Crude all eyes on Iran

Yet again, crude failed to move higher in response to news of a sharper-than-expected draw of 4.9 million barrels in US oil stocks in midweek. […]

Yet again, crude failed to move higher in response to news of a sharper-than-expected draw of 4.9 million barrels in US oil stocks in midweek. […]

Yet again, crude failed to move higher in response to news of a sharper-than-expected draw of 4.9 million barrels in US oil stocks in midweek. It appears as though investors are growing worried about the possibility of Iran flooding the already-saturated global oil market soon. After all, the P5+1 group of Western powers’ self-imposed June 30 deadline for negotiating a final nuclear agreement with Iran is just days away now and the signs are that, unlike the Greek situation, the talks are going well – though by no means the outcome is certain. If sanctions over Iranian oil are lifted, this could have a major impact on oil prices. At the moment though, the market seem relaxed, probably for two reasons. First, the market does not think that the oil sanctions will be lifted completely. Second, that even if the sanctions are lifted completely, it would take the Iranian oil industry a long time to recover. However these assumptions are dangerous in our view. For a start, the infrastructure is already there which means production could increase more quickly than some might think. What’s more, even if it takes a long time for Iranian oil output to return near the pre-sanctions levels, it is the market’s expectations about this additional supply that could weigh on oil prices.

Iran’s oil minister recently said that Tehran’s crude output could increase by almost 1 million barrels per day within 6 months after the time the sanctions are lifted. With the OPEC already producing about 1 million barrels more than its agreed quota of 30 million barrels per day, it wouldn’t take a rocket scientist to come to the conclusion that the supply glut would exacerbate in the event of Iran making a full return to the market. Worried about its lost market share to US shale producers, it is unlikely that the Saudis will make room for this additional output. Libya, which has suffered supply outages of its own in recent times, is also unlikely to make changes to its output and for that matter neither might Iraq. Other OPEC members are only likely to trim their productions levels if the Saudis, Iraqis and co do the same which, as mentioned, appear unlikely. Against these backdrops, any potential falls in non-OPEC supply output may easily be absorbed. This, in our view, is exactly while oil prices have failed to move higher despite signs of falling US oil production and destocking of crude from the admittedly record levels.

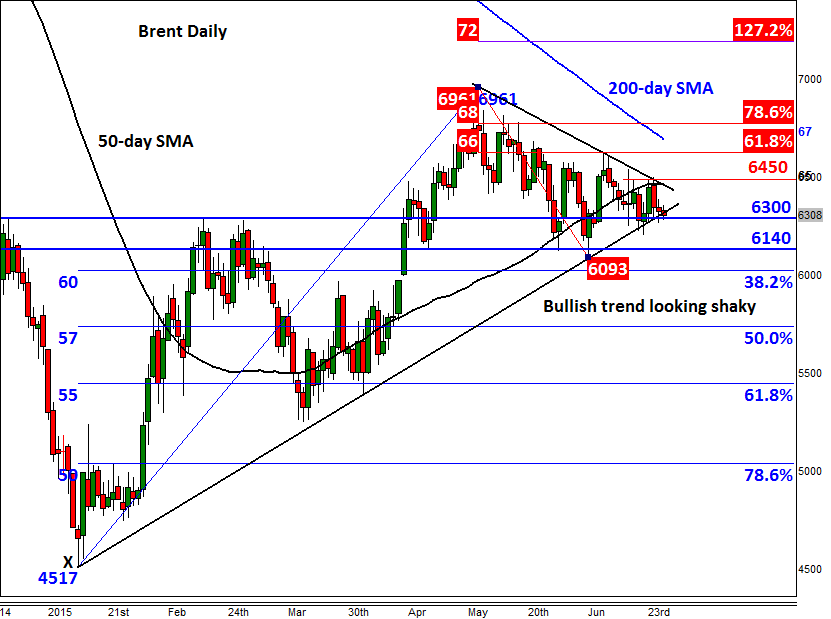

Ahead of the June 30 deadline, Brent is consolidating in between the converging trend lines which you can see on the daily chart. The support trend is looking shaky and given the abovementioned fundamental backdrops we wouldn’t be surprised if it broke it down even before we hear anything on Iran. If broken, Brent could easily drop to the next level of support at $61.40 or revisit this month’s low of just below $61.00, before making its next move. The Fibonacci levels are among the longer term targets for the bears, though Brent could get to those levels fairly quickly if Iran was allowed to make a full return to the market. Meanwhile a potential break above the bearish trend and resistance at $64.50 could pave the way for a move towards the 61.8% Fibonacci retracement level from the May high, around $66.25. Thereafter is the 200-day moving average at $67.15 and then the May high itself at $69.60.