Crude time for OPEC Russia to walk the walk

After surging higher at the end of last week, crude oil prices have started the new week on the front foot. Oil and other traders […]

After surging higher at the end of last week, crude oil prices have started the new week on the front foot. Oil and other traders […]

After surging higher at the end of last week, crude oil prices have started the new week on the front foot. Oil and other traders have completely shrugged off the weaker Chinese trade and Japanese GDP figures that were published overnight. With Japan’s Nikkei closing up more than 7 per cent higher and European stocks also coming back strong this morning, the market either expects to see more Bank of Japan monetary stimuli and/or is more hopeful that oil prices have bottomed out.

After all, Japan’s economy contracted 0.4% in the fourth quarter of last year, which was more than expected. Other Japanese figures, including industrial production and tertiary industry activity, also disappointed expectations overnight. In China, January exports dropped by a sizeable 11.2 per cent year-over-year after a 1.4 per cent decline in December, while imports fell for the fifteenth consecutive months, this time by a huge 18.8 per cent. Oil imports in China also fell sharply, by 20 per cent month-over-month. Although this may look weak, it should be noted that the previous month saw crude imports surged to a record high as China took advantage of the slumping prices to fill up their strategic reserves. Still, the 20% drop is significant and if further declines are reported then this would bode ill for oil demand growth.

At the moment, speculation is rife that some of the largest oil exporting countries will cut oil production in an effort to shore up crude prices following last week’s comments from the energy minister of the UAE. If this is indeed the reason for the oil price rebound then they better walk the walk now, having talked the talk. Else, at the very least Brent may lose its premium over WTI. In the US, signs of imminent oil production cuts are meanwhile rising, judging for example by the latest rigs counts data from Baker Hughes, which shows another 28 active oil rigs were shut down over the reporting week. So, unless oil demand growth declines noticeably now, the oil market looks set to start rebalancing soon, possibly without even the need of significant production cuts from the OPEC and Russia.

