Dectaper Bells Deflated Despite Jobs Report

Today’s simultaneous release of the Fed’s preferred inflation indicator with the November jobs figures is a fresh reminder of the dual forward guidance at the […]

Today’s simultaneous release of the Fed’s preferred inflation indicator with the November jobs figures is a fresh reminder of the dual forward guidance at the […]

Today’s simultaneous release of the Fed’s preferred inflation indicator with the November jobs figures is a fresh reminder of the dual forward guidance at the Fed’s disposal used at tempering enthusiasm of an imminent reduction in asset purchases.

December taper bells are not yet ringing despite the 2nd consecutive monthly release of +200K in non-farm payrolls, the lowest unemployment rate in exactly 5 years at 7.0% and a 15-month high in consumer sentiment.

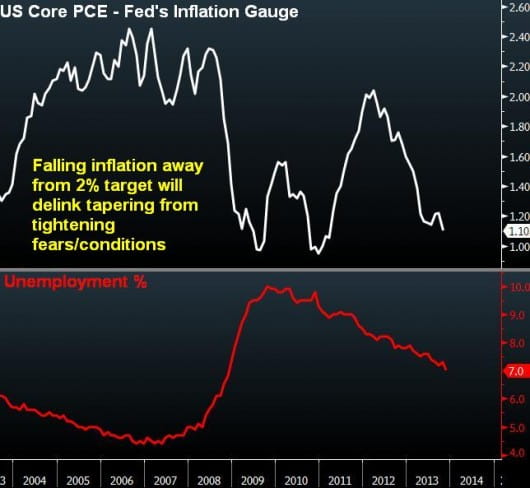

The 7% unemployment reminds us of the infamous Bernanke June remark suggesting an end of asset purchases once the unemployment rate nears 7%. It seems such a long time ago, until the forward guidance was refined further and inflation was introduced with more detail.

Don’t forget the other part of the Fed’s Forward Guidance

Although the 7% unemployment reminds us of that Bernanke reference, suggesting an end to asset purchases, the Fed has disinflation fears to add to its dovish armoury.

The Fed’s recent ruminations have clearly indicated that no rate hikes are due as long as the unemployment is “considerably below 6.5%” and inflation “to remain below our 2% objective”.

7% unemployment may be here, but inflation is at 1.1% y/y according to the Fed’s preferred personal consumption expenditure core price index. 1.1% is the lowest since March 2011.

As long as US inflation continues to fall away from the Fed’s 2% preferred target, any recurring speculation of tapering is likely will be delinked from tightening conditions in the bond market. This explains the euro’s resilience against the US dollar in the clash of the 2 reserve currencies despite today’s strong figures, especially in the aftermath of the ECB’s passive press conference.