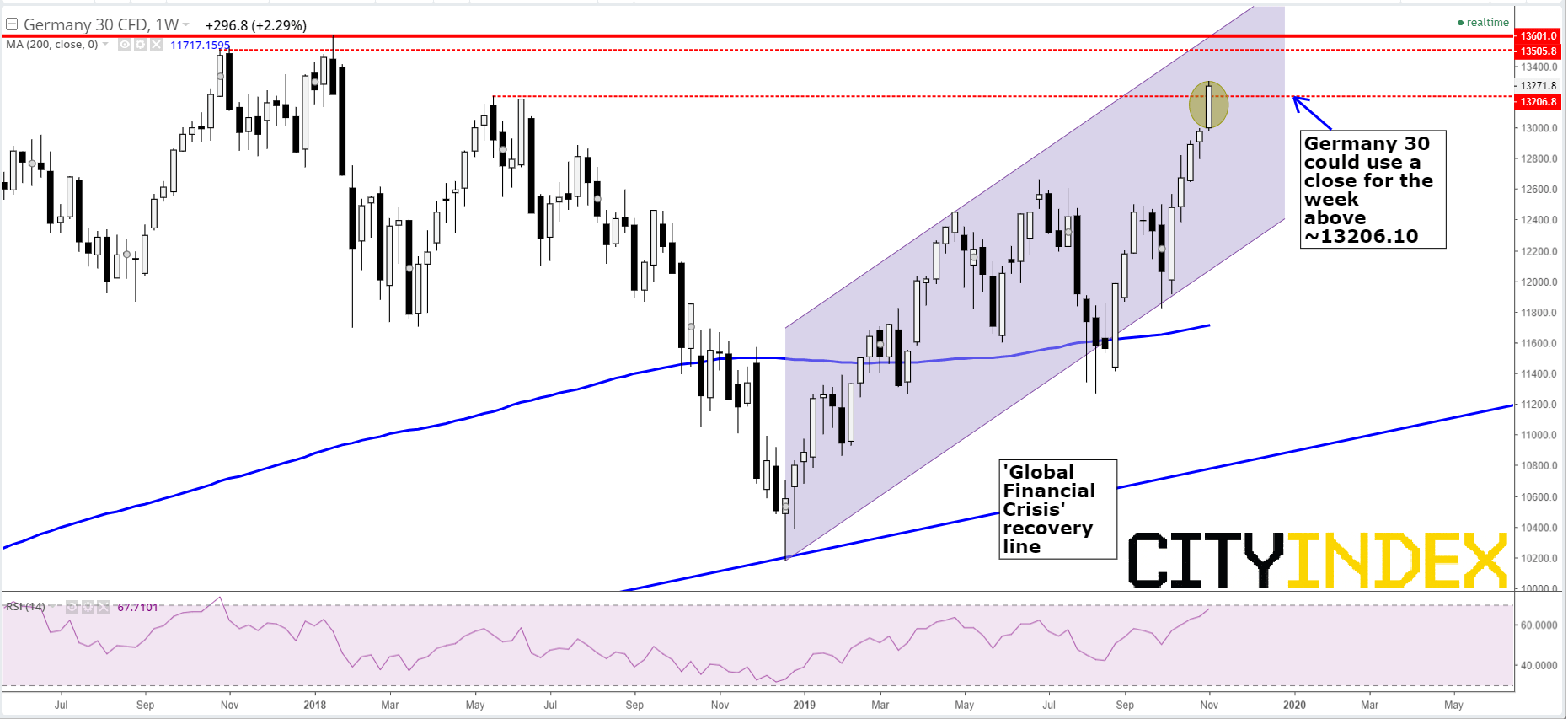

Germany’s benchmark could use a fifth weekly higher close this Friday

This week’s swings between an over-arching appetite for risk and more aversive sentiment have played havoc with stock markets’ short-term direction. On Thursday at least, equity indices appear to be on an upswing on renewed signs that the long grind towards a trade deal could soon bear its first fruit. In Europe, a pre-eminent beneficiary is Germany’s DAX index. The U.S. is Germany’s biggest trading partner overall, followed by the United Kingdom. China is a top-five export partner of Europe’s growth engine. With Brexit worries beginning to alleviate as trade conflict escalation shows signs of reaching its limits, it’s little wonder that the DAX has begun to outperform large European counterpart markets on a year-to-date basis. Naturally, the obverse of the DAX’s tie to high-level geopolitics is that a reversal of recent improvements on the global front will pose risks to the German benchmark’s rebound.

Chart points

Quite remarkably, DAX’s advance from late 2018/early 2019 lows is intact. The rough channel over that stretch continues. In the weekly view, the current focus is whether the market can signal readiness to extend its resilient run of four weekly gains with a fifth higher close on Friday. A close above the closest key resistance—circa 13210, a peak in May 2018—would provide a provide a strong basis for upside progress to continue. A failure would add to suggestions that a consolidation may be due.

Germany 30 CFD – Weekly

Source: City Index

Latest market news

Yesterday 11:48 PM

Yesterday 11:16 PM

Yesterday 05:00 PM

Yesterday 01:13 PM

Latest Indices articles

Yesterday 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM

April 15, 2024 06:08 AM