China keeps ‘adult-in-the-room’ stance, setting limits on coming mayhem

Stock indices and futures are on a decisive rebound from some of the fiercest selling for years. (See an update about the stock market’s bounce here, by my colleague senior technical analyst Fawad Razaqzada.) The trigger: The People’s Bank of China applied a lower than expected gap between onshore and offshore yuan rates at its daily fix. Since this happened just a day the PBOC deliberately allowed the renminbi to weaken below the highly symbolic rate of seven yuan per U.S. dollar, investors interpret the moves as still constructive for market stability, even if the central bank had sought to project a clear message with the renminbi’s first breach of the guided level in five years. As such, Beijing demonstrates that it wants to keep its ‘adult-in-the-room’ stance. Regardless of how authentic that posture may be, it implies limits to the pace or even degree of escalation that’s likely still to come.

The probable shape of further escalation is an important watch point. In Europe, a salient concern is that trade sanctions, including tariffs and corporate level restrictions like the U.S. Commerce Department’s Entity List, could become the template for action against European industries. After Washington levied 10%-25% tariffs on European steel and aluminium imports, U.S. President Donald Trump has been vocal about EU trade barriers, noting last week that "auto tariffs are never off the table".

So whilst the U.S. Treasury has duly labelled China a “currency manipulator”, a move that carries grave consequences and ramifications, it is important to note that the Treasury also signalled that the categorisation has not automatically triggered technical discussions that may ultimately lead to an IMF request for evaluation. To be sure, the designation does increase Washington’s leeway to escalate, but does not guarantee further action. That is appropriate given China’s ambivalent status as a ‘manipulator’. Relative yuan stability over the past decade has followed the PBOC’s active policy to prevent its currency from accelerating lower.

Whilst acknowledging that U.S.-China trade relations remain markets’ clearest and most present danger at present, we think the details mitigate the risk of a violent and rapid escalation that represents the worst-case scenario for risk appetite.

The current bounce by stock markets demonstrates that investors continue to ‘risk’ that scenario as low-probability. Furthermore, despite a definitive flight from risk in recent sessions, ‘panic’ was not necessarily evident. Why would it be? Long-standing pressures and concerns—inversions, negative yields, slowing growth, all aggravated by the trade conflict—warned that a significant portion of the stellar stock market advance from December's low would eventually be torched. We just didn’t know when. Furthermore, portions of above-norm valuations were also suggestive of a correction this year.

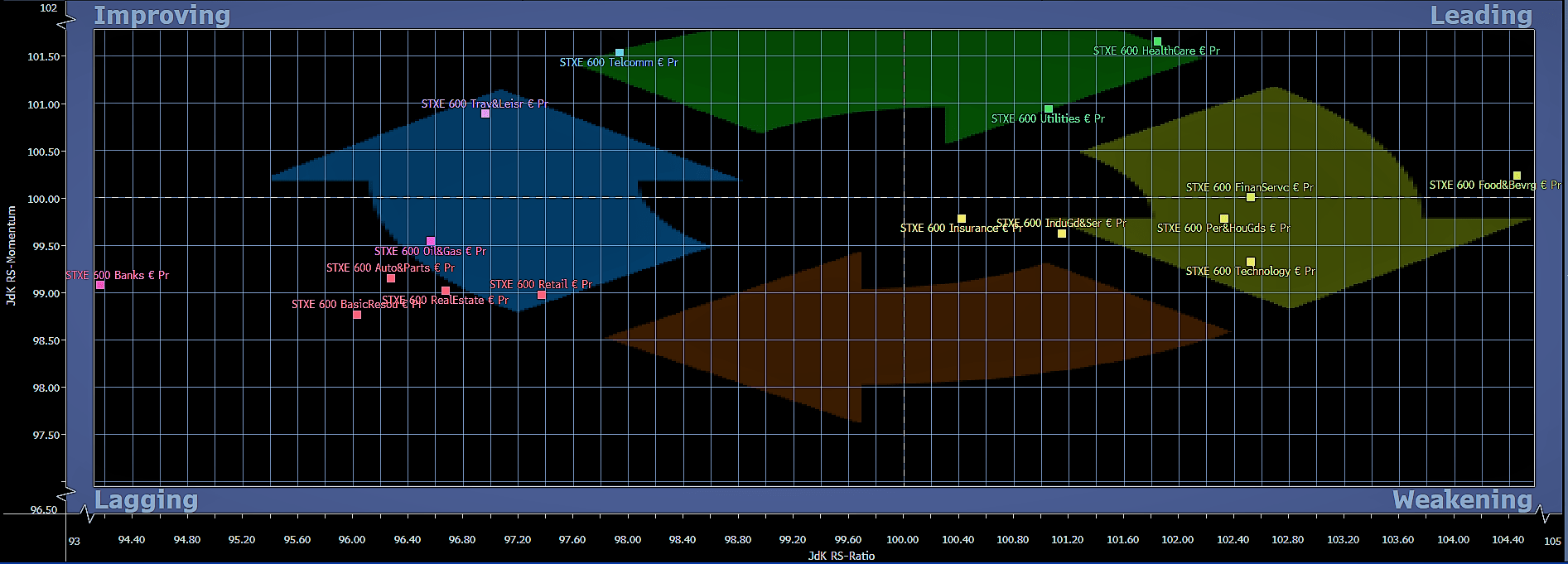

Our Relative Rotation Graph of STOXX Europe 600 industrial indices shows high-beta and cyclical sectors entering the ‘weakening’ quadrant, whilst a pre-eminent ‘defensive’ sector, healthcare, shows the most positive momentum, as defined by the model, in the ‘leading’ quadrant. The chart interval is ‘weekly’ suggesting that even with one of the best first-half advances in years, investors were well aware the party would be over sooner rather than later.

Relative Rotation Graph – STOXX 600 sector indices – weekly

Source: Bloomberg/City Index

Key takeaways

- Whilst the sudden re-escalation of the trade conflict presents severe impediments to risk appetite and the global economy, the outbreak may not be as much of a surprise as the reaction suggests

- China has demonstrated that it is prepared to favour an even-handed approach, to ‘shock and awe’, this puts brakes on potential further escalation

- The backstop of Federal Reserve policy loosening, clearly flagged by chair Jerome Powell last week, in combination with a continued orderly correction, if any, can limit stock market declines to the same magnitude of those seen between October and December last year.

Latest market news

Today 07:55 AM

Today 04:47 AM

Yesterday 11:23 PM

Yesterday 10:19 PM

Yesterday 08:00 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM