Crude may struggle to rise further ahead of Russia OPEC meeting

The long wait for the much-anticipated Russia-OPEC meeting is almost over. The general feeling is that an agreement will be reached on Sunday in Doha […]

The long wait for the much-anticipated Russia-OPEC meeting is almost over. The general feeling is that an agreement will be reached on Sunday in Doha […]

The long wait for the much-anticipated Russia-OPEC meeting is almost over. The general feeling is that an agreement will be reached on Sunday in Doha to freeze oil production at January’s levels, with or without Iran’s participation. This outcome is mostly priced in but will still likely give prices a further short term boost. However, will it be a classic case of “buy the rumour, sell the fact” type of a reaction on Monday? Time will tell. In addition, there is a risk that they will fail to find an agreement, in which case oil prices could gap lower at the open on Monday. Given this uncertainty, I would expect at the very least for oil prices to pause at these relatively elevated levels going into the meeting.

In any case, I think the market will be quick to look beyond this Russia-OPEC meeting and focus on the US where oil production has been falling somewhat of late. If further evidence emerges in the coming weeks that point to a more balanced oil market later in the year then prices could further extend their gains. But at the moment the market is oversupplied and US oil inventories are still near record high levels. After last week’s surprise drawdown in US oil stocks, many people were hoping to see another fall or a small build at worst. As it turned out, the Energy Information Administration (EIA) reported a large 6.6 million barrel build from the previous week. This was expected however after the American Petroleum Institute (API) had reported a similar number on Tuesday evening. Also, the sharp drawdown of gasoline stocks (4.2 million barrels) kind of offset the headline increase.

Consequently, oil prices struggled for direction on Wednesday afternoon. Even if prices go on to push higher, I would expect to see some profit-taking in the next couple of days ahead of the Russia-OPEC meeting. In fact, both oil contracts appear to have reached some significant levels, so profit-taking and/or some selling pressure may well be the outcome here.

