Crude oil prices gushing higher

WTI crude oil prices surged higher at the start of the week before falling slightly on Wednesday on the back the latest weekly EIA crude […]

WTI crude oil prices surged higher at the start of the week before falling slightly on Wednesday on the back the latest weekly EIA crude […]

WTI crude oil prices surged higher at the start of the week before falling slightly on Wednesday on the back the latest weekly EIA crude oil stocks data which showed a surprise build of 3.1 million barrels for the week ending October 2. But speculators have been quick to dismiss that small but noticeable rise on seasonal factors, as after all the end of the summer driving season means there will always be less demand for gasoline at this time of the year. Indeed, gasoline stocks did in fact increase by 1.9 million barrels that week, pointing to reduced demand. Oil refineries also carry out their usual maintenance works at this time of the year and ahead of the winter months – hence the notable fall in the refinery utilization rate.

Many investors are starting to believe that US shale oil output is going to be reduced noticeably and are thus betting that prices will recover from these depressed levels as the global glut is slowly reduced. The CFTC’s positioning data should confirm this when the markets close for trading this evening. Inventors’ growing confidence on the oil market was given an additional lift by comments from the OPEC’s Secretary-General Al-Badri who said that oil demand will climb more this year than previously projected (by 1.5 million barrels a day), and as the EIA predicted that global oil companies will cut investments in crude exploration and production by 20% this year. Russia’s controversial and apparently imprecise bombardment of IS targets in Syria is further heightening the geopolitical risks in the Middle East region and this is also helping to push oil prices higher.

In addition, the dollar weakness has persisted after the FOMC’s September meeting minutes did not provide any major surprises. This is providing a boost to the buck-denominated commodities across the board with gold also climbing above a major resistance area as we end a very good week for commodities. Equities are also pushing higher ahead of the third quarter earnings seasons and on growing expectations that the Fed will hold off raising rates until next year, giving the “risk-on” trade a further boost.

The sentiment on the oil market is therefore improving. So, we could see further gains early next week, provided of course we don’t see any nasty surprises – for example, from Baker Hughes’ rig count data this evening or China’s macro numbers next week.

From a slightly longer-term view point however it is questionable how far this rally will go because the excessive supply of crude is unlikely to be removed meaningfully any time soon. Increased production from the likes of Iran, Libya and Russia to name but a few will probably offset the expected production cuts in the US. Indeed, if oil prices rise significantly then it is easy for US shale companies to ramp up production once more.

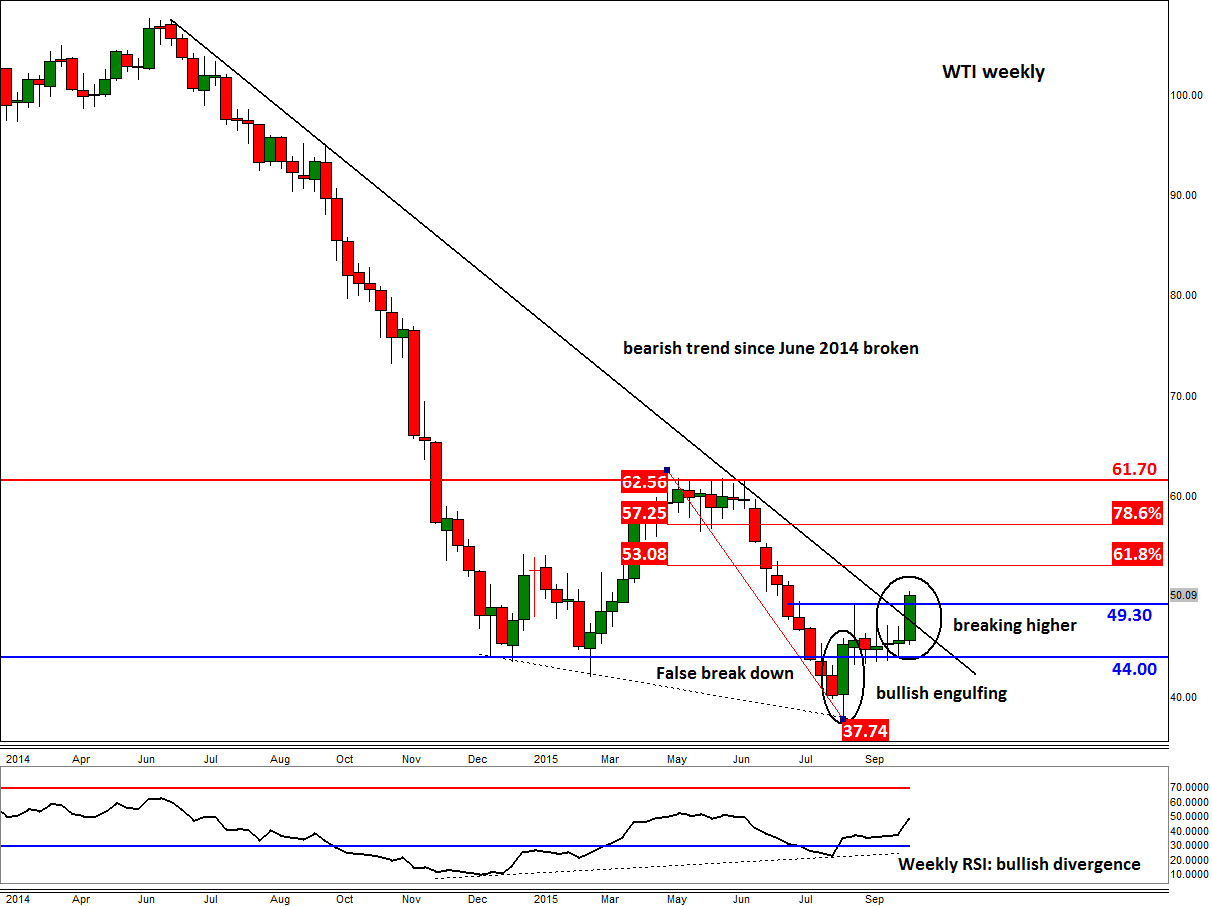

Nevertheless, the short-term positivity in the oil market has been accompanied by a major technical breakthrough this week as WTI has finally broken down its bearish trend line that has been established since prices peaked in the summer of last year. WTI has also broken above the August high of $49.30, thereby confirming the trend breakout and the false breakdown reversal pattern that had occurred earlier that month. As things stand therefore, WTI could easily reach its 200-day SMA at just below $51 (not shown on the chart) before climbing towards the Fibonacci levels of the downswing from the summer of this year around $53.05 (61.8%) and $57.25 (78.6%). The major resistance and this year’s high reside around $61.70/$62.55.

The short-term bullish outlook will become questionable if WTI oil prices fall back and hold below the old resistance level at $49.30 and completely invalid on a potential break below $44.00.