Debenhams Mothercare shares trump rivals as they scale back price cuts

Two UK-based retailers were the largest leading shares on London’s stock exchange on Thursday after surprisingly strong results, both of which were bolstered by breaking […]

Two UK-based retailers were the largest leading shares on London’s stock exchange on Thursday after surprisingly strong results, both of which were bolstered by breaking […]

Two UK-based retailers were the largest leading shares on London’s stock exchange on Thursday after surprisingly strong results, both of which were bolstered by breaking a recent over-dependence by most British retailers on heavy discounting.

Debenhams Plc., owner of Britain’s second-largest department store chain and childcare specialist retailer Mothercare, traded as much as 5.7% and about 11% higher respectively after interim updates showed they were outpacing expectations.

Debenhams said a reduction in promotions backed by a more determined focus on online-based offers plus try-outs of new concessions to capitalise on under-used space, were bearing fruit.

Britain’s No. 2 department store chain in terms of sales, behind John Lewis, said these efforts helped lift pre-tax profit for the 26 weeks to 28th February to £88.9m, 4.3% higher than profit in the same half a year before, and above a consensus forecast of analysts polled by the company which totalled £84.5m

The first four concessions of Sports Direct, Britain’s biggest sporting goods retailer, had been well received and would be extended to 16 by August 2016, said Debenhams, taking up 20% of the 1 million square foot of under-used space it had identified.

Sports Direct, majority owned by businessman Mike Ashley, holds a 16.6% interest in Debenhams, though ruled out a bid for its rival early in the year.

Other concessions being tried out are Costa Coffee and Monsoon. These will be doubled to 20 and 10 respectively, while menswear chain Jack & Jones would be in 15 stores by September.

As in all things retail, scrutinising the underlying picture is a must and it quickly becomes clear that margins should remain an area of concern.

The decrease in markdowns gave an 100bp boost, but this was all eaten up by increasing sales of lower-margin cosmetics and softening Womenswear sales from the poor autumn (-50bp) and then ‘investment in price’ elsewhere (-50bp).

Net effect: flat margin vs. year before.

In fact, strictly speaking, the margin outcome should be -10bp year-on-year, because the firm’s regular New Season Spectacular promo (and its stated hit on margin) was moved from its usual H2 scheduling into H1.

It’s also worth keeping an eye on depreciation and amortisation which accounted for the erosion of £51m on the balance sheet.

Finally, again, inventory levels falling is reassuring, though note the 5.6% fall in value of goods in stock, and that current ‘terminal stock’–stock marked for discontinuation—constituted 2.9% of inventory, approaching the midpoint of the historical 2.5%-3.5% range and therefore implying weaker pricing to liquidate the inventory uptick.

Stripping out all negative and beneficial effects though, pre-tax profit still topped expectations.

That increases the likelihood of the firm matching full-year revenue consensus forecast of £2.9bn, +24% and £111.12m in pre-tax profit, +0.7%.

Debenhams’ high street rival Mothercare, albeit smaller and more narrowly focused, is also showing the countertrend benefits of eschewing discounts with a 5% advance in Q4 same-store sales, besting its 1.1% growth in the prior quarter.

It’s some vindication of new CEO Mark Newton-Jones’s strategy to push for more full-priced products to protect margins and represents a complete year of quarterly like-for-like sales growth (from stores open over a year).

International also remains strong with 11.4% growth if we take out foreign exchange effects.

The market forecast for a pre-tax profit of £12.3m full-year profit, 30% higher year-on-year, now looks very likely to be achieved.

The fight against the main competitive threats from online (namely Amazon) and low-cost (mostly Primark) aren’t going away anytime soon, though, and that’s reflected in Mothercare’s own margins too.

Its operating margin collapse by 12% into the red in 2012, moderated to a mean of 2.5% in the two years that followed and is forecast to average more than 3.5% during 2015-2017 inclusive.

At the same time market growth expectations now pitch Mothercare at a level that’s above steady burner Ted Baker Plc., which pays a respectable dividend (Mothercare does not) yet whose latest price/earnings ratio was 29x vs. MTC at 32x.

Mothercare, like Debenhams, could well be proved right in terms of its decision to stand aside from the retail herd rushing headlong downmarket.

But I think it’s going to take some time for complete vindication, with neither having started from a position of unequivocal strength.

That leaves them vulnerable to a market that at some point will return to a bias for total return.

In Mothercare’s case, the backdrop of its shares coming up to a notable retracement marker suggests investors may re-consider, especially since the net gain since May last year is a solid net 100%-plus.

The point in question is at 236p, 23.8% of the bounce back from 61p all-time low in February 2000 toward all-time highs c.800p in 1996.

