Crude arrives at key technical juncture ahead of stocks data

Crude oil has now fallen for the third consecutive trading day. Despite the significantly weaker prices, sentiment remains decisively bearish, in part because of the […]

Crude oil has now fallen for the third consecutive trading day. Despite the significantly weaker prices, sentiment remains decisively bearish, in part because of the […]

Crude oil has now fallen for the third consecutive trading day. Despite the significantly weaker prices, sentiment remains decisively bearish, in part because of the lack any significantly bullish fundamental factors. So, the situation is still the same, which is that the oil market remains significantly oversupplied. Over the past couple of weeks, US crude stocks have risen noticeably sharply, which admittedly has been due to seasonal factors as many refineries are shut because of maintenance works. Another sharp build in inventories is what many people fear we will see from the API and EIA’s weekly reports, which will be published tonight and tomorrow, respectively. Traders are also concerned that the global excess will still be in place for much of 2016 as potential increases of Iranian supplies and elsewhere will simply offset the expected falls in US oil output. The fact that economic growth in China and elsewhere has slowed down recently means that the growth in oil demand will also likely to be weaker which therefore means that the rebalancing of the market will take longer to achieve than expected. Indeed, demand concerns could come to the forefront of investors’ minds if the third quarter US GDP estimate disappoints expectations on Thursday.

But I wonder how much of all this negativity is already priced in and as such I don’t envisage there to be further vicious drops in oil prices. So we may see some consolidation around the current levels until we see more evidence that US oil production is indeed going to be reduced in a meaningful way. Even so, the potential gains could be limited.

