Crude stages small recovery after Monday s tumble

Crude oil prices have bounced back a little following their sharp declines the day before. Brent appears to be a little bit firmer relative to […]

Crude oil prices have bounced back a little following their sharp declines the day before. Brent appears to be a little bit firmer relative to […]

Crude oil prices have bounced back a little following their sharp declines the day before. Brent appears to be a little bit firmer relative to WTI, but this is only due to the contract rollover. Both oil contracts have found support first and foremost from short-side profit-taking after Monday’s steep declines. It is not uncommon for some institutional investors or hedge funds to close out existing positions at the end of the month. In addition, the shutting down of the gasoline and distillate pipelines after an explosion and fire in Shelby, Alabama, has helped to ease the pressure on the energy sector as a whole. But sentiment on the oil market has turned more bearish in recent days on the back of another fruitless discussions between the OPEC and non-OPEC members that took place at the weekend. There are still no signs of a breakthrough on a coordinated production cut plan, leaving the prospects of an agreement at the cartel’s meeting on November 30 hanging in the balance. This is because a growing number of OPEC members want to be except from a production cut or even a freeze, which pretty much leaves Saudi Arabia and its allied Gulf states to shoulder the responsibility on their own. At the moment, the OPEC is pumping oil like there is no tomorrow with the cartel’s production rising to a new record high last month, according to a Reuters survey. On top of this, it is not clear what the intention of key non-OPEC oil producer Russia really is, for it has also ramped up its production to a post-Soviet high.

In short, the oil surplus is growing and unless the OPEC and Russia somehow manage to come up with a plan to reduce their output, oil prices will almost certainly come under further pressure. Even in the short-term, oil prices are in danger of falling further unless the OPEC or Russia provide us with some confidence that a deal to curb production is still forthcoming. Given this uncertainty, I won’t be surprised to see oil trading more or less side-ways until at least the November 30 meeting. In the meantime, US weekly oil inventory data should keep crude traders occupied. The American Petroleum Institute (API) will report its estimate tonight ahead of the official numbers from the US Department of Energy (DOE) tomorrow. Another unexpected inventory drawdown in the US could well serve as the catalyst for a more profound rebound in oil prices.

