Crude oil and the supply demand situation

The International Energy Agency (IEA) stated on Wednesday that the global glut in crude oil will likely persist through 2016, even as demand is projected […]

The International Energy Agency (IEA) stated on Wednesday that the global glut in crude oil will likely persist through 2016, even as demand is projected […]

The International Energy Agency (IEA) stated on Wednesday that the global glut in crude oil will likely persist through 2016, even as demand is projected to grow at more than twice the rate of last year’s growth due to low prices stimulating consumption. If this scenario comes to fruition, it would constitute the strongest demand growth in five years.

This positive outlook on global oil demand, despite persistent oversupply and overproduction conditions, provided some tentative support for crude oil prices on Wednesday after the West Texas Intermediate (WTI) benchmark for US crude on Tuesday hit its lowest level since March’s six-year low around 42.00.

While this report from the IEA paints a rather optimistic picture, at least on the demand side of the equation, China’s currency devaluations of the past two days have put into question whether demand from the world’s largest oil importer would be sustained in the face of higher costs for dollar-denominated oil and an apparently troubled economy. Despite these challenges, however, low oil prices may well prove to be too good a bargain to pass up for a China that continues in its relentless quest to stockpile strategic oil reserves.

Therefore, while overall global demand for oil may not be projected to diminish substantially, and in fact may increase over the next year, the question again comes back to oversupply. On Tuesday, OPEC reported close to record levels of production for July, as the organization’s Persian Gulf members continue to staunchly refuse a cut-back on production. This comes as US shale production also remains stubbornly high and a potential lifting of Iran sanctions could flood the market with even more crude oil.

The Energy Information Administration also reported on Wednesday that US crude oil inventory fell last week for a third week in a row. Despite the drop of 1.7 million barrels last week, however, the decrease was largely in-line with expectations, and therefore did not affect oil prices substantially.

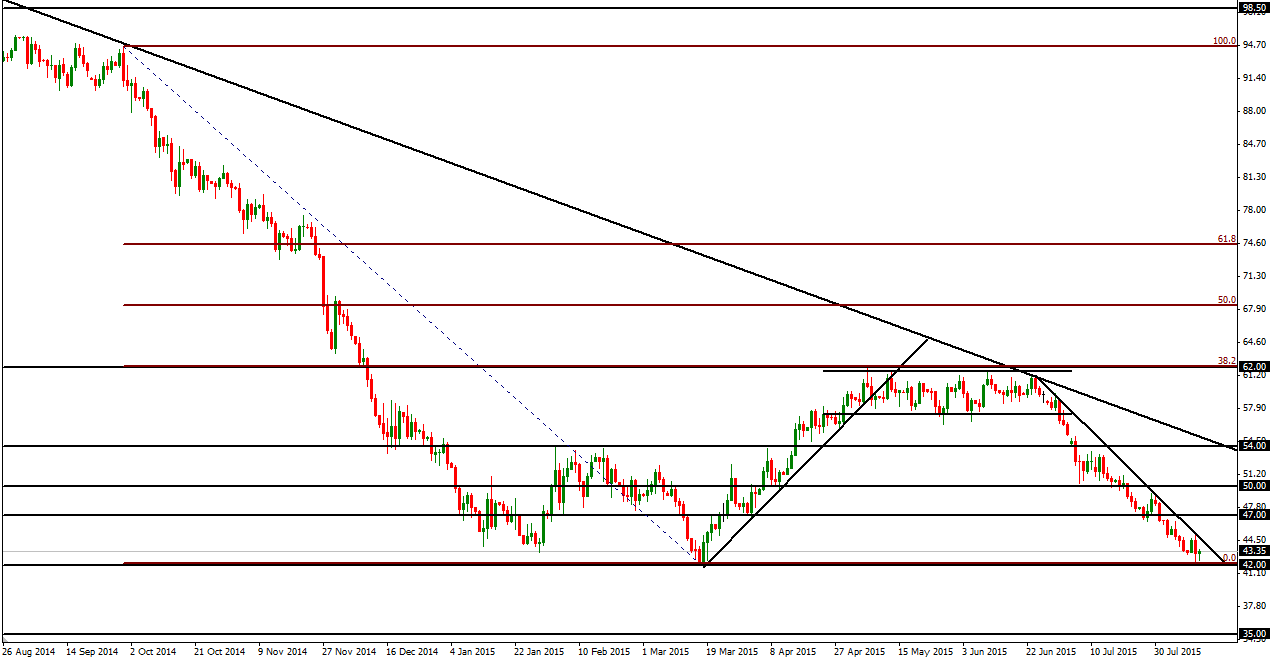

From a technical perspective, WTI has essentially formed what could be viewed as a double bottom pattern, but only if a rebound or relief rally occurs from around the current support levels. This places the price of US crude oil at a critical technical juncture. In the event of this rebound, upside targets reside around the 47.00 and 50.00 levels. More likely, however, persistent oversupply conditions should likely lead to a further fall to continue the plunge of the past month and a half before any appreciable recovery occurs. In the event of a breakdown below 42.00 support, the major downside target resides at the 35.00 level, last approached in late 2008.