Czeched out CNB drops peg with the euro

If you want to drop a currency peg, then the CNB can show you how to do it. After dropping the EUR/CZK peg earlier today […]

If you want to drop a currency peg, then the CNB can show you how to do it. After dropping the EUR/CZK peg earlier today […]

If you want to drop a currency peg, then the CNB can show you how to do it. After dropping the EUR/CZK peg earlier today the koruna has rallied less than 1% versus the euro, and volatility has been moderate. Dismantling a long-held currency regime doesn’t need to be as volatile or panic-stricken as Swiss peg debacle back in 2015.

We mentioned last Tuesday that the CNB could drop the peg at any time after the bank failed to commit to maintaining the peg after April 1st. Doing it sooner rather than later was a good call from the CNB for a few reasons:

Positioning was not as extreme in EURCZK as it was in EURCHF, but there was still approx. $65bn of speculative inflows in EUR/CZK. The CNB should be praised for the smooth transition from a pegged currency to a floating one.

So where does the CZK go now?

As mentioned, the CZK has rallied only moderately on the back of today’s CNB action, and it isn’t even the best performing currency in the EMEA space. The timing of dropping the peg has been pre-emptive: the economy isn’t too hot that the CNB desperately needs a stronger currency, neither are bond yields too high, which means the CNB doesn’t have to worry about hiking interest rates. Instead, the CNB can keep a steady ship for now, although it will want to have one eye on inflation, which has risen to 2.5%, the highest level since the end of 2012. We don’t expect the CNB to hike interest rates yet, although this could be on cards for the summer months. If the CNB does hike rates then we would expect CZK appreciation against the euro.

Is the post-peg Swissie price action a blueprint for the CZK?

Although we think that the CNB masterfully avoided a SNB –style debacle today, the CZK may not be able to avoid the same fate as the CHF. The Swissie has remained stronger versus the euro since its peg was dropped in 2015, and EUR/CHF has not managed to get back to 1.20, it is currently trading at 1.07, and has lost 3.6% in the last 9 months as the ECB embarks on an extension of its QE programme. The CZK could also trade with an upward bias while the ECB maintains its ultra-lose monetary policy, and we think it will be tough for EURCZK to get back to 27.00 in the aftermath of this currency shift.

Upward pressure on the horizon:

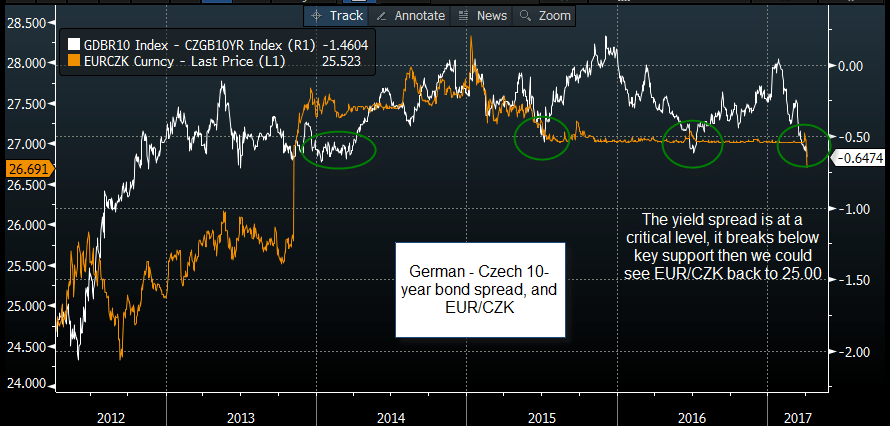

The CZK might only be moderately higher today, but there could be upward pressure on the horizon. Right now the spread between German and Czech 10-year bond yields is at a crucial support zone that dates back to 2014. If this spread drops further and the spread widens to more than -0.65 basis points, as you can see on the chart, then we would expect further EURCZK appreciation, potentially back towards 25.00 in the next couple of weeks.

Figure 1:

Source: City Index and Bloomberg