Crude shrugs off latest fall in stockpiles

Crude oil traders have ignored a stronger US dollar and have pushed prices higher at the start of this week. There has been a corresponding […]

Crude oil traders have ignored a stronger US dollar and have pushed prices higher at the start of this week. There has been a corresponding […]

Crude oil traders have ignored a stronger US dollar and have pushed prices higher at the start of this week. There has been a corresponding rally in risk assets across the board, with equities surging higher on Monday and Tuesday amid hopes that Greece will be saved from a potential default this week. Another reason why oil prices may have bounced back was probably due to some bearish speculators taking profit ahead of this week’s US oil inventories reports and as the June 30 deadline for negotiating a final nuclear agreement with Iran looms large. In addition, oil’s relatively tight trading ranges of the recent past may have unnerved the technically-minded market participants because of the fact that the consolidation has occurred near the multi-month highs, which point to a potential price breakout.

Today oil prices were little-change first thing as investors awaited the official supply numbers from the US Energy Information Administration (EIA) after the industry group American Petroleum Institute (API) had reported a 3.2 million barrel decline in stockpiles. This therefore pointed to an eight consecutive decline in inventories. As it turned out, the EIA reported this afternoon that crude stocks actually fell more profoundly, namely by 4.9 million barrels. What’s more, crude stocks at Cushing declined by an above-forecast 1.87 million barrels. Yet, WTI prices showed a negative initial reaction to the news. The reason could be that oil production edged up by 0.1 million barrels to 9.6 million and as gasoline inventories unexpectedly increased by 0.7 million barrels, which does not point to a robust driving season.

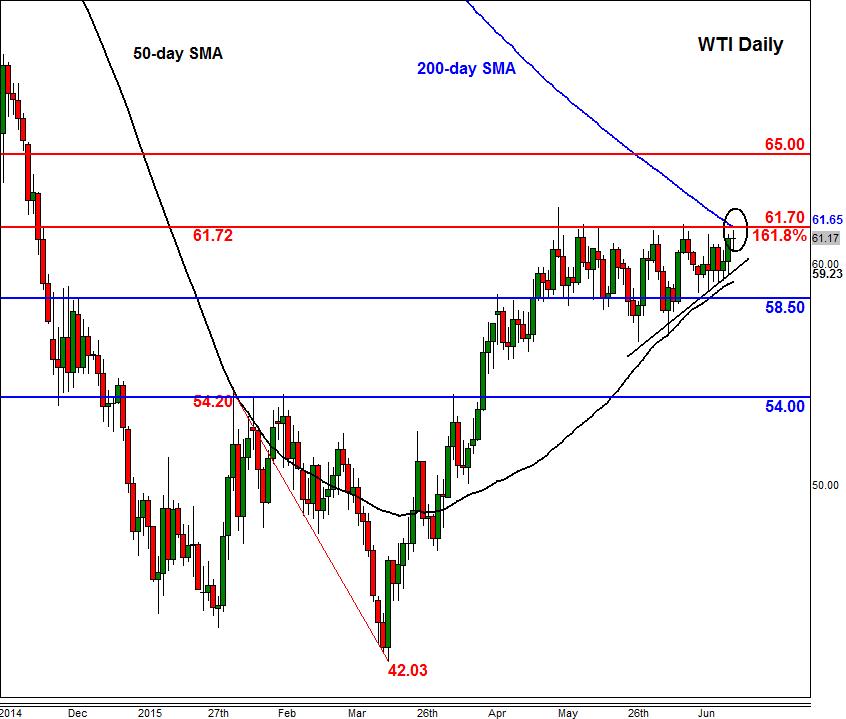

Nevertheless, today’s US supply data obviously shows that stockpiles are falling which can only be good news as it points to stronger demand. However with inventories still remaining near record levels this merely represents a drop in the ocean and it certainly won’t be a game changer. Oil prices are still in consolidation mode as the declines in US crude stockpiles are offset by supply increases from the OPEC. Oil output from Saudi, Iraq and UEA has recently risen to record levels. And although major hurdles remain in the Iran’s nuclear negotiations, the consensus is that a deal will eventually be reached, so the threat of additional oil flooding the already-saturated market is there. This may keep a lid on prices even if we see further sharp decreases in US stockpile levels over the coming weeks. In the short-term however prices may rally sharply if the bulls manage to take out the key $61.70 resistance level on a closing basis. If seen, this could give rise to further follow-up technical buying for the next several days and could easily see WTI reach and potentially surpass $65.00.