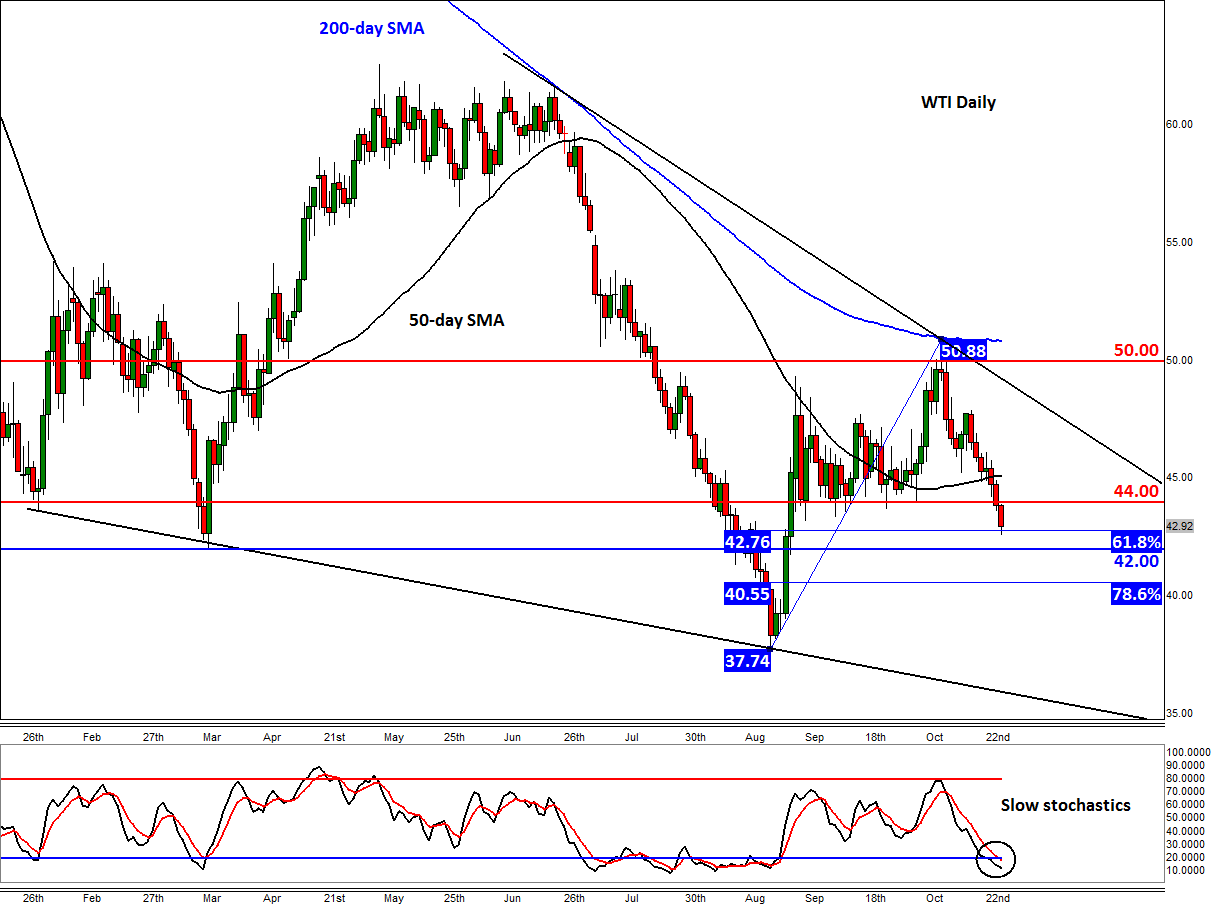

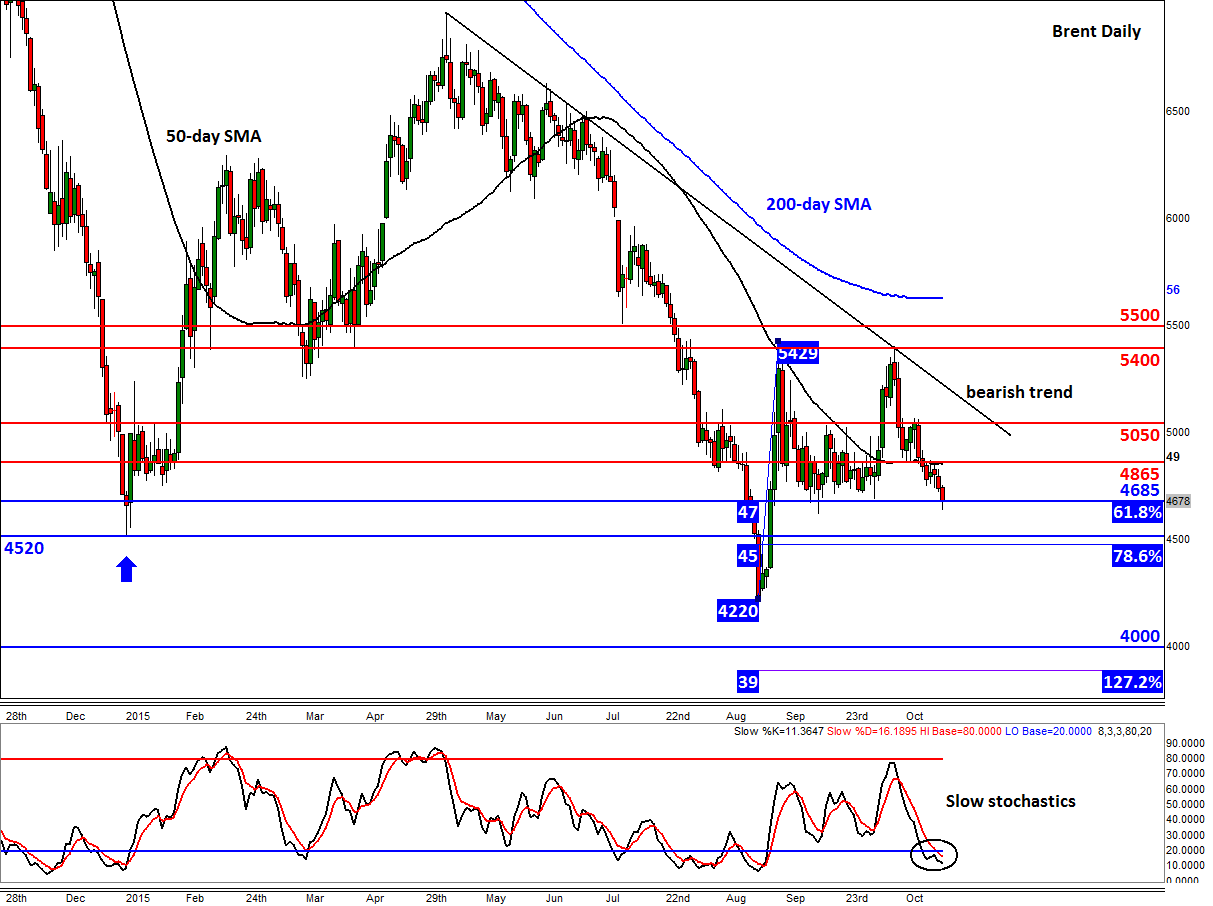

Technical outlook

Both crude contracts have now reached some technically-important levels after a 2.5-week sell-off, namely the 61.8% Fibonacci retracements of the upswing from the August low. For Brent, this comes in around $46.85 while for WTI it is at $42.75. The 61.8% is among the most important of Fibonacci retracement levels. It is often used to provide an objective profit target, while under certain circumstances it could also be used as an ideal entry point in the opposite direction. In the case of oil, both Brent and WTI prices have been falling every day apart from three or four occasions since the last rally ran out of steam around the 9-10th October. Since then, Brent has fallen some 13 per cent while WTI has shed around 15%. Following such a vicious sell-off, it is likely that some of the existing sellers would be looking to book profit here. Bullish speculators meanwhile might be thinking that prices are oversold – as suggested, for example, by the slow stochastic momentum indicators – and may therefore step in here. There may also be a group of speculators who think oil prices have already bottomed out this year and this recent pullback is a perfect opportunity to go long after missing the initial rally at the end of August. Now, whether or not we have already seen a bottom is up for debate and unconfirmed at this stage, but for all the above reasons the probability of that we may see at least a short-term bounce here is now high.

However, should oil prices break decisively below the above-mentioned support levels, then further losses could follow in the coming days, although WTI’s next potential support, at $42.00, is not that far off now. Below $42 is the 78.6% retracement at $40.55 followed by the August low at $37.75. For Brent, the next support is around $45.00/20, followed by the August low at $42.20.

But for the short-term bias to turn bullish, both oil contracts will now need to break down some key resistance levels, starting with $44.00 on WTI and $48.65 for Brent. Until and unless we see that, any potential bounces here should be taken with a pinch of salt.