Crude fails to rally despite seventh weekly drawdown

Both the major oil contracts had risen sharply this morning with Brent snapping a 4-day losing streak with a gain of more than 2% and […]

Both the major oil contracts had risen sharply this morning with Brent snapping a 4-day losing streak with a gain of more than 2% and […]

Both the major oil contracts had risen sharply this morning with Brent snapping a 4-day losing streak with a gain of more than 2% and WTI extending its gains for a second day. Traders were buying oil ahead of the official weekly supply numbers after data from industry group the American Petroleum Institute (API) last night had suggested that both crude and gasoline inventories had declined by a more-than-forecast 2.9 million barrels last week. As it turned out, crude inventories did decrease for the seventh time in as many weeks though by just 2.7 million barrels, which disappointed those who were hoping for a reading of 2.9 million or higher. What’s more, crude inventories at Cushing – the delivery point of the Nymex WTI contract – unexpectedly rose by 112,000 barrels last week when a decrease of 850,000 barrels was expected. Speculators were further discouraged when they realised that rather than falling, gasoline stocks had actually increased by 0.5 million barrels. As a result, oil speculators rushed for the exits, causing WTI to turn flat on the day. Brent followed suit and looked poised to surrender all of its earlier gains.

Although US crude stocks have been falling consistently in recent times, with the rig count also declining for several months, the oil price has not really moved much higher over the past seven or so weeks. Investors are probably sceptical that the US supply glut will be reduced in a meaningful way any time soon, even if domestic production slowed last week to 9.59 from 9.61 million barrels the prior week. US shale oil producers can still produce oil profitably at these levels and if prices were to rise a little from here, they could easily ramp up output because the infrastructure is already there. The OPEC meanwhile has been keeping the taps open like there is no tomorrow, with Saudi, Iraq and UAE all pumping record amounts of oil in May. Iran could make a full return to the oil market soon, too, should the US-led sanctions are lifted. As the OPEC tries to win back lost market share, the global oil surplus is thus likely to remain in place for the foreseeable future, even if the demand prospects are looking a little bit brighter. Therefore, oil prices may remain under pressure for a long time.

The investor focus has now turned to the Federal Reserve which concludes a two-day meeting this evening. The FOMC policy statement and economic projections are due at 19:00 BST and the corresponding press conference from Chair Janet Yellen will start half an hour later, at 19:30 BST. Virtually no one expects a rate increase at this meeting, but the Fed may provide hints as to whether it will hike rates in September. Our full FOMC preview, which was written by my colleague Matt Weller, can be found HERE. If a more hawkish than expected message comes out of the Fed then one would expect the dollar to appreciate. Conversely, a more dovish tone could undermine the greenback. Buck-denominated commodities like oil and gold therefore could move sharply in the opposite direction of the dollar – at least in the short term, anyway.

