March 31, 2021 10:47 AM

China: So many problems but PMIs ain’t one

Geopolitical tensions with China have been abundant over the last few weeks. The European Union, UK, US, and Canada have all placed sanctions on China regarding human rights violations. In response, China has placed sanctions on senior individuals in various capacities in each of those countries. In addition, China and Iran signed a deal work $400 Billion investment deal last weekend, which means more sanctions may be ahead. Of course, China is still dealing with the sanctions from President Trump on technology firms such as Huawei, who was accused of spying (although they did show a profit last year in earnings released earlier today). And a new potential problem has come to light over the past few days regarding China’s cooperation with the WHO during their investigation into the origins of the coronavirus. There is increasing speculation that China was not transparent with WHO investigators when they recently visited.

However, despite all the geopolitical negativity surrounding China lately, they are still producing! China’s official Manufacturing PMI rose to 51.9 in March vs a reading of 50.6 in February. Expectations were for a reading of 51.0. This was China’s highest reading since December. The Services PMI beat was even more impressive. The March Services PMI was 56.3 vs 51.4 in February. This was the highest reading in 4 months. All components of both indexes rose! Many have been expecting the recent slowdown in the PMI data to continue. However, the stronger data shows that China is still a force and worries of a contraction may have been premature.

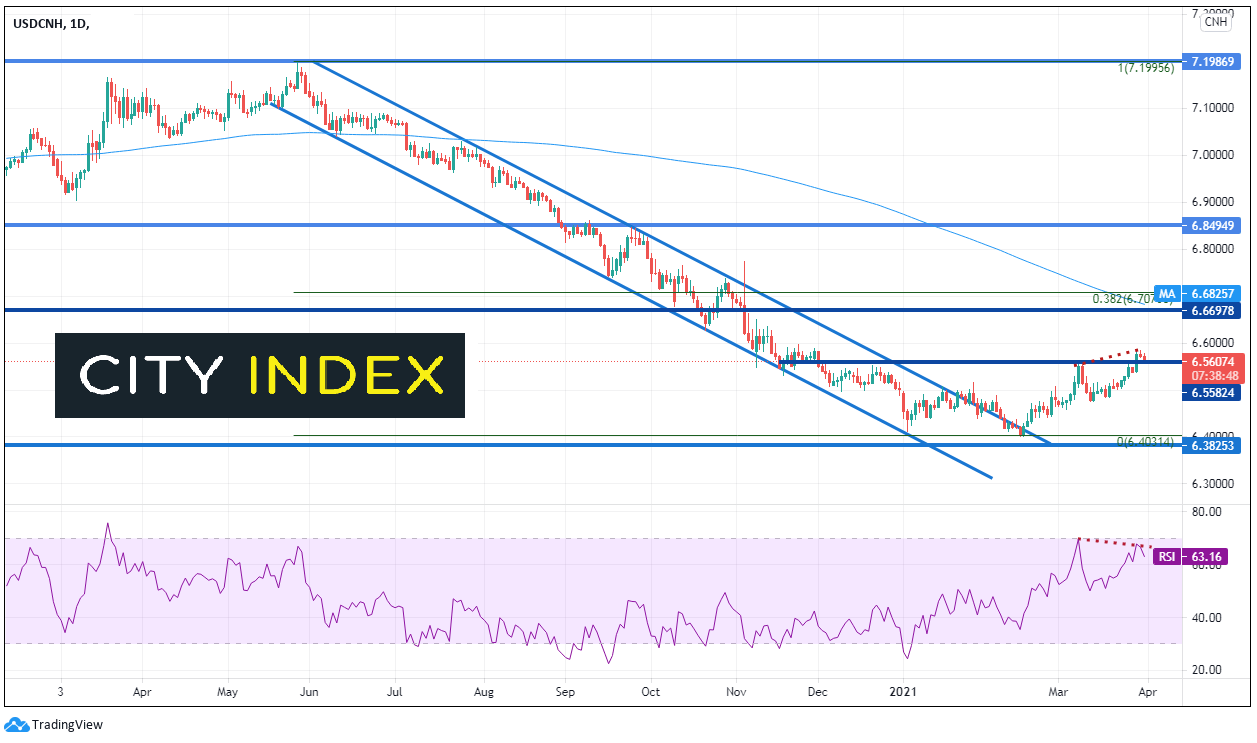

USD/CNH had been moving lower in an orderly channel since late May 2020. The pair put in a low on January 5th near 6.4116 and began trading sideways, moving out of the downward sloping channel. After briefly pushing below the January 5th low in mid-February, the pair began moving higher and broke above horizontal resistance on Monday near 6.5626. However, note that price is diverging from the RSI, which may be an indication of a pullback.