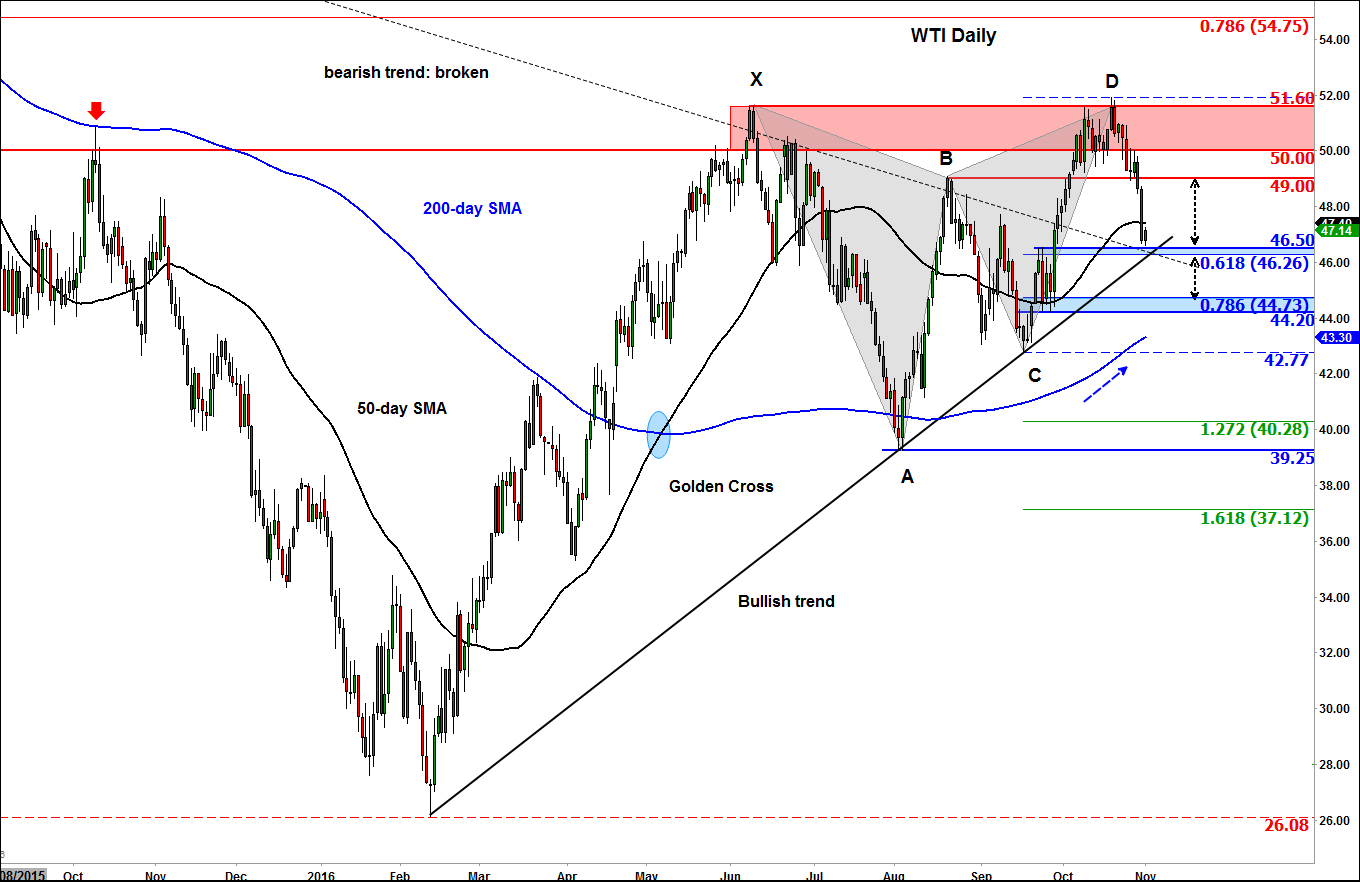

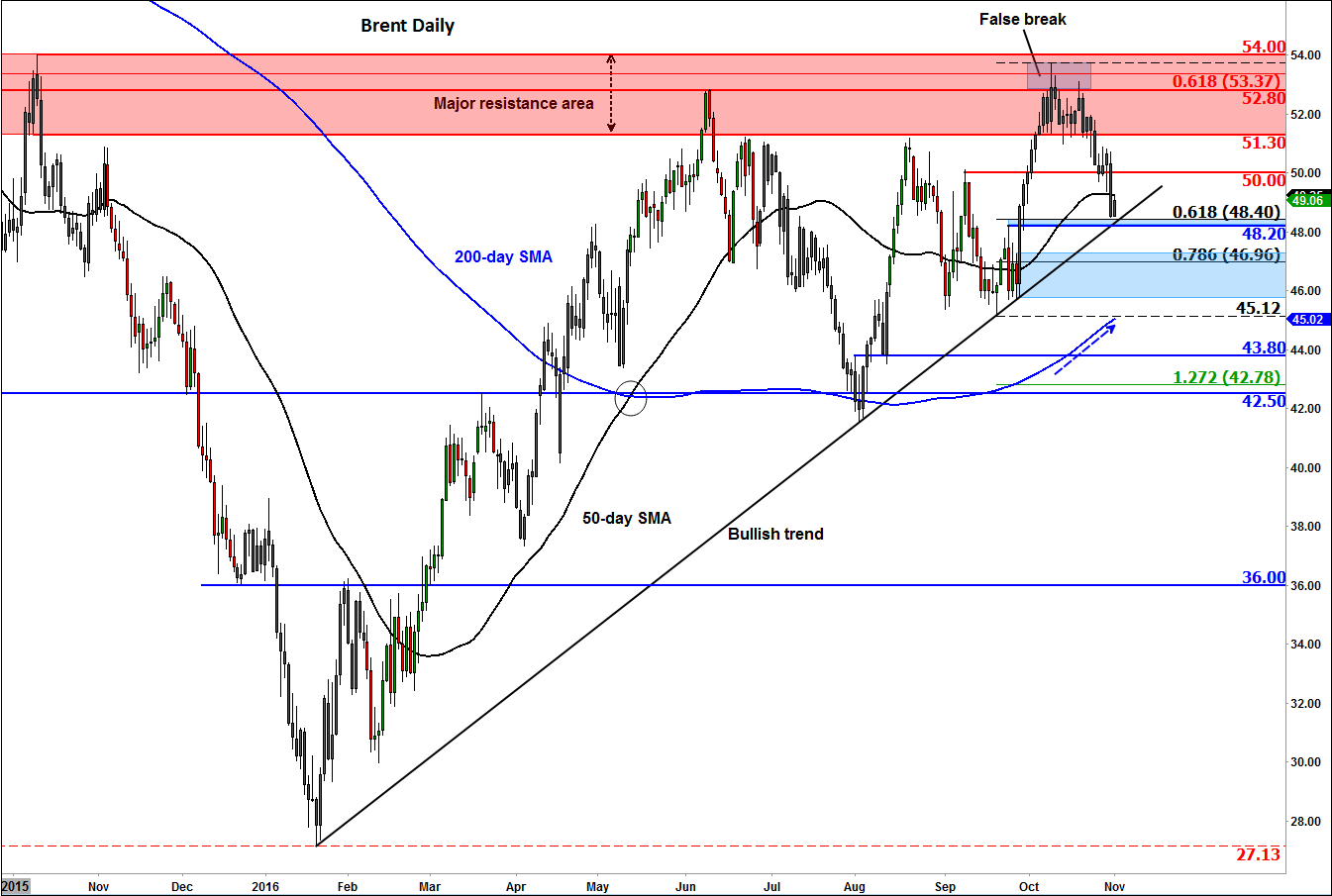

From a technical point of view, the fact that both oil contracts plunged through their respective 50-day moving averages on Monday is arguably a bearish development which could lead to further momentum-based selling pressure in the days to come. However, it should be pointed out that the most recent breaks below these averages have proved to be temporary and this could be another such occasion. Indeed, traders will need to take into account the fact that both Brent and WTI are now very close to their rising trend lines, as well as their respective 61.8% Fibonacci retracement levels and prior reference points. Thus a bounce of some sort should not come as a surprise.

Specifically, the area around $46.25-$46.50 is where all these technical factors converge on the WTI contract, while the corresponding area for Brent is around the $48.20-$48.40 range. While we are above these levels, we will still give the bulls the benefit of the doubt in terms of control. However, if these levels fail to hold for long then there is a possibility that oil prices will take sharp leg lower.