DAX relapse deepens post Fed

Equity investors are paying dearly on Friday after the Fed decided to hang fire in September, something many had been demanding for months. In the […]

Equity investors are paying dearly on Friday after the Fed decided to hang fire in September, something many had been demanding for months. In the […]

Equity investors are paying dearly on Friday after the Fed decided to hang fire in September, something many had been demanding for months.

In the event, it was a ‘pyrrhic victory’ for stocks.

It now looks like continued uncertainty about when the world’s most closely watched central bank will pull the trigger is more damaging than its ‘easy money’ benefits.

All major Western stock markets were in the red on Friday.

European equity indices were among the hardest hit, especially Germany’s DAX30.

That’s partly because the Fed’s fudge of its seemingly interminable dilemma has coincided with unrelated headwinds for two heavily-weighted German stocks.

On Friday, poor overall sentiment combined with continued fallout from Germany’s abandonment of nuclear energy two years ago.

The country’s nuclear exit forced its top power producers, whose atomic exposure goes back more than half a century, to rapidly retrench.

But doing so has been expensive.

Power giants, RWE AG and E.ON SE, have been forced to make billions of euros of provisions to shutter and make-safe nuclear facilities.

Consequently, selling pressure on their shares this year has been relentless.

E.ON’s stock is down 43%, RWE’s off 59% year-to-date, wiping out a combined €21bn in market valuation.

But another leg of their sell-off was initiated earlier this week after media reports of a shortfall of up to €30bn more in nuclear exit costs.

E.ON and RWE traded at the bottom of the DAX for most of Friday.

Germany’s internal issues are of course combining with a two-pronged external hit.

Whilst the volatility of the summer seen in China’s stock market has calmed, by no means is this a sign of economic recovery in Germany’s No.3 export partner.

And, buyers in its No.1 trading partner, the United States, may soon have additional financing costs to consider, despite the Fed having stood pat last night.

Either way, the Federal Reserve has tacitly signalled a new concern about the strength of the US economic recovery by voicing concerns over slowdowns elsewhere.

Whilst Germany’s own economic rebound accelerated in the second quarter of 2015, it did so in less robust fashion than expected.

Crucially, Germany was largely supported by foreign trade, whilst slowing investment acted as a brake on Europe’s largest economy.

Friday’s DAX sell-off can thus be interpreted as a rekindled wariness among investors in Germany’s equities.

Much like the Fed’s worry, the concern is that Germany’s nascent economic recovery could be kyboshed by overseas factors.

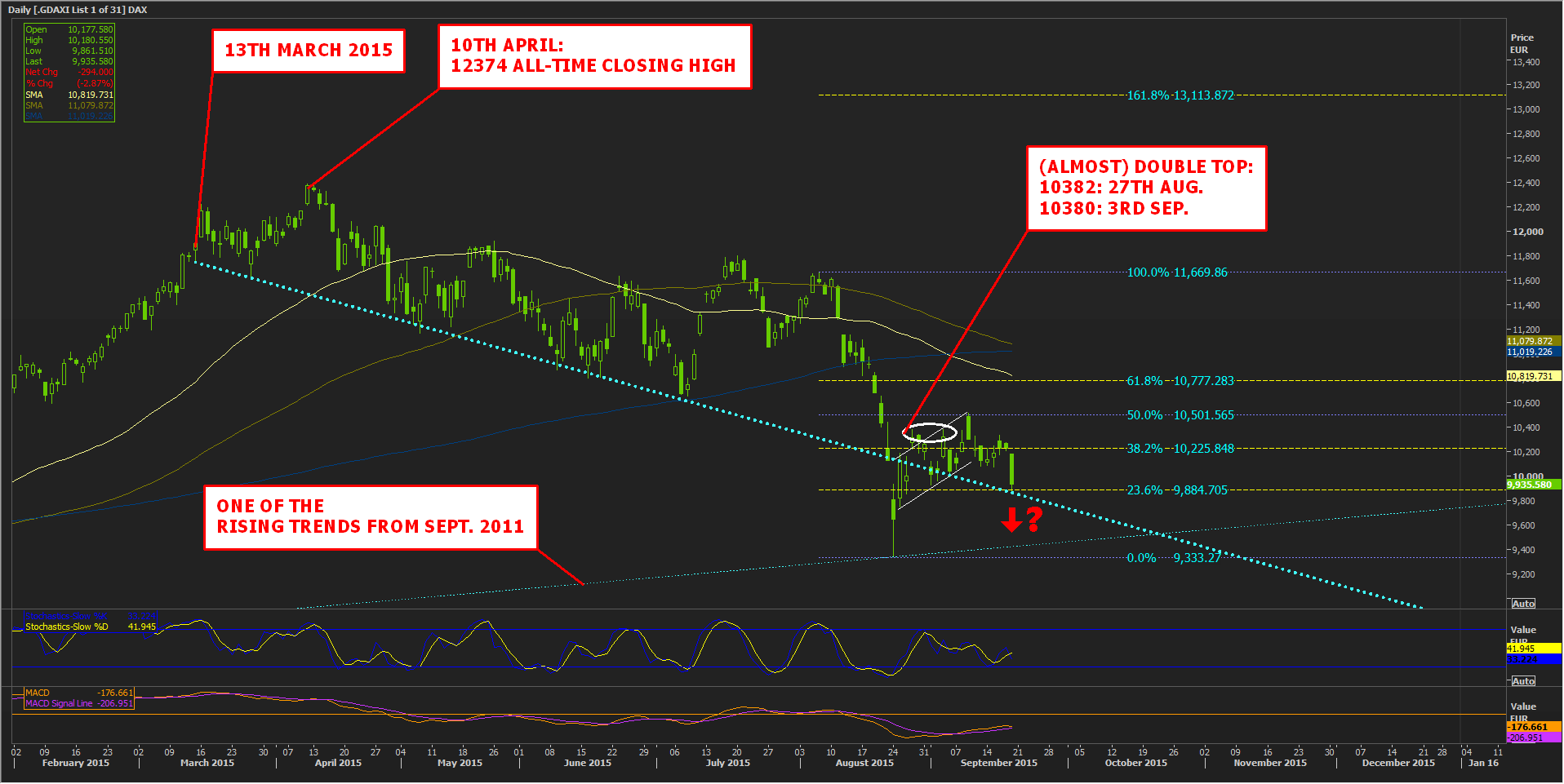

On the DAX, this wariness has been embodied by a steadily descending trend from all-time highs hit in April around 12374-12390.

In recent weeks, trader attention has focused on extensions from the year low at 9333.27, seen late last month.

DAX’s upward advance from that has faced formidable challenges.

Firstly there was what amounted to an effective double top (albeit imperfect) between 31st August and 3rd September.

This was closely followed by struggles with important 50% and 38.2% Fibonacci intervals.

The DAX30 is currently resting on the weak 23.8% marker combined with the falling trend mentioned earlier.

A break could open the way back to the year’s lows.

However, one of the long-term lines rising from September 2011 could break the DAX’s fall.

Either way, it’s clear the German benchmark has so far failed to break the funk it entered after failing from Icarian heights in the spring.

Its first step to begin doing so would be to mount the confluence of resistances created by its defeated recovery off 2015 lows.

This resistance region is between 10128 and 10501.

Please click image to enlarge