The stock challenged the levels above this mark last July, and failed.

Weak momentum in the daily chart right now argues against success on a second attempt.

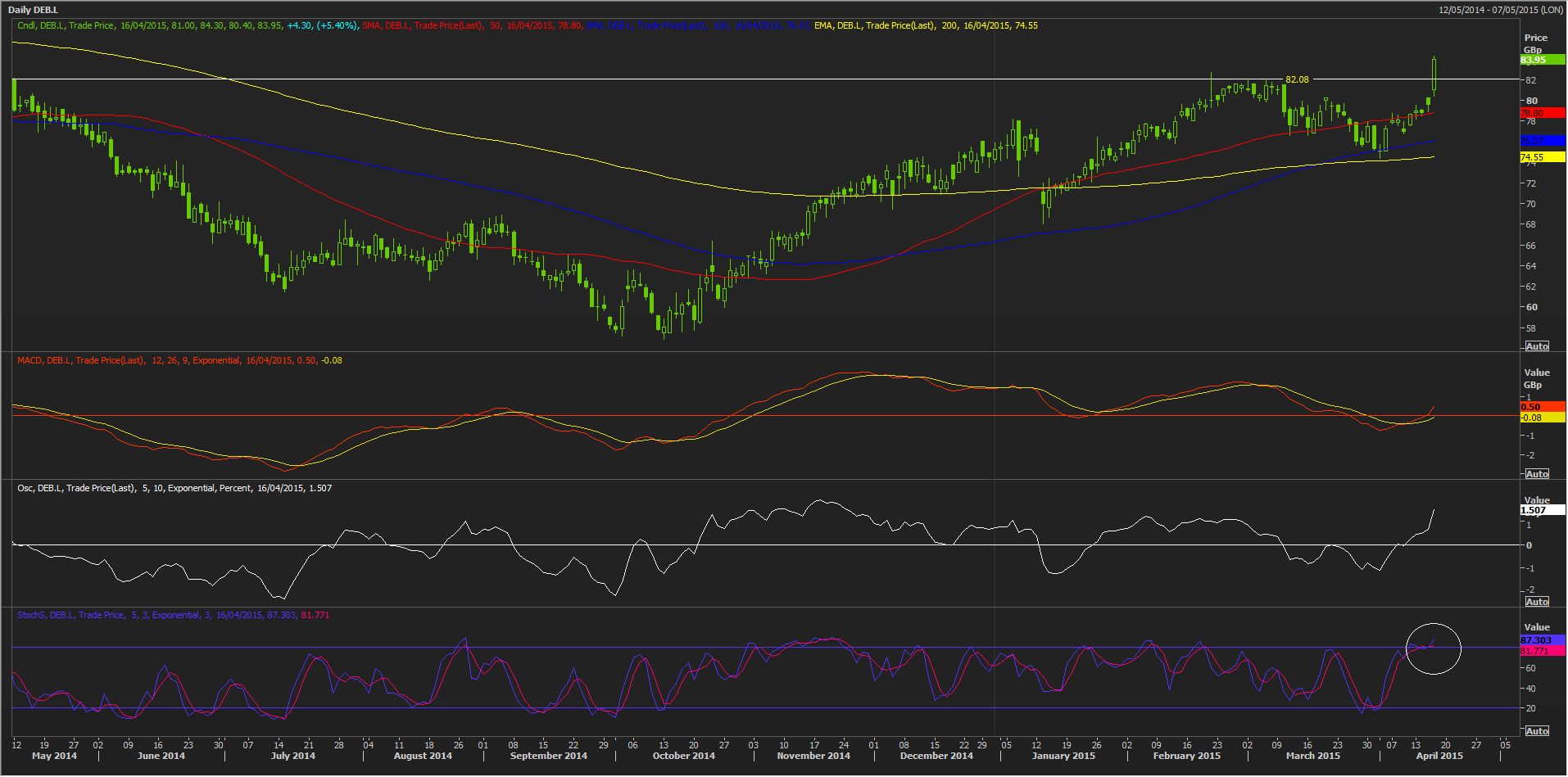

As for Debenhams shares, on the face of it, they’re in better shape in the daily view.

They’re also coming up to a resistance that stymied an attempted break out last year, with the balance of current sentiment favouring fast buying.

The MACD system sub-chart shows its ‘fast’ moving average (MA) red line above the slower MA, which is also inverting upwards.

Below that, the percentage oscillator sub-chart (white line) concurs, rising in positive territory.

The last sub-chart calls for caution though: the Slow Stochastic system has its slower %K MA crossing further into overheated territory than the faster %D MA.

Not ideal conditions to call for a continuation of the uptrend.