Crude oil slumps

A correction of some sort in crude oil prices seemed inevitable and this may well have started today with both contracts falling nearly 4% each. […]

A correction of some sort in crude oil prices seemed inevitable and this may well have started today with both contracts falling nearly 4% each. […]

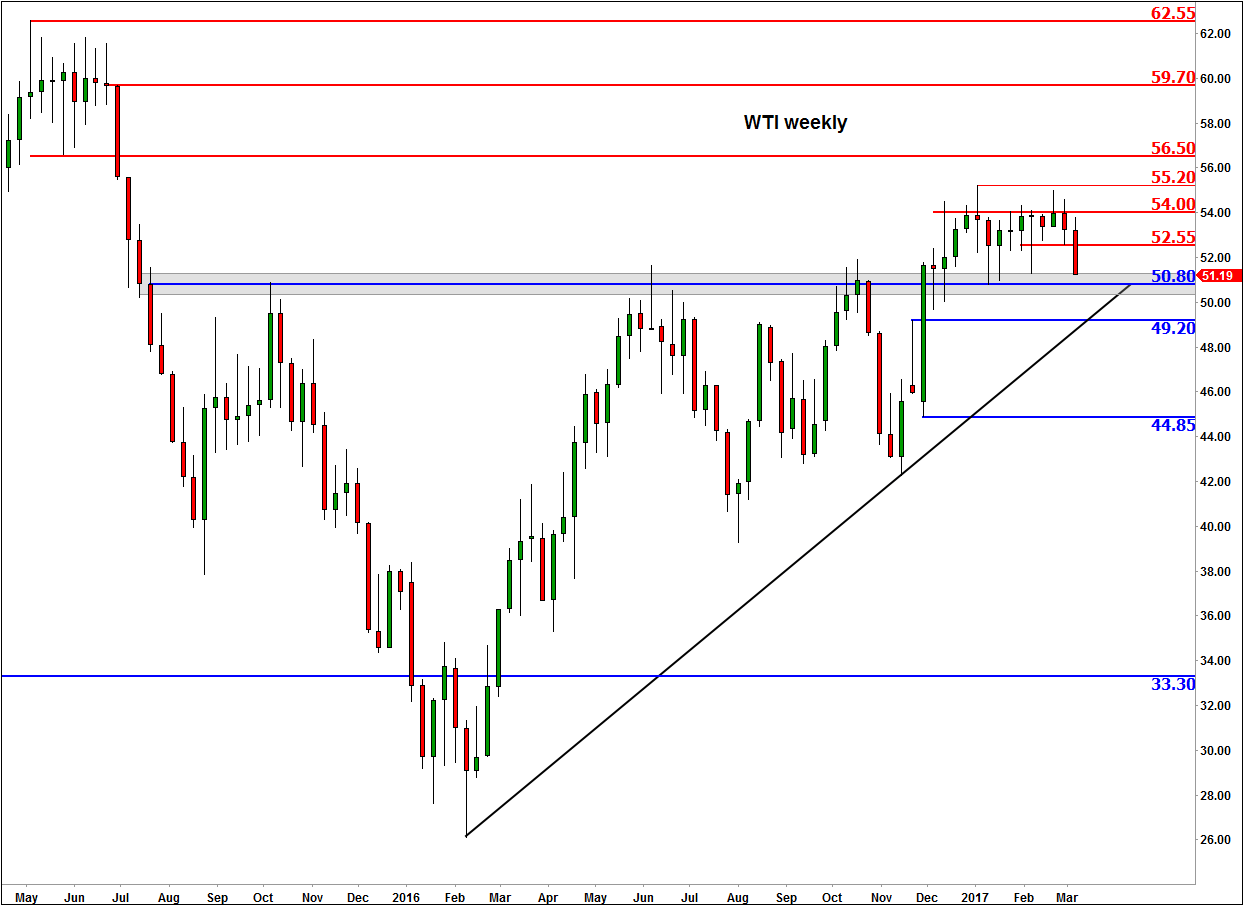

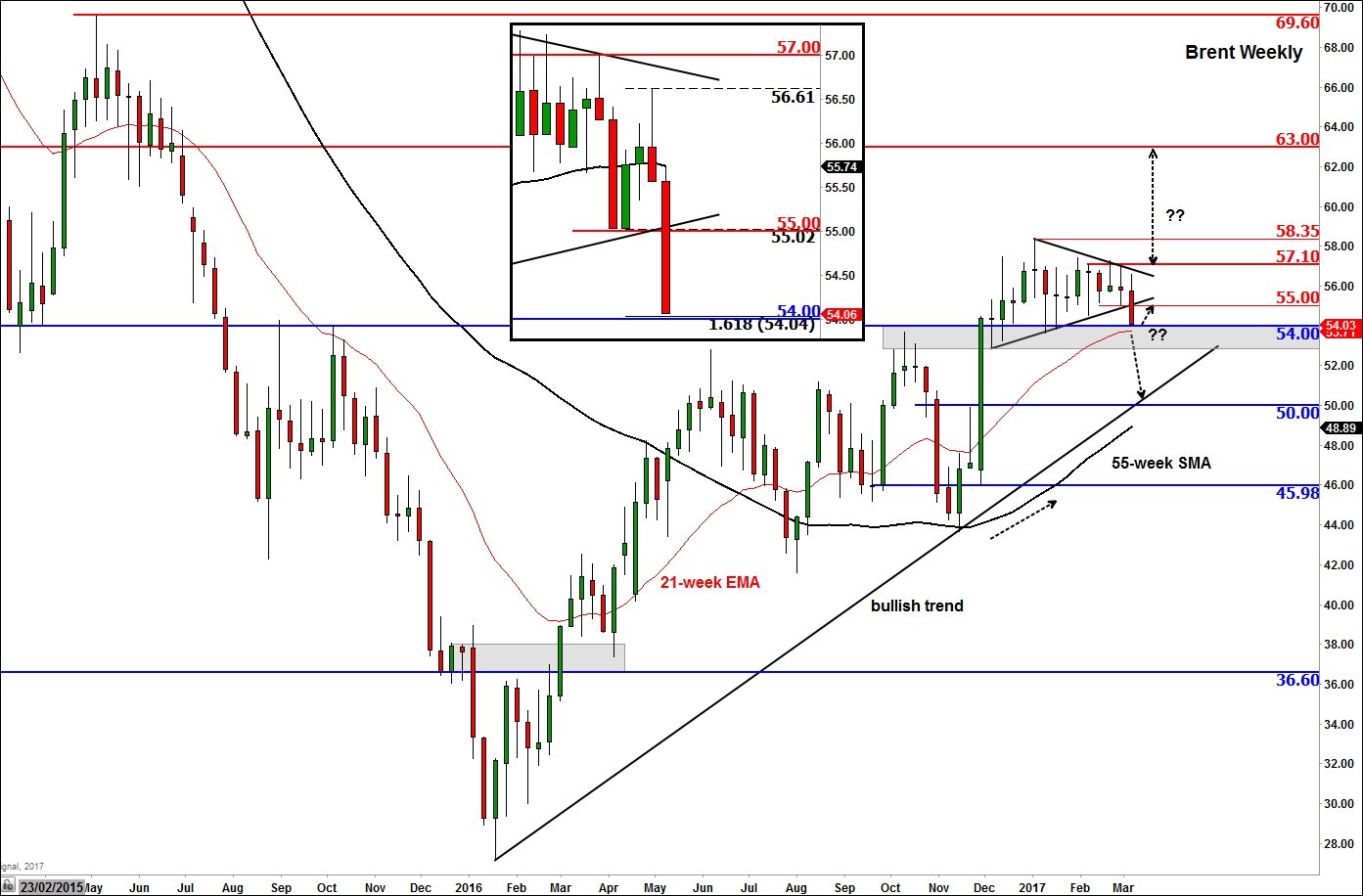

A correction of some sort in crude oil prices seemed inevitable and this may well have started today with both contracts falling nearly 4% each. As we reported the possibility on Friday, Brent has fallen to $54 and WTI to $51 a barrel. The rising crude inventory levels in the US to new all-time highs has been the number one reason why prices have been unable to move further higher after the OPEC had agreed with some non OPEC members to limit production back in November. Expecting higher oil prices, money managers and other large speculators have been increasing their bullish bets to record high levels – until last week. As we had anticipated, these market participants sharply reduced their long positions last week, as evidenced by the latest positioning data from both the CFTC and ICE. They are likely to have further reduced their holdings following today’s oil price drop.

Today’s big drop in oil prices was hardly surprising. According to the US Department of Energy, oil inventories rose by a much larger-than-expected 8.2 million barrels last week to a new record level. This was the ninth consecutive weekly rise. Crude production has meanwhile climbed to a new 13 month high. Not all aspects of the oil report were bearish, as stocks of gasoline saw an unexpectedly sharp drop of 6.6 million barrels – the highest drawdown since April 2011. But this failed to offer any support.

As a result of rising US oil production, the OPEC is losing market share. But surely they won’t do a U-turn now. Their response may very well be a continuation of corporation to limit their oil production, perhaps for a little longer than they had hoped. This should help keep a floor under oil prices. Indeed, despite today’s sharp sell-off, I remain bullish on oil and still expect to see $60-$70 a barrel by the year end. As before, the key risk to this view would be if we see an acceleration in US oil production relative to the demand growth. In such a scenario, oil prices will struggle to get very high.

As we go to press, both oil contracts were testing their long-term support levels: Brent at around $54 and WTI at around $51. While a breakdown below these levels may be forthcoming, given the size of today’s price drop I wouldn’t be surprised if the sellers booked some profit at or around these levels now, potentially leading to a short-covering bounce later on. It is possible for prices to test the liquidity zones below these levels before potentially bouncing back. But until we see distinct reversal patterns, the short term path of least resistance is to the downside on both contracts now. The long-term bullish trends would technically end if and when oil prices create significant lower lows.