Source: Tradingview, City Index

There is a confluence of resistance above on the daily, but not until 6.6670. With the horizontal resistance at that level dating back to April 2019, the 200 Day Moving Average at 6.6825, and the 38.2% Fibonacci retracement level from the highs of May 27th, 2020 to the lows on February 25th near 6.7074, there is strong potential for a halt in price if it reaches these level.

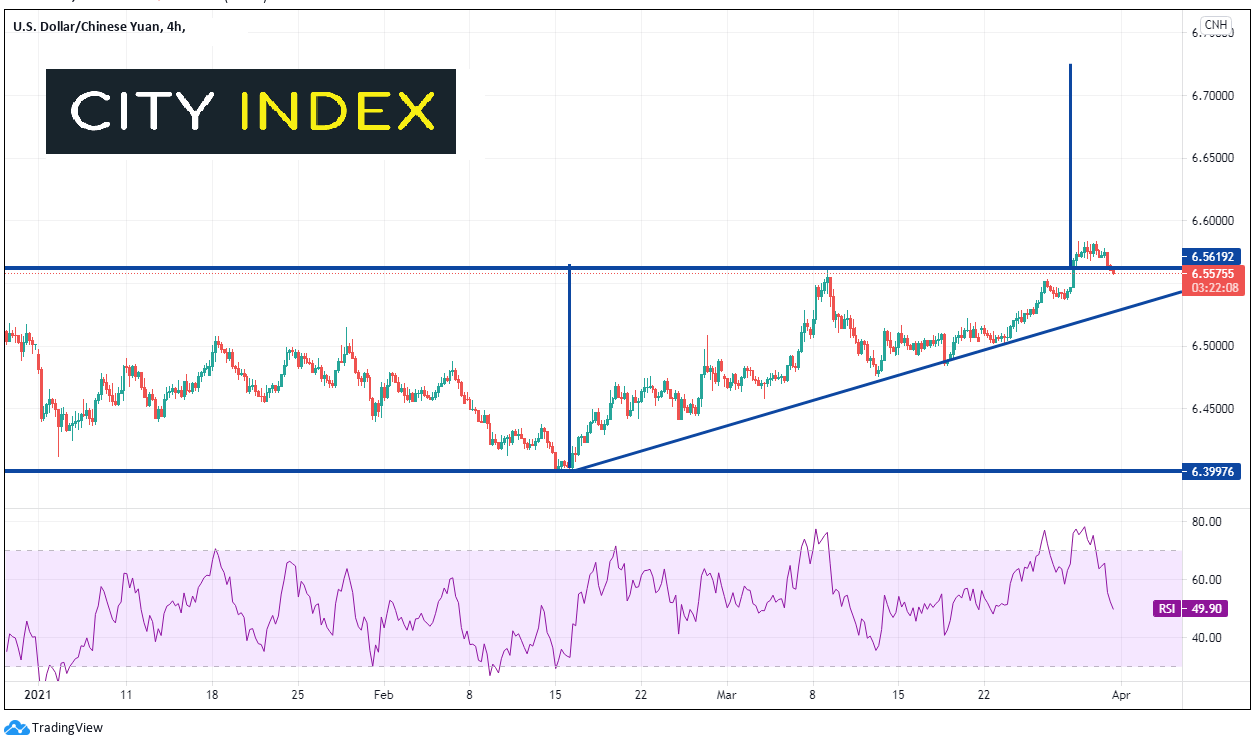

Source: Tradingview, City Index

On a 240-minute timeframe, the sideways channel since the beginning of the year is clearer. Off the lows of February 15th, price began forming a rising triangle and the break above the horizontal resistance on the daily was also a breakout of the rising triangle. The target for a rising triangle is the height of the triangle added to the breakout point, which s near 6.7250. This is just above the resistance levels on the daily chart; therefore, it may have some difficulty making it that far. Price is currently retesting the breakout point near 6.5625. Bulls will be looking to add near current levels Support is below the rising trendline of the triangle near 6.5285.

Despite all the geopolitical problems, the economy is still humming along. USD/CNH has been drifting higher for the past month. The rising US Dollar may be to blame for the rise in USD/CNH, however the technical indication is that if the breakout holds, the pair could move much higher!

Learn more about forex trading opportunities

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Forex articles

April 24, 2024 03:14 PM

April 24, 2024 11:00 AM

April 23, 2024 11:09 PM