Crude off highs as traders weigh impact of Canada fire Saudi s new oil chief

At the start of this week, oil prices found themselves sharply higher with Brent almost reaching $46.50 and WTI $46 a barrel overnight. Support for […]

At the start of this week, oil prices found themselves sharply higher with Brent almost reaching $46.50 and WTI $46 a barrel overnight. Support for […]

At the start of this week, oil prices found themselves sharply higher with Brent almost reaching $46.50 and WTI $46 a barrel overnight. Support for oil prices is coming from Canada due to the ongoing wildfires, which has reportedly reduced the nation’s daily crude output by a fifth already. Unfortunately it could take a very long time before the fire is brought under full control so its impact on oil production remains unclear. But this is obviously a temporary factor so it won’t have a long-lasting impact on prices. Both contracts eased off their highs by midday in London. The sacking of Saudi’s Ali al-Naimi as head of the country’s oil ministry may be a reason why oil prices have failed to maintain their early advance. Al-Naimi’s successor, Khalid al-Falih, the former head of the state-owned Aramco, is largely expected to follow the strategy of protecting the nation’s market share. This has further reduced the likelihood of an oil-freeze deal with other large non-OPEC producers like Russia.

In fact, oil prices haven’t moved much since the start of May. Profit-taking was largely the reason behind the oil price declines since the end of April after speculative net long positions had risen to record levels in the preceding weeks. Indeed, the CFTC’s latest positioning data on Friday revealed that bullish bets on WTI oil prices dropped for the first time in three weeks and short positions rose in the week to May 3. The selling continued in the early parts of last week, though prices recovered as the week wore on. The impact of another build in US oil inventories was offset by concerns about disruptions to oil supply in Canada – as a result of the wildfire in Fort McMurray, the country’s oil sands hub. Friday’s disappointing US jobs report saw traders revise their expectations about a rate increase further out, triggering a “risk on” rally from which oil also benefitted.

Essentially, though oil prices still appear to be in an upward trend. It is expectations about a tighter global oil market this year that has been driving prices from the multi-year lows hit in February. Above all, the declines in US shale oil production look set to continue for some time yet as the rig counts continue to fall. According to Baker Hughes, another 4 US oil rigs were taken out of operation last week. In April, the average US rig count was 437, down 41 from the previous month and a huge 539 from April 2015. But it is not just the North America where oil rigs are falling. The international rig count (which excludes the US and Canada) fell by 39 in April compared to March, led by a drop of 15 rigs in Latin America.

But as oil prices trade near the lower band of the levels that many think will put the brakes on the decline in US oil production (namely around $50-$70 a barrel), it will be interesting to monitor the changes in the weekly oil rig counts in the coming months. Actual oil production will obviously also respond to higher prices but with a longer lag. If we start to see a slowdown in the decline in oil rig counts in the coming months then this may provide an early indication that oil prices are about to hit a medium term peak. Conversely, if the relentless declines continue then it would strongly suggest that prices may rise towards $70 or so before peaking.