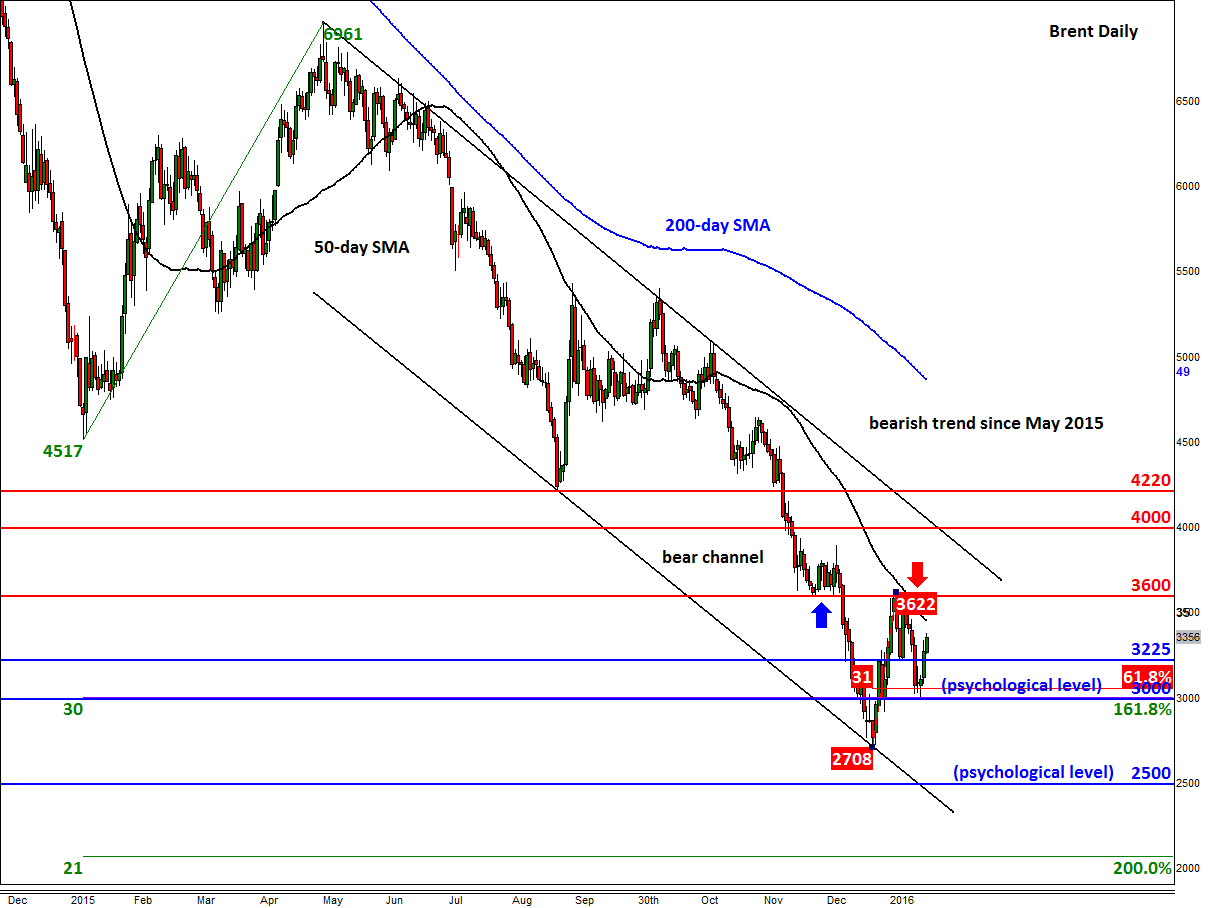

Meanwhile from a technical point of view, oil’s rebound suggests we have seen a bottom – at least in the near-term, anyway. Brent’s desire to hold its own above the key 61.8% Fibonacci retracement and psychological level of $30 is a bullish outcome in the short term outlook. For as long as it holds above $30 now, there is a strong probability that we will see significantly higher than significantly lower levels now. For Brent, a break above the recent range highs of around $36.00 could pave the way for a move towards the resistance trend of the bearish channel at $40.00, and potentially higher. But if Brent breaks back below $30 then all the bets are off and in this case $25 could become in focus once more.

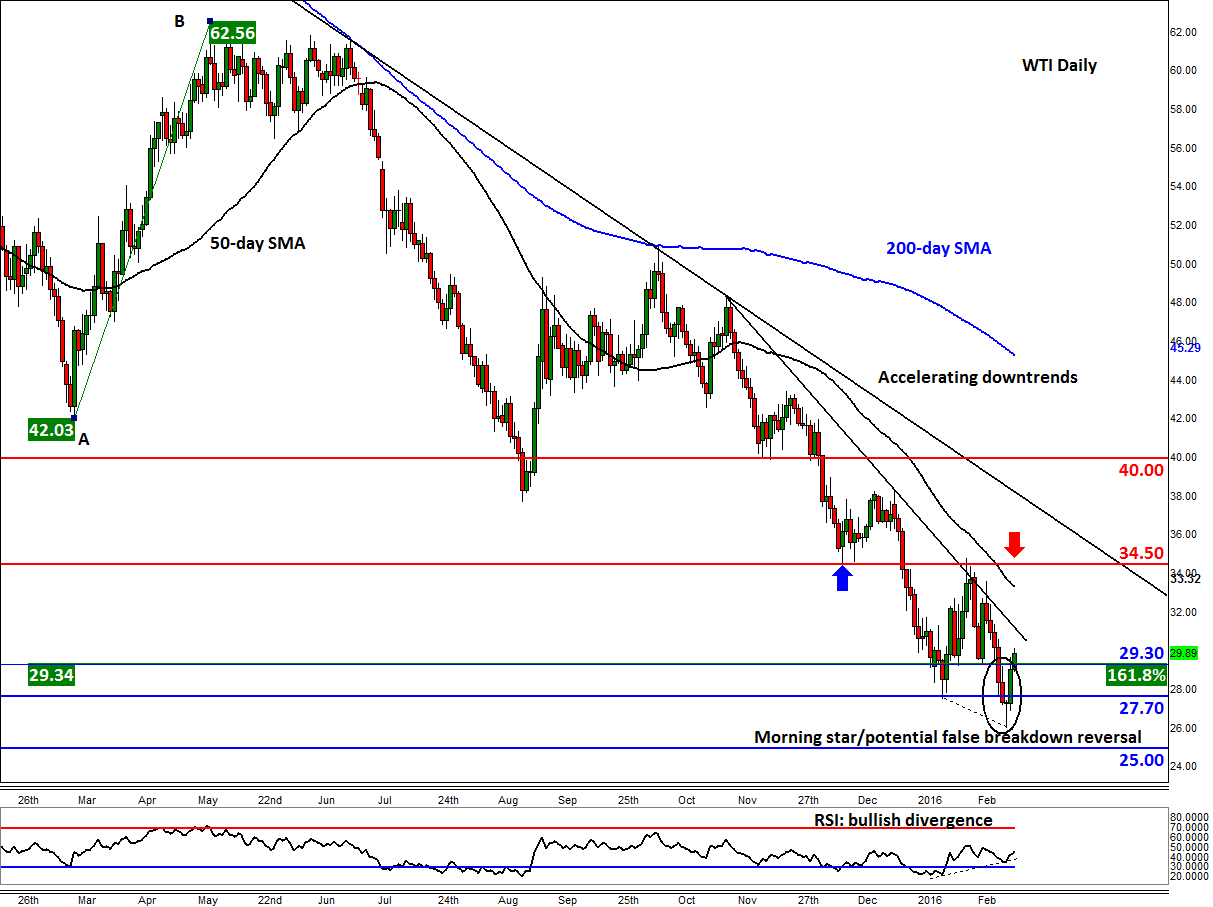

WTI’s doji candlestick formation on Thursday, combined with the follow-through in the buying momentum on Friday, suggests we may have a rare three-candle reversal pattern called a ‘morning star’ being formed. The reversal can only be confirmed if and when WTI breaks above the recent range highs of around $34.50, but the fact that the RSI is in a state of bullish divergence is a good sign for the bulls nonetheless. This potentially bullish setup would become invalid however if WTI moves back below support at $27.50. In this case, a potential drop towards the next psychological level of $25.00 would become highly likely. But for now, it appears as though the short-term path of least resistance has changed course to the upside.