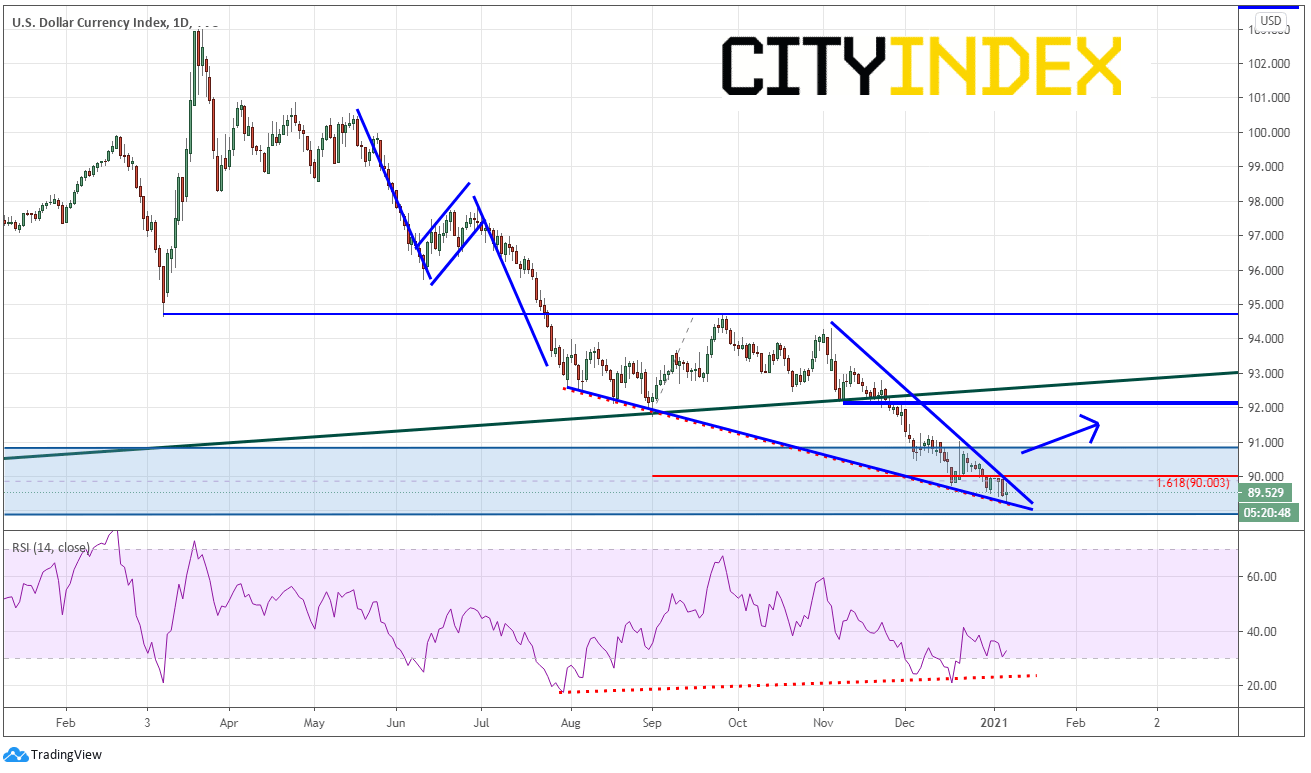

On a longer-term daily timeframe, DXY could be ready for a move higher. Price is currently trading within a support zone dating back to early 2018. It is at the 161.8% Fibonacci extension from the lows of September 1st to the highs of September 25th. In addition, DXY is near the apex of a descending wedge and the RSI is diverging with price. This confluence of supports suggests there could be a possible bounce on a longer-term daily timeframe. Longer-term resistance is near 92.00.