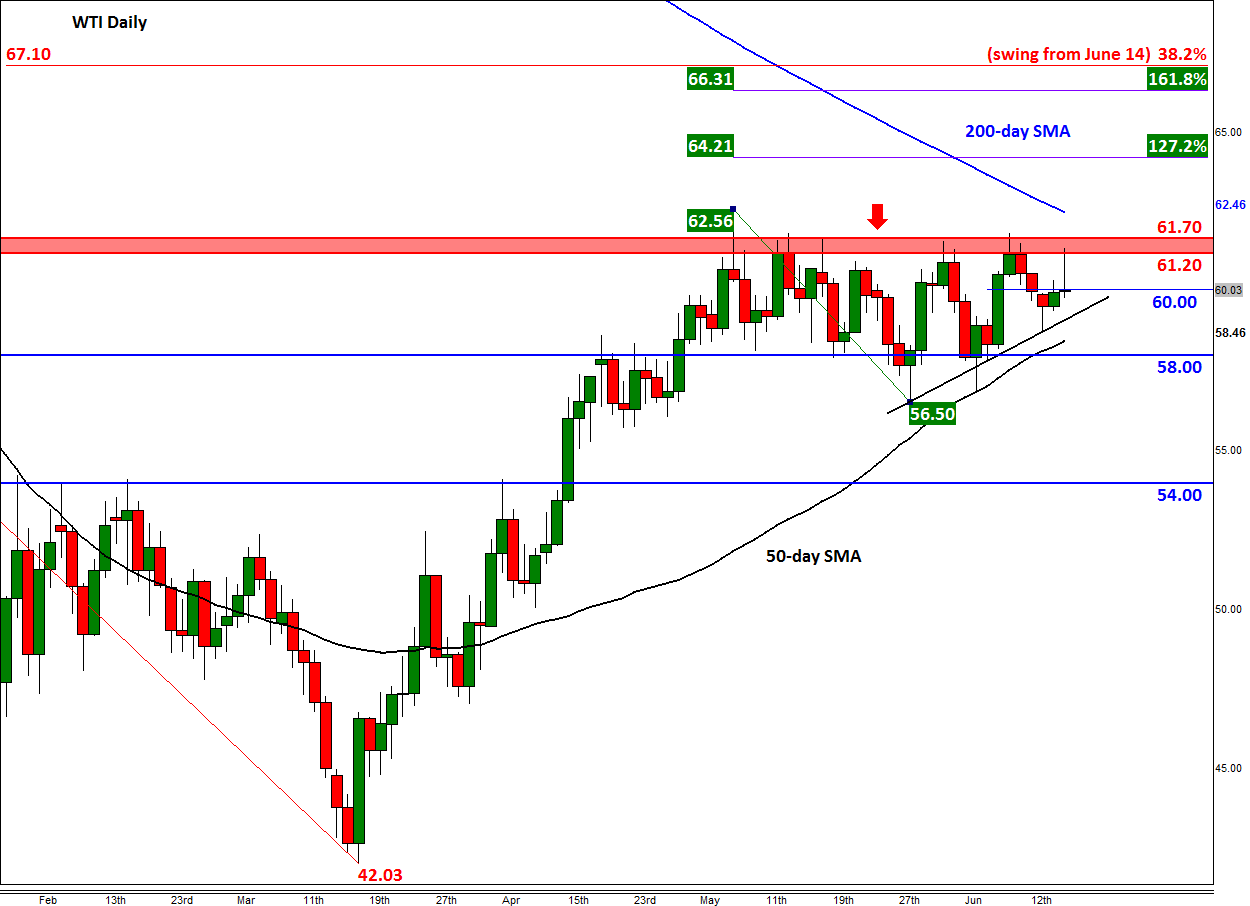

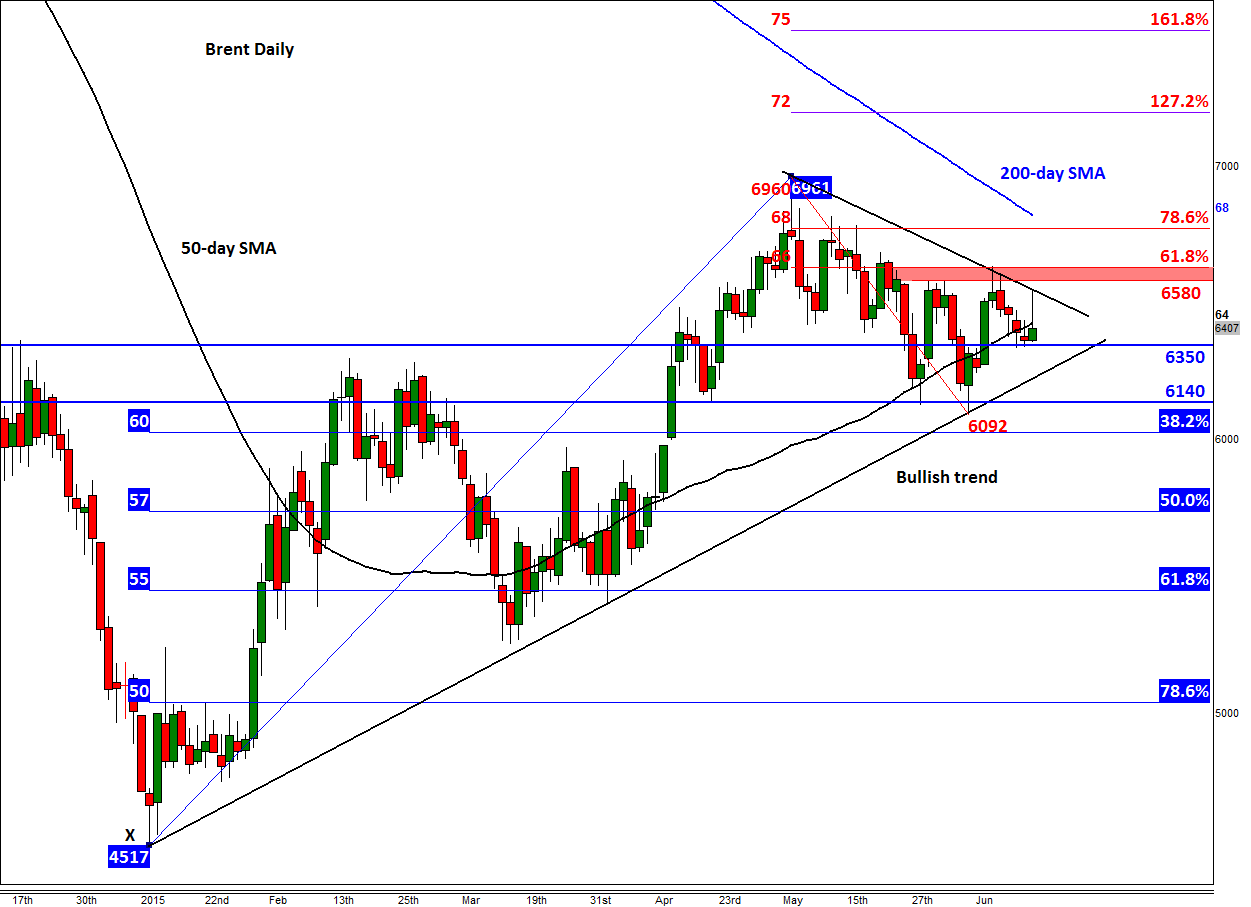

Ahead of the FOMC decision and after the rather bearish oil report, both crude contracts are looking vulnerable. WTI has once again failed to crack that sturdy resistance area between $61.20 and $61.70. The longer the bears hold their nerves here, the more likely it is that the bulls will give up hope and lead to a vicious sell-off. WTI is currently testing the psychological $60 handle and is looking to head further lower. A potential closing break below the 50-day moving average, at $58.45, would be a particularly bearish outcome. If seen, US oil may go on to break the May low of $56.50 and over time potentially even drop to the key $54 handle, a level which was previously resistance. Brent is back below its 50-day average and is heading towards it medium-term bullish trend line. Needless to say, if the trend is taken out in one of the upcoming sessions then a move down to at least the 38.2% Fibonacci level at around $60.30 would be highly likely.