Crude oil struggles to shake off oversupply concerns

Oil prices have been extremely volatile of late, without making any significant progress in either direction. The long and short of it is that the […]

Oil prices have been extremely volatile of late, without making any significant progress in either direction. The long and short of it is that the […]

Oil prices have been extremely volatile of late, without making any significant progress in either direction. The long and short of it is that the stream of mostly negative news has helped to halt the recent rally, while ahead of this month’s informal meeting of the OPEC in Algeria not many people will want to be betting boldly on an oil price plunge. Therefore consolidation is the dominant theme in the oil market at the moment, with a slight bearish bias due to the ongoing oversupply concerns.

Indeed, there has been more negative than positive news on the oil markets recently. According to the International Energy Agency (IEA), for example, the global oil market will not balance until mid-next year as demand in 2016 grows by 100,000 barrels per day less than previously anticipated while at the same time non-OPEC supply is likely to be 100,000 bpd higher both in 2016 and 2017. The IEA has also estimated that the OPEC expanded its production to 33.5 million bpd in August. The cartel’s oil production has therefore risen significantly compared to a few months ago and had it not been for this, the market would have been a lot tighter or even balanced by now.

Bullish oil investors are now hoping that the OPEC and Russia will come up with a plan to halt the relentless increases in crude production, and see some destocking in US oil inventories which remain near record high levels.

Last week, both the American Petroleum Institute (API) and the Energy Information Administration (EIA) reported surprisingly large drawdowns in crude stockpiles as imports dropped. Naturally, oil analysts expect to see a rebound and that’s exactly what the API reported last night. That being said, the 1.4 million barrel increase was half the amount expected. In addition, crude stocks at Cushing fell by 1.1 million barrels while gasoline inventories dropped by a sharp 2.4 million barrels. So you could say that the report was bullish for oil, not that prices have actually responded that way…yet.

If the official data from the EIA, due out later this afternoon, confirm or beat the API figures then we may see oil prices stage a bounce of some sort after all. But there are a few warning signs that suggests the contrary. For example, WTI has more than gave up the sharp gains made on the back of last week’s US oil inventories reports. Oil’s failure to hold onto those gains clearly suggests that the market participants have treated last week’s data as outlier rather than game changer. More evidence is needed to be seen before investors start believing that the tide has turned from rising to now falling oil inventory levels. Until that happens, WTI is unlikely to stage a sustainable rally – unless of course the OPEC blinks first and agrees (and sticks) to a lower production quota.

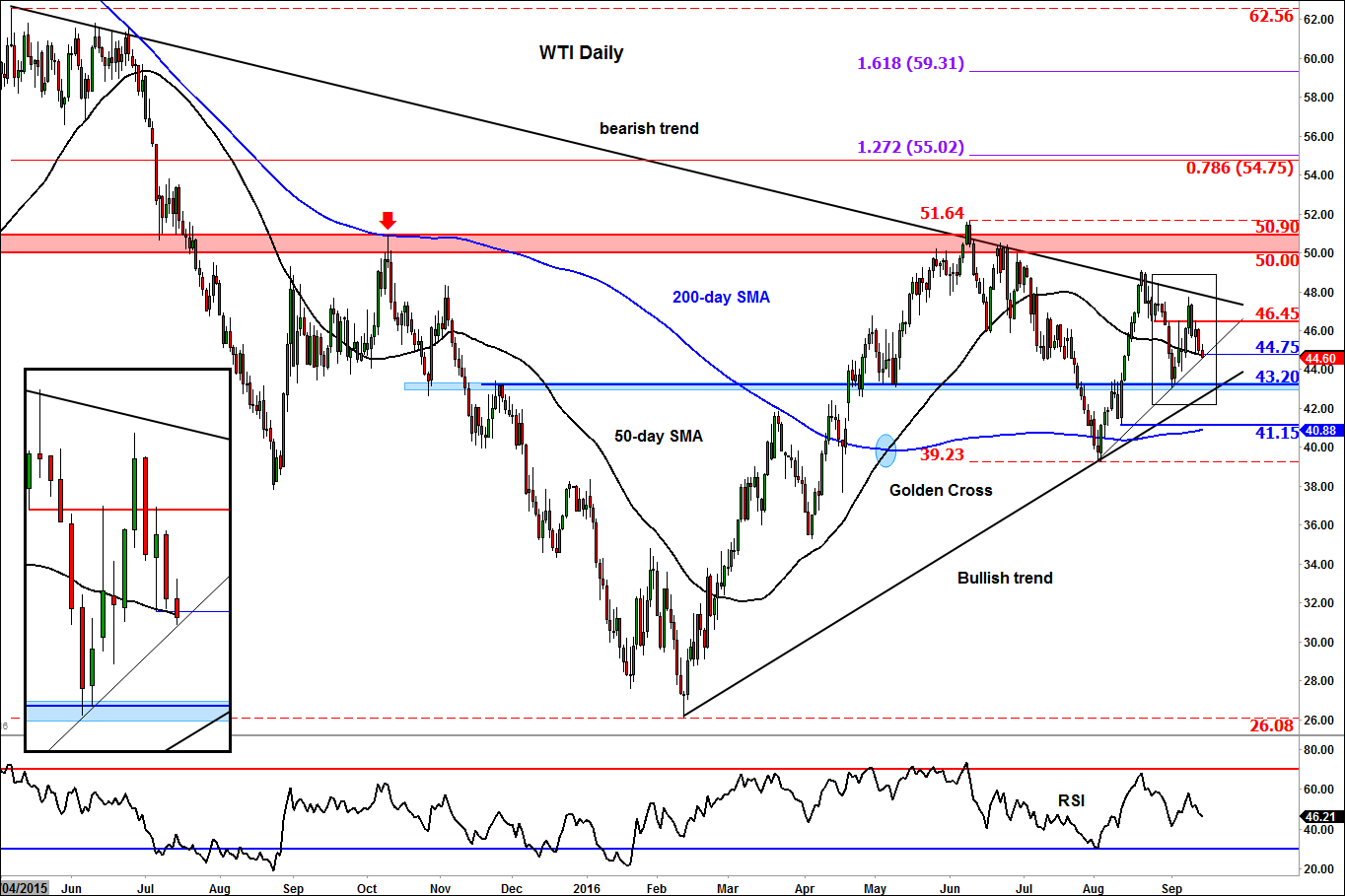

There’s not much we can glean from looking at WTI’s daily chart, except that the trend lines are converging fast and that a break out or a break down is forthcoming. Some of the key levels to watch are shown in blue (support) and red (resistance) on the chart.