DAX higher as Draghi s press conference looms

European equity markets are trading mixed following a weaker close on Wall Street last night, where stocks ended near their lows. Similarly, Asian Pacific markets […]

European equity markets are trading mixed following a weaker close on Wall Street last night, where stocks ended near their lows. Similarly, Asian Pacific markets […]

European equity markets are trading mixed following a weaker close on Wall Street last night, where stocks ended near their lows. Similarly, Asian Pacific markets ended mixed overnight with China rebounding and Japan closing lower. US index futures are up slightly after eBay reported a stronger-than-expected quarterly profit after the closing bell last night and raised its full-year adjusted profit forecast. More, big, US technology companies are due to report their results today, including Microsoft, Amazon and Google. So, it could be an interesting day on Wall Street. In Europe, the focus will undoubtedly be on the European Central Bank press conference. Comments from Mario Draghi, the ECB President, could cause some sharp moves in both the euro and the European indices, in particular the German DAX index which is outperforming at the time of this writing. Traders should expect a volatile afternoon, for a change.

The ECB is widely expected to leave its monetary policy unchanged at this meeting, which should come as no surprise at 12:45 BST. But it is Mario Draghi’s press conference, which starts at 13:30 BST, that will garner more attention. The ECB’s bond buying programme is almost 8 months old, yet inflation in the Eurozone is literally non-existent with the Consumer Price Index (CPI) falling 0.1 per cent year-over-year in September. Clearly, policymakers are miles away from achieving the ECB’s inflation target and so are undoubtedly disappointed with the progress of QE thus far. Economic growth is also weak, while unemployment remains high for many Eurozone countries. Admittedly, the lack of inflationary pressures is mainly due to the falling price of oil and other commodities, as after all, core CPI is running at 0.9% at the moment – a small, but notable, improvement from about 0.5% at the start of this year. Still, core CPI ‘should’ have risen more meaningfully since the inception of QE and inflation expectations are, somewhat unsurprisingly, very low.

So for all these reasons alone, not to mention the on-going Chinese growth concerns and VW’s emission scandal et al., the market is demanding for more from the ECB. Speculators are hoping that at this particular meeting the ECB is at least talking about the prospects of a more beefed-up version of QE package. If Mr Draghi does signal the ECB’s intention to expand the size and duration of the stimulus package at some future point in time, perhaps in December, then this could be BIG news. The euro could drop sharply, especially against some of the weaker currencies like the Canadian dollar, as my colleague Matt Weller reported yesterday. The weaker euro and prospects of further easing steps from the ECB should also boost the appetite for European stocks.

That being said however, there’s significant scope for disappointment now. The ECB could easily blame external and temporary factors, such as the oil price weakness, for the lack of inflation and insist that it is far too early to judge whether QE is working as expected. In this scenario, the euro may actually shoot higher and European stocks tumble.

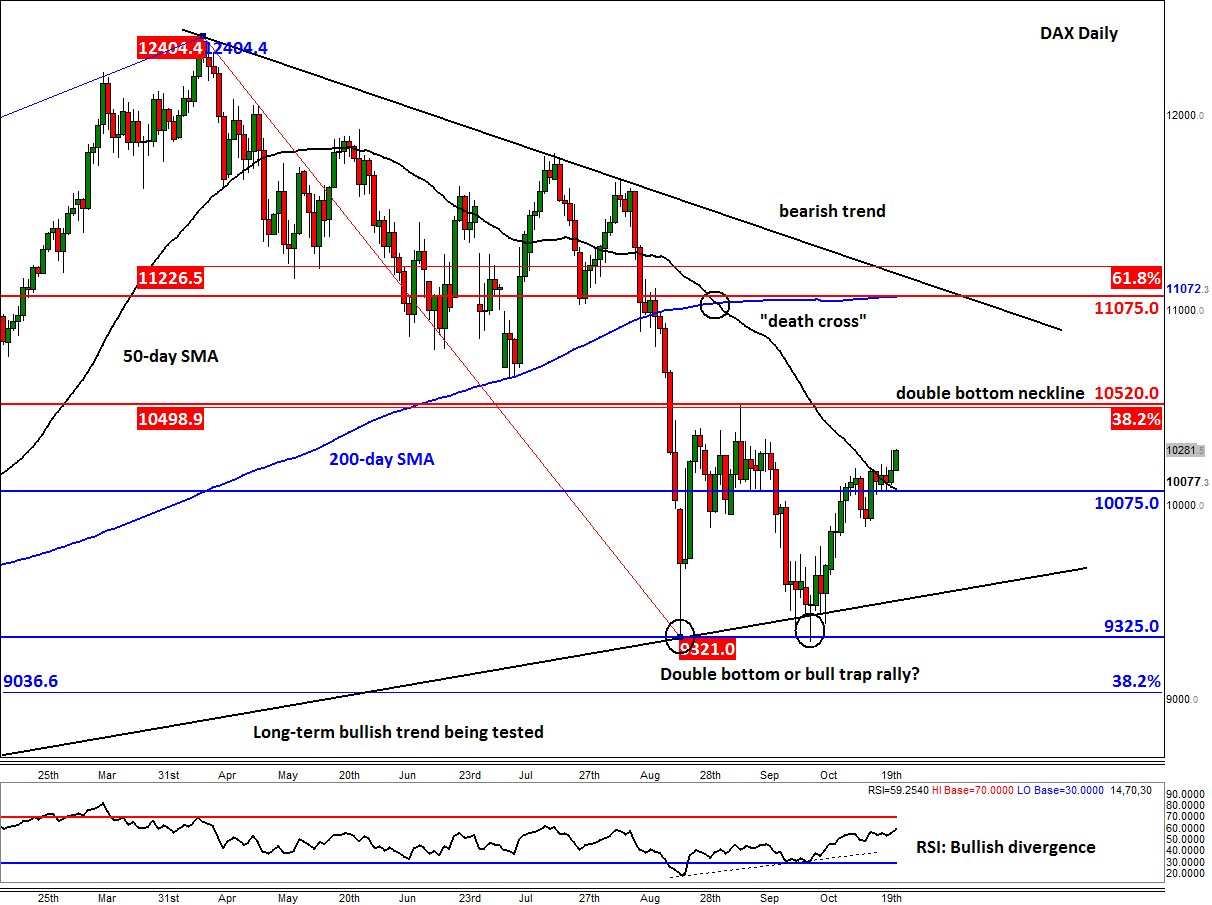

Ahead of the ECB’s press conference, the German DAX index is technically looking strong, but is by no means out of the woods just yet for it remains below the double bottom neckline at 10520/5 area. The DAX has also underperformed its US peers. While some might say it has a bit of catching up to do now, there must be a good reason why it had underperformed in the first place – and there was: car makers, due to VW’s emission cheating scandal and their exposure to China, where the economic growth is cooling. This means that if the global equity markets start to turn lower again, then the DAX could be an obvious choice for the sellers. But as mentioned, a lot could change today and for the better, depending on the ECB’s message. From a purely technical point of view, the short-term outlook on the DAX would turn decisively bullish upon a break above the noted 10520/5 resistance area. If seen, the DAX could then rally all the way to around 11000/75 where it will meet a bearish trend line and the 200-day moving average. On the downside, a break back below support and the 50-day SMA at 10075 would be a bearish outcome. If seen, the DAX could then drop all the way back to the long-term bullish trend line, around 9500-600, before deciding on its next move.