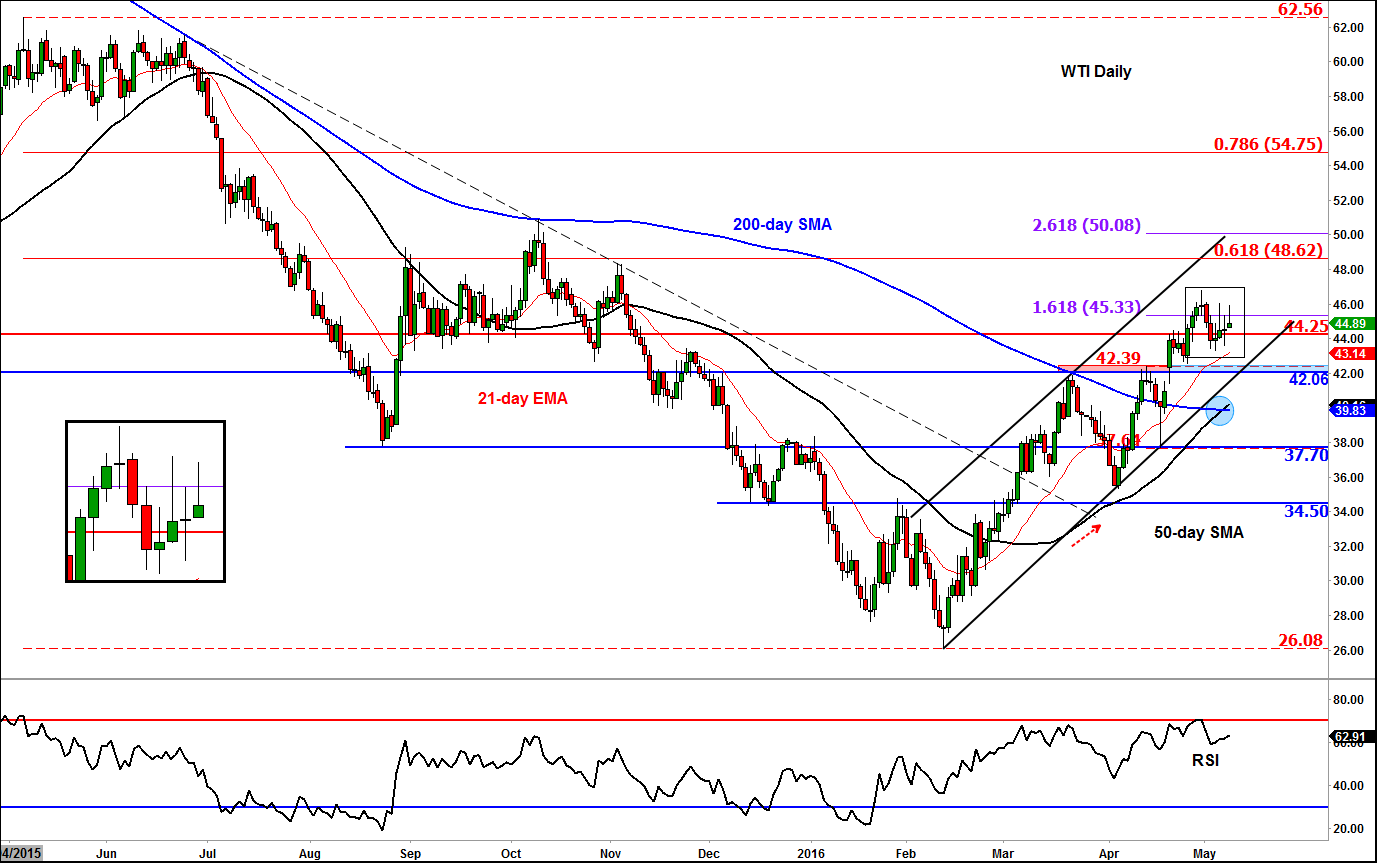

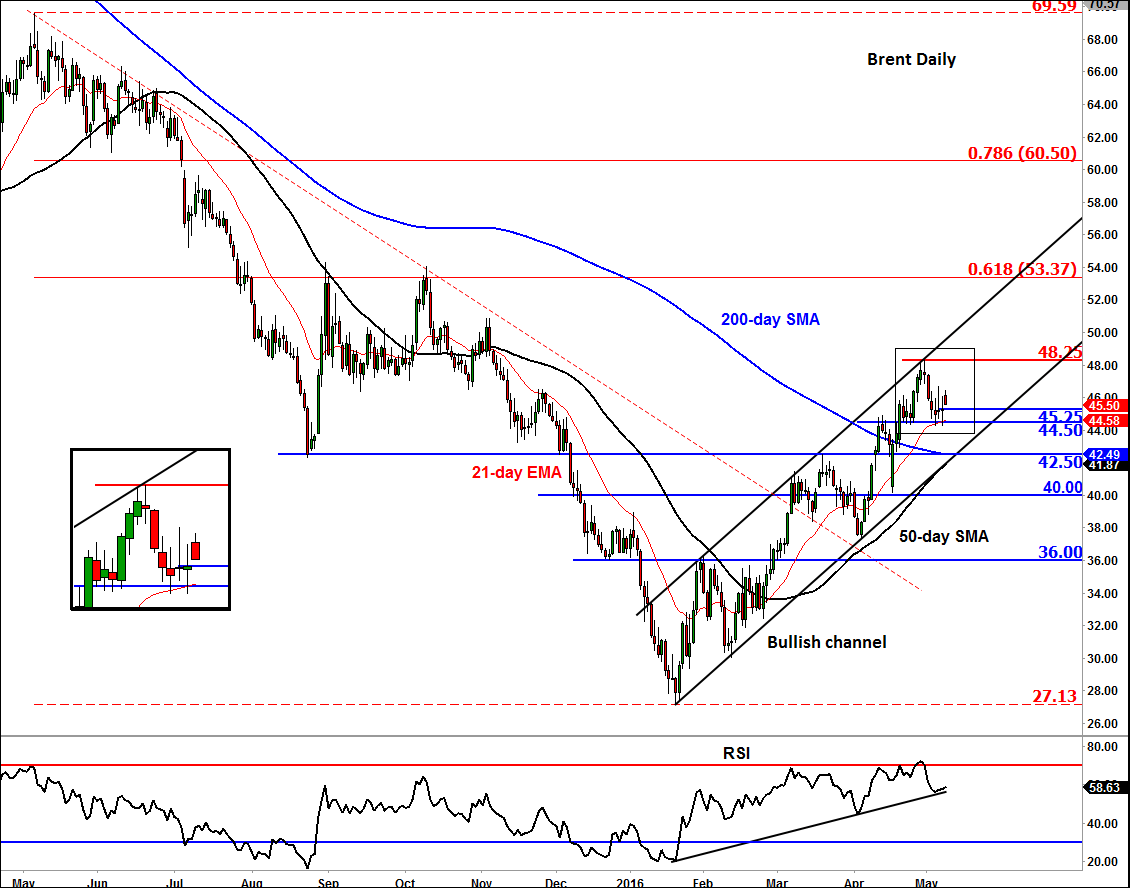

However the path of least resistance remains to the upside for now as both oil contracts remain inside their bullish channels and above key support levels as shown on their charts, below. WTI’s 50-day moving average has now crossed above the 200 to create a “Golden Crossover.” Meanwhile, Brent’s RSI has now worked off “overbought” condition, potentially paving the way for another rally this week, assuming that the key short-term support at $44.50 will hold. If this breaks however, we may see a drop towards $42.50, the support trend of the bullish channel and the 200-day moving average.