Currency Wars amp LTRO Repayments

The euro’s gains may just be starting as the ECB balance sheet shrinks further from LTRO repayment 278 European banks have repaid €137 bn in […]

The euro’s gains may just be starting as the ECB balance sheet shrinks further from LTRO repayment 278 European banks have repaid €137 bn in […]

The euro’s gains may just be starting as the ECB balance sheet shrinks further from LTRO repayment

278 European banks have repaid €137 bn in the first LTRO operation, which raised €489 bn in December 2012. LTRO-2 from February 2012 now receive a repayment of about €250 bn.

On today’s announcement, Spanish 10-year yield saw its biggest decline of all Eurozone bonds, losing 15 bps versus a mere three bps for its Italian counterpart. This is partly explained by the fact that Spanish banks were the biggest borrowers in LTRO-1 lending, accounting for 41% of total take-up, compared to 25% from Italian banks.

Repayments of LTRO-2 will be announced on February 22 and will take place on February 27. As European banks repay about €400 bn, the immediate analysis to make is to expect a reduction in liquidity and a run-up Eurozone overnight interest rates—something the ECB has worked hard to avoid. But EU banks will continue to seek funding from the ECB’s shorter-term LTROs, keeping their needs sufficiently met.

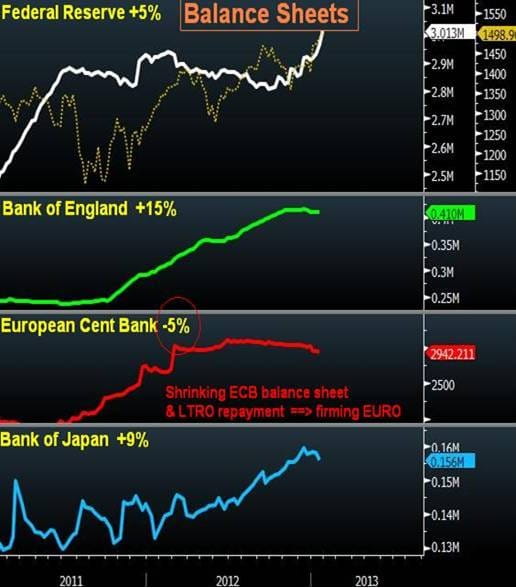

Regardless of whether LTRO repayments will keep €200 bn or €500 bn in excess liquidity in the Eurozone monetary system, the ECB is the only major central bank not to have issued a fresh dosage of asset purchases as is the case of the Fed, BoJ and inevitably the BoE (following its triple quarterly growth dip). The charts below show the ECB balance sheet has in fact shrank by 5% over the last six months compared to increases of 5-15% for the other big three.

The ECB’s refraining from currency wars may not be the only reason to the euro’s sharp rebound. 32-month highs in Germany’s business surveys and solid auctions by most periphery Eurozone nations as of late can be categorized among “stabilising fundamentals” for the Eurozone. The road to $1.37 in EUR/USD remains intact as suggested in our December 4 note “Is that a Reverse H&S or you’re happy to us?”. $1.40 is no longer deemed an aggressive forecast, and is considered baseline objective for early Q2 2013.