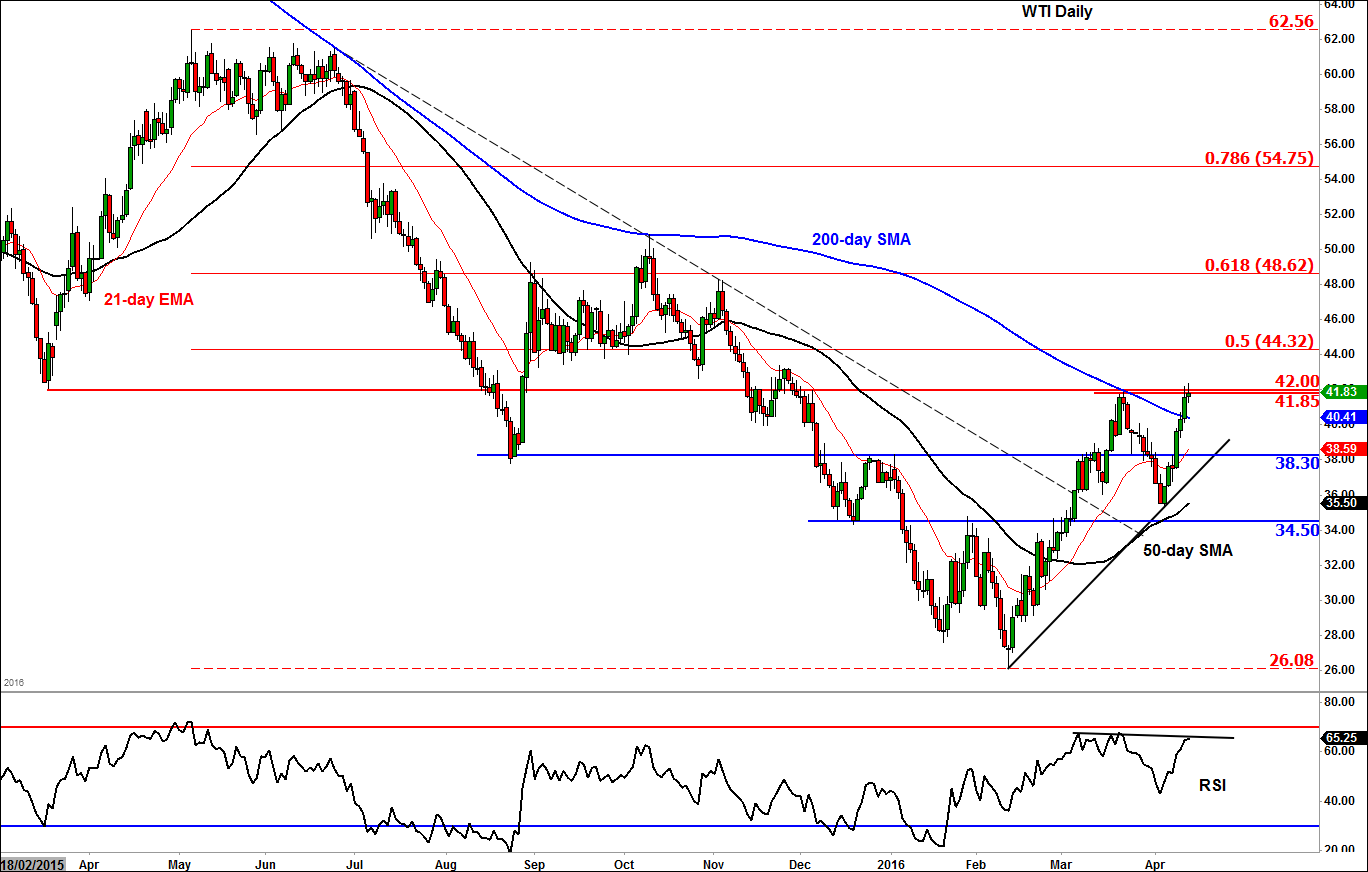

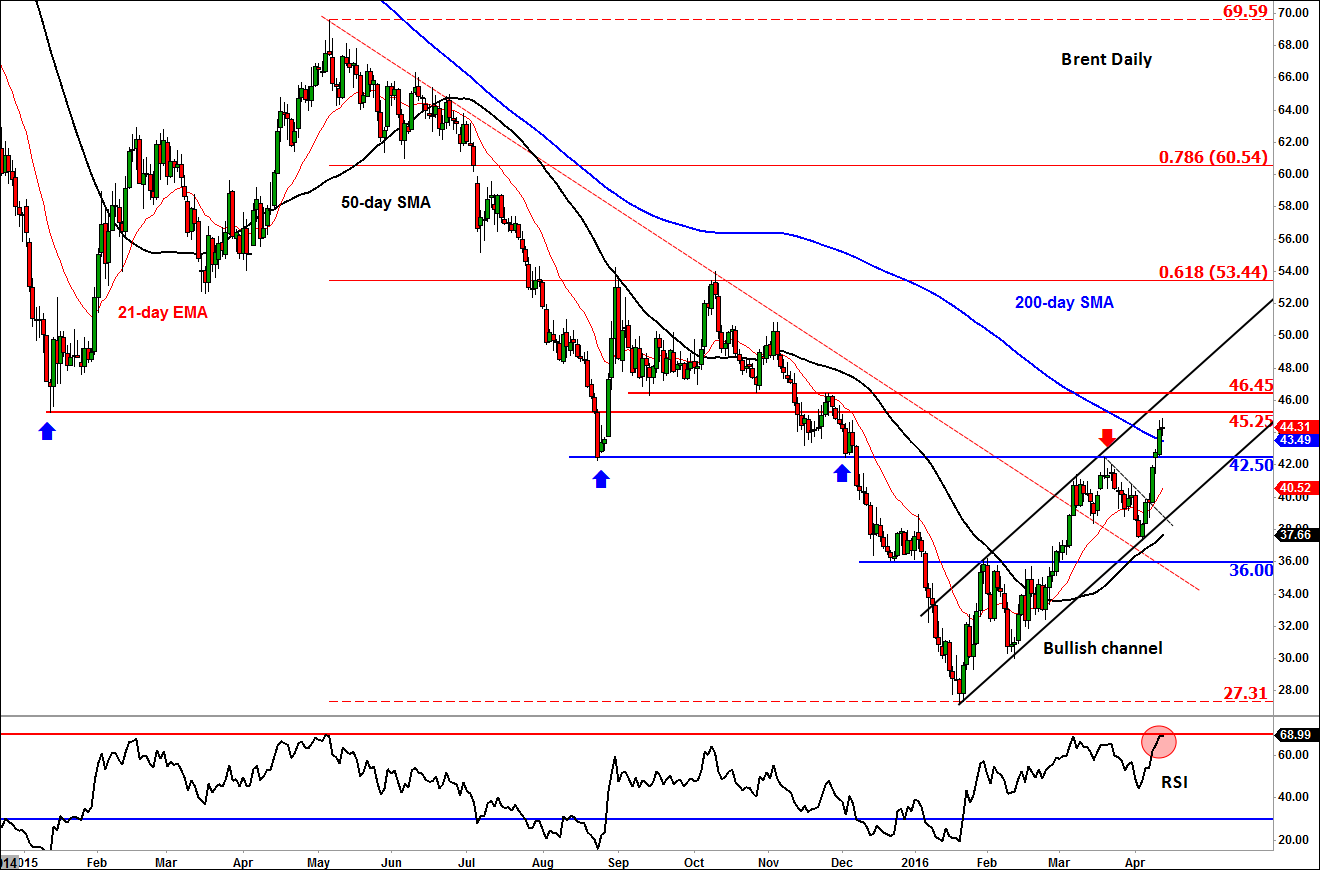

As the WTI’s daily chart shows, below, it has now reached $42.00 which was a pivotal level in the past. The RSI momentum indicator is also in a state of negative divergence with price, making a slightly lower high which suggests that the bullish momentum is weakening. Likewise, the RSI on the Brent contract shows a similar picture, having reached the “overbought” level of 70. The underlying price action on both oil contracts is bullish, however. The short-term moving averages have turned higher in recent times, while both Brent and WTI have now broken above their respective 200-day moving averages and established clear bullish trends. So, the best outcome for the bulls would be if we see a period of consolidation here, which should allow the oscillators to unwind from overbought levels through time rather than price action. Until and unless the trend lines break down, the sellers will need to be nimble, especially given the abovementioned fundamental risk event. The key levels of support and resistance are shown on the chart in blue and red, respectively.