Crude short squeeze rally or bear trend resumption

The price of oil has risen for the third consecutive day. Since hitting a low of $42.20 on Monday, Brent has risen by $2.80 to […]

The price of oil has risen for the third consecutive day. Since hitting a low of $42.20 on Monday, Brent has risen by $2.80 to […]

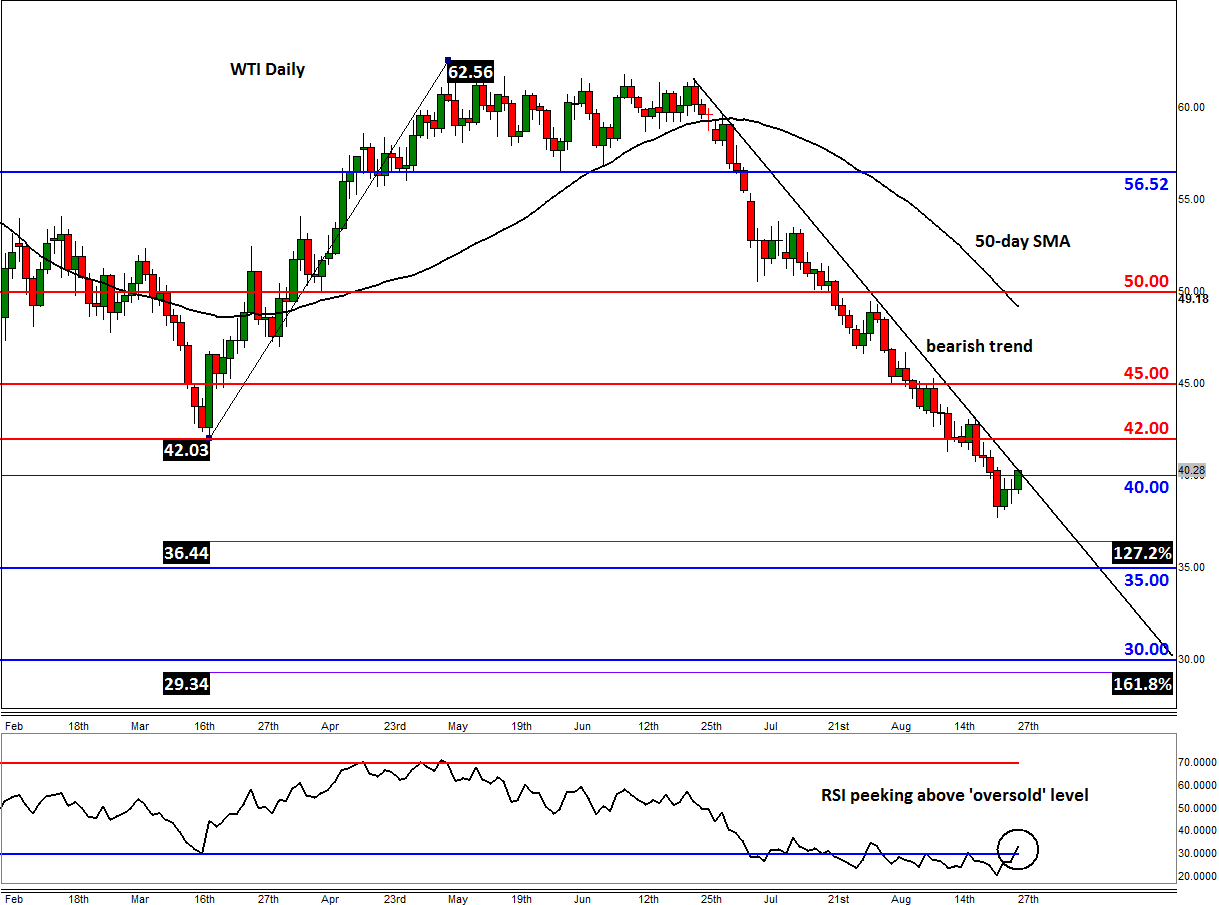

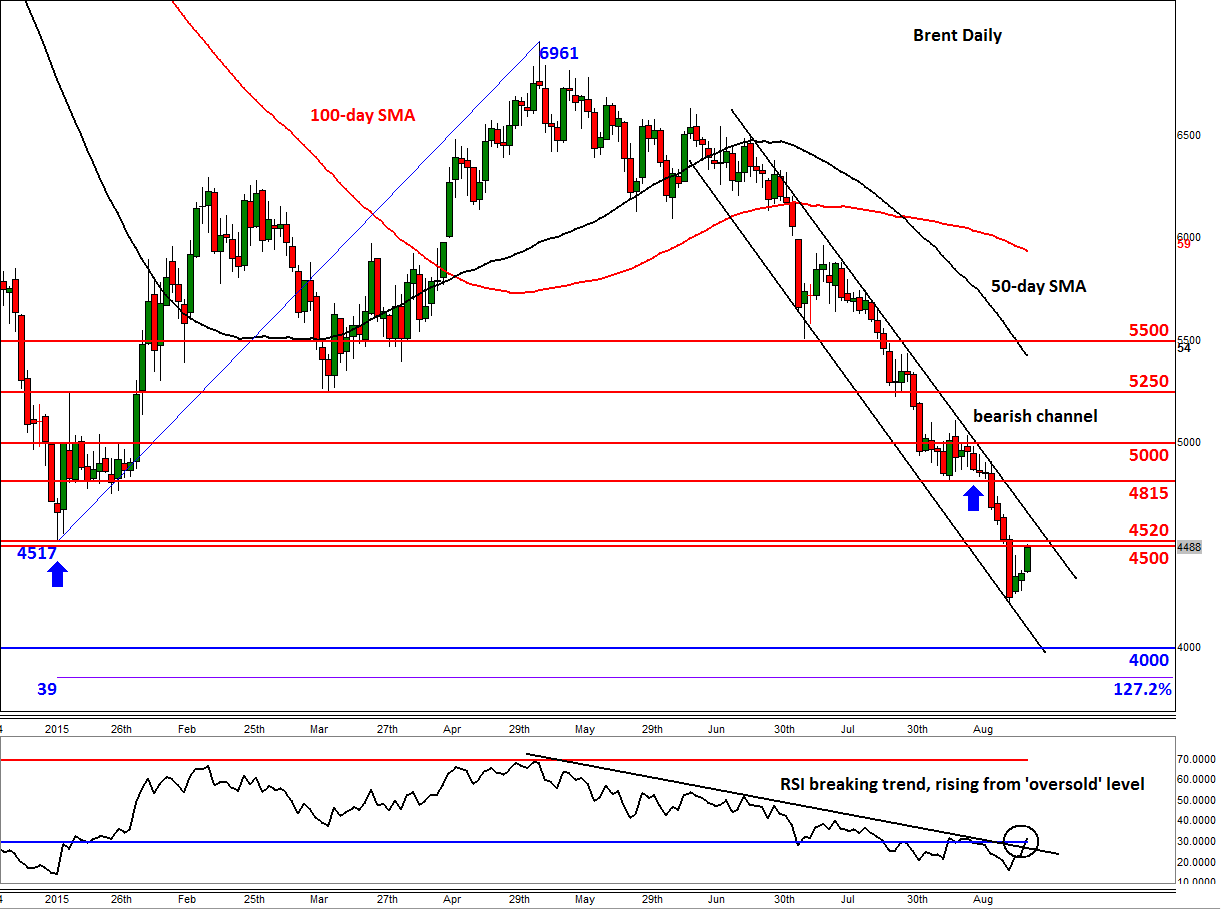

The price of oil has risen for the third consecutive day. Since hitting a low of $42.20 on Monday, Brent has risen by $2.80 to a high so for of $45.00. In percentage terms, it has gained a good 6.5%. WTI has slightly underperformed in nominal terms as it has ‘only’ gained $2.60 from its low on Monday but because it has risen from a lower base, it has outperformed on a percentage basis – up about 6.9% over the same period. More gains could be on the way if prices manage to break some key technical levels that are now being tested, though a failure at these levels could see the return of the sellers – more on this later. From a fundamental point of view however, not a lot has changed although most of the bearish news is surely now priced in. Thus the correction potential is high. The bulls will now want to see signs that the global supply glut is going to reduce. At the moment however, there are no such signs although the sharp 5.5 million barrel drawdown in US crude stocks last week was a bit of a surprise. Though the weekly change in crude stockpile levels since the start of the summer has generally been negative, the magnitude of the declines has been very modest. Indeed, the most profound weekly decrease was just 6.8 million barrels in early June. Given that we are now in the twilight of the summer driving season, gasoline demand is set to fall. The usual refinery maintenance works will further reduce demand. It is thus unlikely we will see further sharp declines in crude stockpiles levels – unless many shale producers go out of business all of a sudden. But this may only happen if oil prices remain low for a long period of time. Thus, even if oil manages to rally from these depressed levels, it is unlikely that we will see significantly higher prices for the foreseeable future.

But as mentioned, the possibility of at least a short term rally is there as some key resistance levels are being tested. As the daily chart of Brent shows, the London-based oil contract is testing $45.00/20 as resistance, an area which had offered strong support in January. If the sellers fail to defend this key technical juncture then we may see a sharp short-squeeze rally over the coming days and the buying pressure will likely gather pace if prices also break out of the bearish channel that has been in place since June. The old support levels such as $48.15 and $50.00 could be realistic targets for the bulls should we see the breakout. WTI is currently trying to break above its bearish trend line around $40.30. If the bulls succeed here, then the March low of $42.00 will be the immediate target to keep an eye on. Further resistance is seen around $45.00. Meanwhile the momentum indicator RSI is peeking above the oversold territory of 30 for both contracts and in the case of Brent it has also broken its bearish trend line.