Crude OPEC unlikely to cut production quota

The official OPEC meeting is underway in Vienna and crude oil prices are trading in tight ranges as the market awaits a decision. A division […]

The official OPEC meeting is underway in Vienna and crude oil prices are trading in tight ranges as the market awaits a decision. A division […]

The official OPEC meeting is underway in Vienna and crude oil prices are trading in tight ranges as the market awaits a decision. A division within the cartel is clearly visible with Saudi Arabia and Gulf countries wanting to maintain production quota unchanged, while the rest, most notably Venezuela, favouring a reduction in order to shore up prices to help support their struggling economies. Saudi would have considered a cut if certain non-OPEC members like Russia also agreed to reduce their crude oil output. This is a bizarre request and unlikely to be agreed upon. Iran’s oil minister wants everyone to cut their production apart from his country. With so many members in disagreement, an eventual decision will undoubtedly not be unanimous.

Ultimately, it will be the OPEC’s most influential member, Saudi Arabia, who will decide on what’s in the best interest of the cartel and more importantly Saudi Arabia itself. It would surprise me if the decision was anything but to continue defending its share of the market and producing similar amounts of oil going forward. At the moment, the cartel is producing way more than the daily required target of 30 million barrels, and with Indonesia set to re-join the OPEC, this limit may actually be increased. It should be noted however that this will not have a net impact on global supply, as either with or without the cartel Indonesia would be producing the same amount of oil. The other problem for the OPEC is of course Iran, which is ready to increase its production immediately after more sanctions are lifted. All in all, the OPEC meeting is likely to conclude with a decision that would favour defending market share.

Thus the surplus is likely to remain in place for longer, which should not be good news for oil prices. As we have said before, given the current circumstance, the best outcome for the OPEC might actually be if oil prices stayed depressed for a bit longer. This could force some weaker oil producers out of the market and the consistent falls in the rig counts does certainly point in that direction for US producers. So the oil market could begin to tighten sharply at some point next year. But the on-going supply surplus should continue to exert heavily pressure on oil prices in the short term and as such any price gains should be treated with extreme caution.

But even if the OPEC decides to maintain production target unchanged, one should not expect to see a massive slide in oil prices as after all, this outcome is mostly priced in. Thus, oil could fall by a few dollars at the very most, in our view, on Friday, before it stalls and decides on its next move.

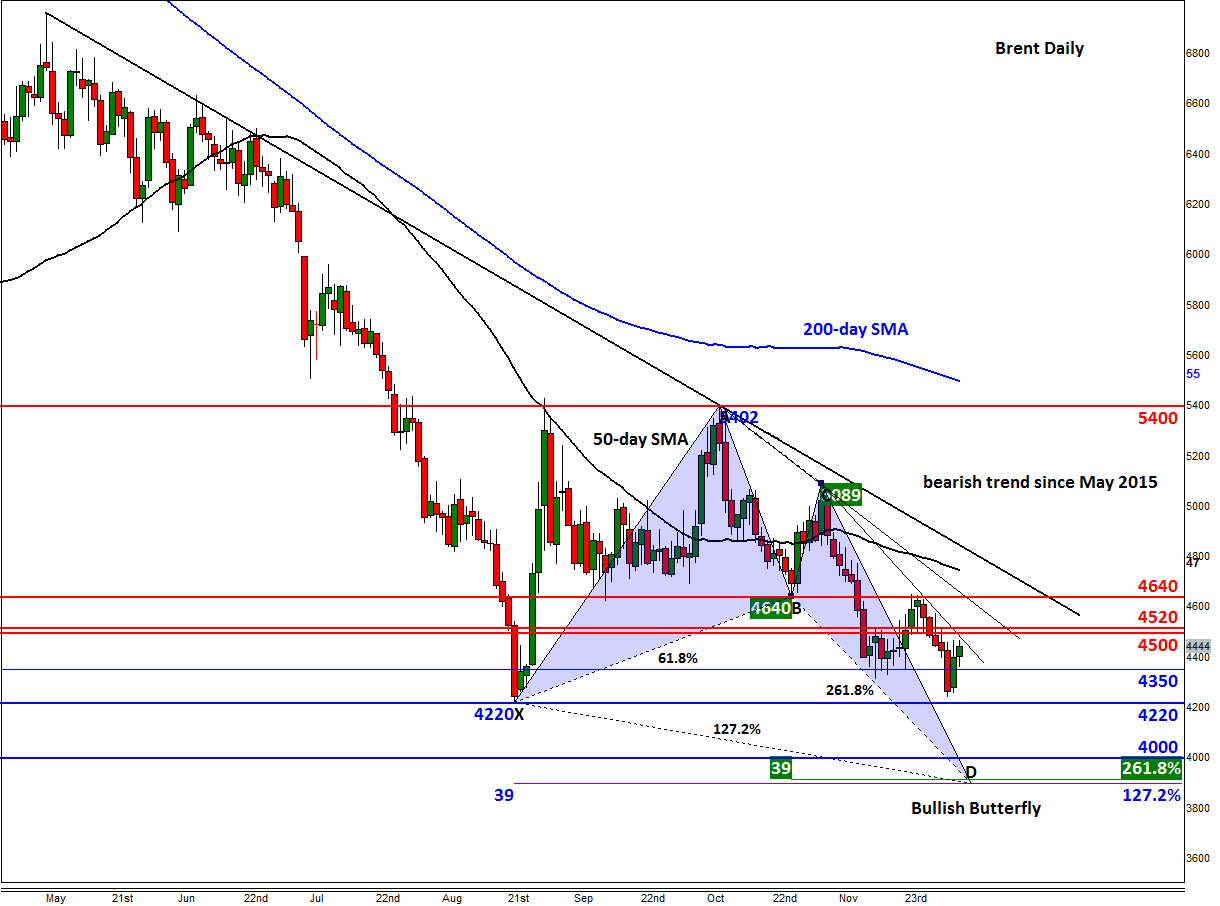

With the bearish trends still in place for Brent, the technical outlook continues to remain bearish until proven otherwise. Some key resistance short-term resistance levels are also approaching around $44.65/70, $45.00/20 and $46.40. The key level on the downside is this year’s low around $42.20, followed by the psychologically important $40 handle. If these levels break, Brent may drop to the Fibonacci converges area around $39.00 before potentially bouncing from there as the shorts take profit. The $39.00 level is also the extended point D of an AB=CD move, so it represents a Bullish Butterfly pattern, which can sometimes pin-point the exact top, and in this case, bottom.