Source: City Index

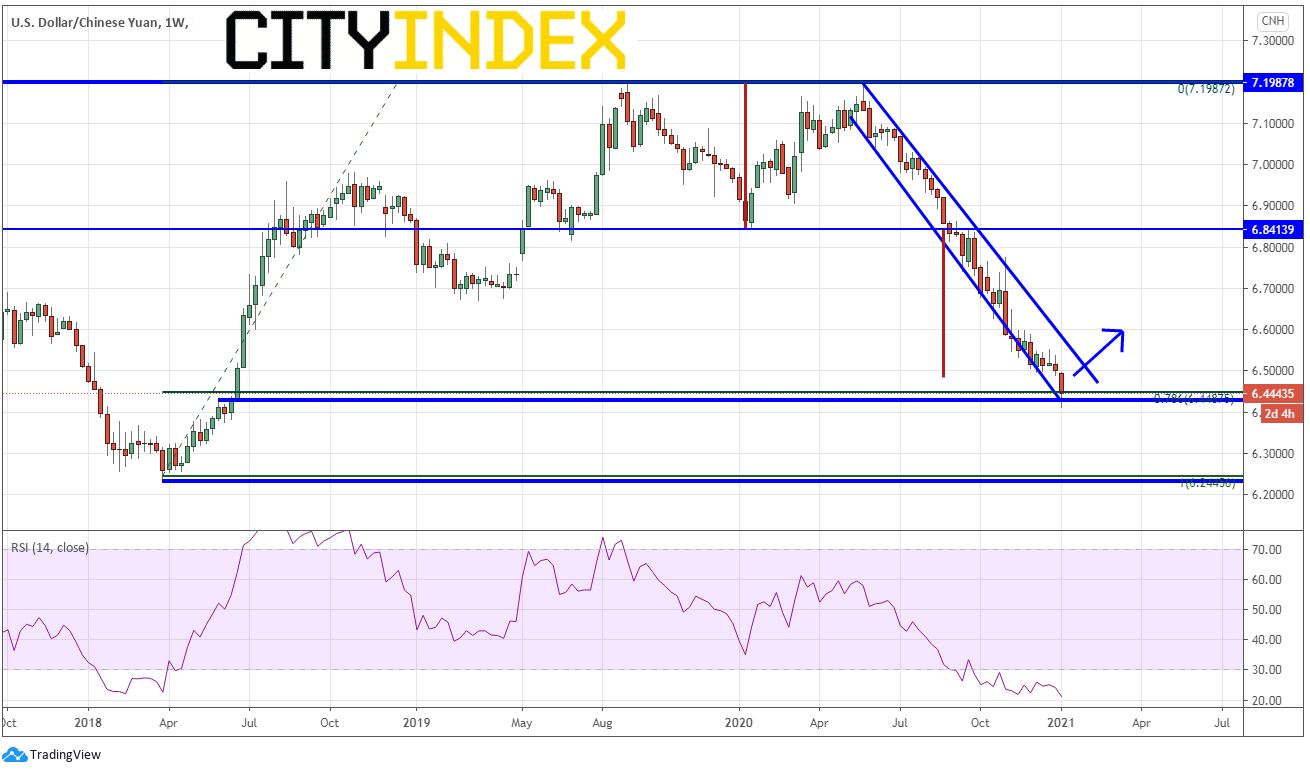

USD/CNH also suggests that the US Dollar may be ready for a move higher. The pair has been trading in an orderly downward sloping channel since late May 2020 after breaking below the double top neckline during the week of August 31st. The pair reached the double top target (red lines) this week, but has halted at horizontal support from May 2018, the 78.6% Fibonacci retracement from the lows of March 2018 to the double top highs and the bottom trendline of the downward sloping channel. The RSI is also extremely oversold, near 21.23. This confluence of support near 6.44 suggests there could be a possible bounce on a longer-term weekly timeframe. First resistance is at the top trendline of the channel near 6.51, however if USD/CNH breaks above, there is room to move much higher.

Source: Tradingview, City Index

The result of the Georgia Senate elections could result in 2 very different moves for the US Dollar over the next year. In the short-term, even with today’s bounce earlier, it’s possible that the stimulus will be too great and push the US Dollar lower. However, with the proposed tax hikes and the look at the longer-term charts, it appears that the US Dollar may be heading higher!

Learn more about forex trading opportunities.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM