US President Donald Trump has arrived in Japan on the eve of the G20 summit, where he will hold talks with Chinese leader Xi Jinping. The outcome of the meetings will likely be a binary one. If trade talks falter, Trump has said he has a plan B for China: more tariffs on Chinese goods. If they make progress, then a delay in raising tariffs or cancelling some of the previously announced-levies are likely, and talks could resume between the two nations in July. Another topic that will likely take centre stage will be that of Iran’s situation, so oil prices could be impacted as well as equity and FX markets. Ahead of the meetings, sentiment is cautious and investors are taking no chances. But there is one major market that may be able to ignore what happens at the G20, or not react too negatively in the event of talks collapsing: silver.

Silver may be able to ignore G20 developments

It is inevitable that most markets will be impacted by the outcome of the talks at G20, making it even more difficult to predict the direction of prices. But one market that is least likely to be impacted will probably be silver as it is considered both a precious metal (and therefore a safe haven asset), and an industrial material (simultaneously making it a risk asset). But with the dollar falling recently and yields ticking lower, the grey metal has been making steady but slow progress, unlike gold and Bitcoin. But is it about to do what gold and Bitcoin have recently, and stage a sharp rally?

Gold/silver ratio climbs towards records

At around $92, the gold/silver ratio has climbed to levels not seen since the early 90s. This means that the probability of a collapse in the ratio is on the rise. If the ratio drops, this could obviously happen in two ways: both metals falling with gold dipping at a faster clip, or both rising with silver at a faster pace. Either way, silver could outperform gold. Given that the ratio has been as low as $32 in 2011 and around $15 in late 70s, there is significant room for upside potential in silver (or downside for gold, obviously).

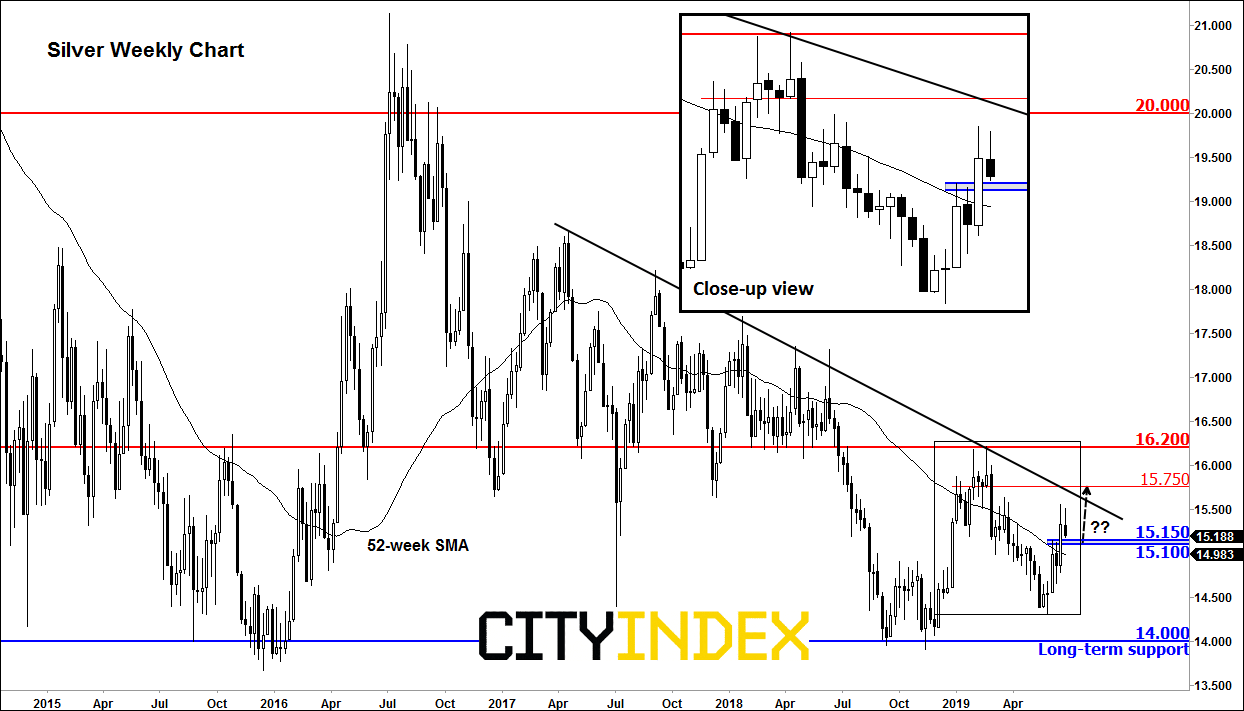

Silver tests key support

As the theme of the above fundamental considerations is long-term, we might as well keep the technical focus on a higher time frame. So, looking at the weekly chart of the metal, things are starting to look quite interesting for bulls although unlike gold, silver is still holding below its long term resistances, which explains why the gold/silver ratio has been climbing towards record levels. Crucially, however, we have seen the development of some bullish price action over the last several months above the long-term support in the $14.00 region. This could be the start of something big, although we are yet to see the break of the medium-term bearish trend line. But with price making a couple of shorter-term higher highs and higher lows, a breakout could be on the cards over the coming weeks. It is therefore imperative that the bulls will be able to hold their own and defend the old resistance at around the $15.10/15 region, which was being tested at the time of writing.

Source: eSignal and City Index

Latest market news

Yesterday 08:33 AM

Latest Gold articles

April 1, 2024 01:09 PM

March 28, 2024 10:30 AM

March 26, 2024 11:24 PM

March 26, 2024 12:00 PM