Crude resume decline as inventories rise bad news for CAD

Crude traders have been given a rollercoaster ride. After surging some 25% in the space of just three days, prices collapsed by a huge 8 […]

Crude traders have been given a rollercoaster ride. After surging some 25% in the space of just three days, prices collapsed by a huge 8 […]

Crude traders have been given a rollercoaster ride. After surging some 25% in the space of just three days, prices collapsed by a huge 8 per cent yesterday. This morning saw both Brent and WTI contracts regain some ground but prices came under renewed selling pressure in the afternoon following the release of the official US stockpiles report from the EIA. The report showed, among other things, a sharp build of 4.7 million barrels in stockpiles for the week ending August 28. Although the initial reaction has been negative, prices are still holding above yesterday’s lows at the time of this writing, partly due to the fact that the build was still below the 7.6 million barrel increase that had been reported by the American Petroleum Institute (API) last night. Nevertheless, the unexpectedly sharp build reminds traders about the excessive supply of the stuff in the US, which should continue to weigh on prices for the foreseeable future. Oil inventories are unlikely to be reduced meaningfully in the short term because not only is the summer driving season coming to an end but there is also the usual refinery maintenance works that will take place soon, meaning weaker demand – particularly for gasoline. In fact, the demand outlook for crude oil remains bleak judging, for example, by the latest PMI data out of China, Europe and the US.

If oil prices extend their falls today or later in the week then it could be bad news for commodities currencies such as the Canadian dollar. Thus, there may be plenty of trading opportunities to look forward to on the USD/CAD and CAD crosses, if not on the underlying crude oil prices themselves. One interesting pair that has caught my attention is the GBP/CAD. Following the recent correction, there is now potential for the cross to resume its long-term upward trend, particularly if the pound also finds some support now. Tomorrow’s UK services PMI report should therefore be watched closely, along with the direction of oil prices. From Canada, the key data will be the employment figures that are released at the same time as the US nonfarm payrolls data on Friday afternoon.

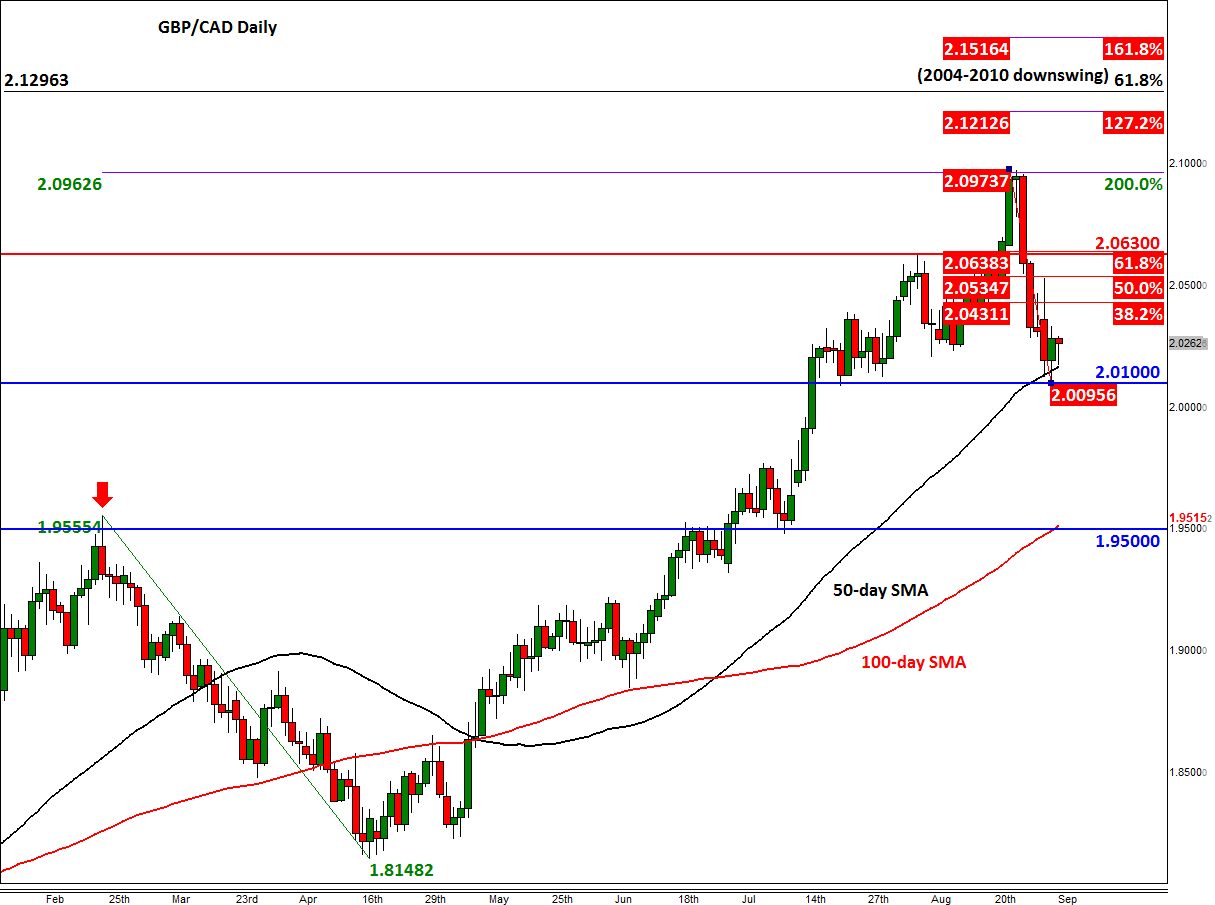

From a technical point of view, the GBP/CAD has fallen sharply ever since reaching the 200% extension level of the correction we saw between February and April, at 2.0960 on August 24. From there, the cross has fallen to a low so far of 2.0095, shedding in the process some 850+ pips or 4.1 per cent. But at the start of this month, the buyers have shown their presence once more around the key technical level of 2.010. As well as prior support, this level corresponds with the 50-day moving average. As a result, there is a chance for price to rally back towards the 61.8% Fibonacci and old resistance level at 2.0630, before it decides on its next move. But a top may have already been established, so while price remains below last month’s high, bullish traders should proceed with extra caution. Meanwhile there is also the potential for a 500+ pip drop towards the previous resistance-turned-support at 1.9500 should the cross take out the aforementioned 2.0100 support. Thus expect volatility to remain high in this pair, which should mean lots of trading opportunities.