Crude drops as rally runs out of fuel

Oil prices have retreated sharply at the start of this week, with Brent dipping back towards $38 and WTI to $36 a barrel, thus giving […]

Oil prices have retreated sharply at the start of this week, with Brent dipping back towards $38 and WTI to $36 a barrel, thus giving […]

Oil prices have retreated sharply at the start of this week, with Brent dipping back towards $38 and WTI to $36 a barrel, thus giving back a good chunk of their recent gains. Recently, sentiment on the oil market had turned positive on realisation that the significantly lower oil prices had boosted demand, most notably in China, and as large OPEC members decided to talk with Russia about curbing crude output at January levels. Talks have been on-going for several weeks now and so far there has been little or no real progress, with Iran unwilling to participate in a deal unless its daily crude production rises to 4 million barrels. As it is highly uncertain that a deal to freeze oil production is forthcoming without the participation of Iran, and possibly Iraq, bullish oil traders have evidently taken profit on some of their positions. This could well be the case as after all net long holdings in both Brent and WTI had risen strongly in recent times, according to positioning data from both the CFTC and ICE. Further withdrawal of bullish positions, if seen, could pressure oil prices even more.

In the US meanwhile, drilling activity has been falling continually now for some time and recently oil supply has also started to decline. As such, the high inventory levels should begin to fall soon. So far however there’s been little evidence of that. If anything, crude stockpiles have actually risen to fresh record levels. And there is a danger they may climb even more because of the seasonal maintenance works at this time of the year. So traders should watch the latest stockpiles data from the American Petroleum Institute (tonight) and the Energy Information Administration (tomorrow) closely and if they show any surprise drawdowns then this could be positive news for oil prices. But I think that by the start of the summer driving season, we should begin to see sharp declines in oil inventories anyway as demand for gasoline, which is already strong for this time of the year, rises further.

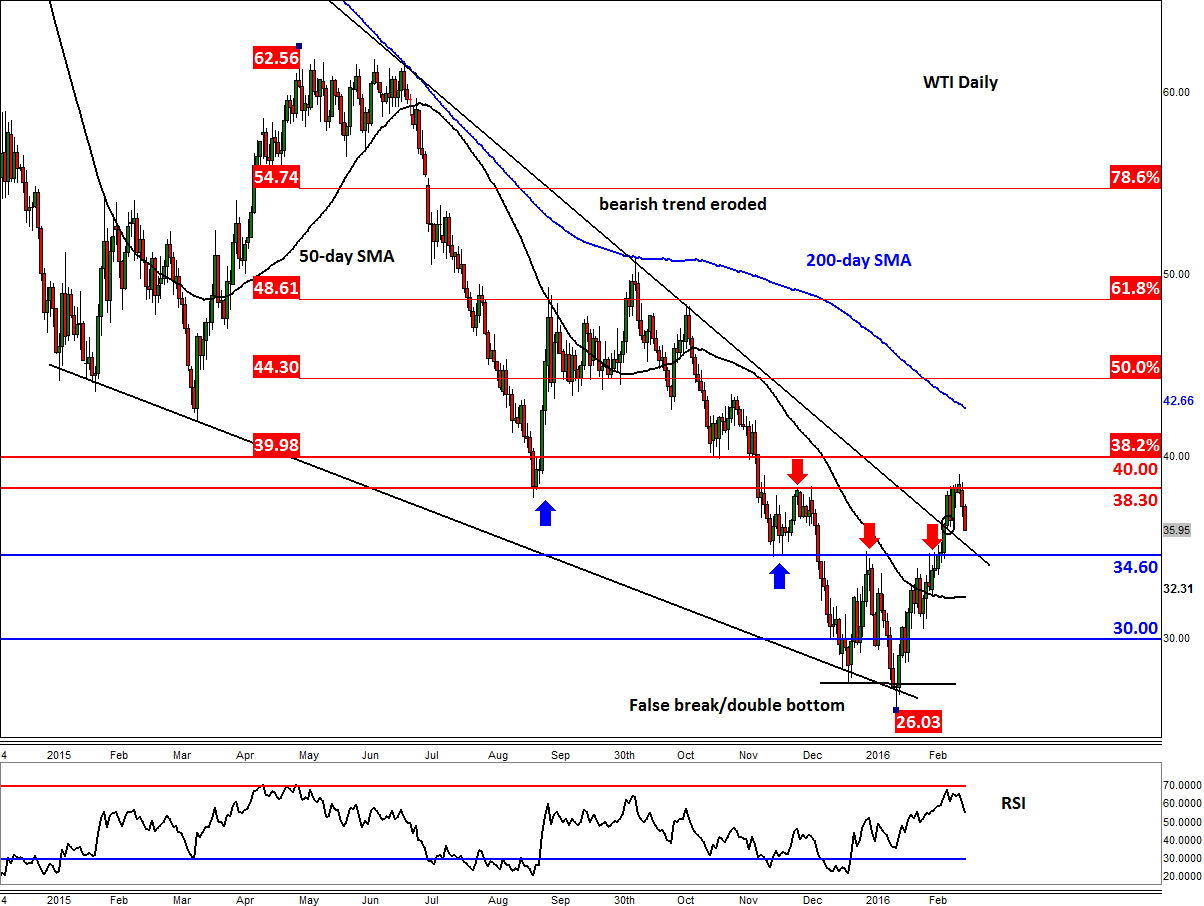

The technical outlook on WTI oil remains bullish despite the latest sell-off. The US oil contract formed a double bottom reversal pattern around the $26/$27 area in February, before breaking out of its falling wedge (bullish) pattern to the upside earlier this month. It has also taken out several resistance levels, including $34.60 most recently. However, the rally has come to a halt around the old resistance area of $38.30. For now, it looks like the bears are aiming for the broken resistance at $34.60 as their next big target. Our short-term outlook would turn bearish only if WTI breaks back below this support level on a daily closing basis. In this potential scenario, oil could then drop to test its 50-day moving average at $32.30 or even the psychological $30 handle once more.

But until and unless $34.60 breaks, we would expect oil to recover and head higher once again. If and when it breaks above the $38.30 resistance then the bulls may aim for the psychological level of $40 as their next target. This level was also previously support and converges with the 38.2% Fibonacci retracement against the May 2015 high. An eventual breakout above $40, if seen, would be deemed a very bullish outcome.