China s currency devaluation raises question marks over crude demand

The biggest market-moving events so far this week have come from China. First, it was the disappointing trade figures that were released over the weekend […]

The biggest market-moving events so far this week have come from China. First, it was the disappointing trade figures that were released over the weekend […]

The biggest market-moving events so far this week have come from China. First, it was the disappointing trade figures that were released over the weekend which showed exports had tumbled some 8.3% in July from a year earlier. Chinese imports weren’t great either, though inward shipments of crude oil in July climbed to a record high on a monthly basis which helped to underpin Brent and WTI prices on Monday. Nevertheless, concerns about the Chinese economy remains in focus which is continuing to weigh heavily on commodities across the board. This view has been reinforced by China’s surprise move overnight to weaken the yuan’s daily reference rate by a record 1.9%. The PBOC said this was a one-off adjustment as the yuan’s effective rate was stronger than that of the other currencies. But the devaluation has triggered a “risk off” response from traders, with stocks and commodities falling sharply along with the yuan and Australian dollar, assets that are sensitive to changes or perceived changes in Chinese demand. Clearly, the market has interpreted the move as a sign that the health of the Chinese economy is probably worse than even what the official data suggests. Wednesday’s industrial data from the world’s second largest economy is therefore likely to garner more attention than usual. Meanwhile on the supply front, not much has changed. If anything, the excess surplus has increased. Indeed, the OPEC raised its output by 100,700 barrels a day (mb/d) to 31.5 million last month, the most in more than three years and significantly higher than the required 29.2 mb/d for 2015. According the OPEC, output increased from Iraq, Angola, Saudi Arabia and Iran, while production in Libya fell.

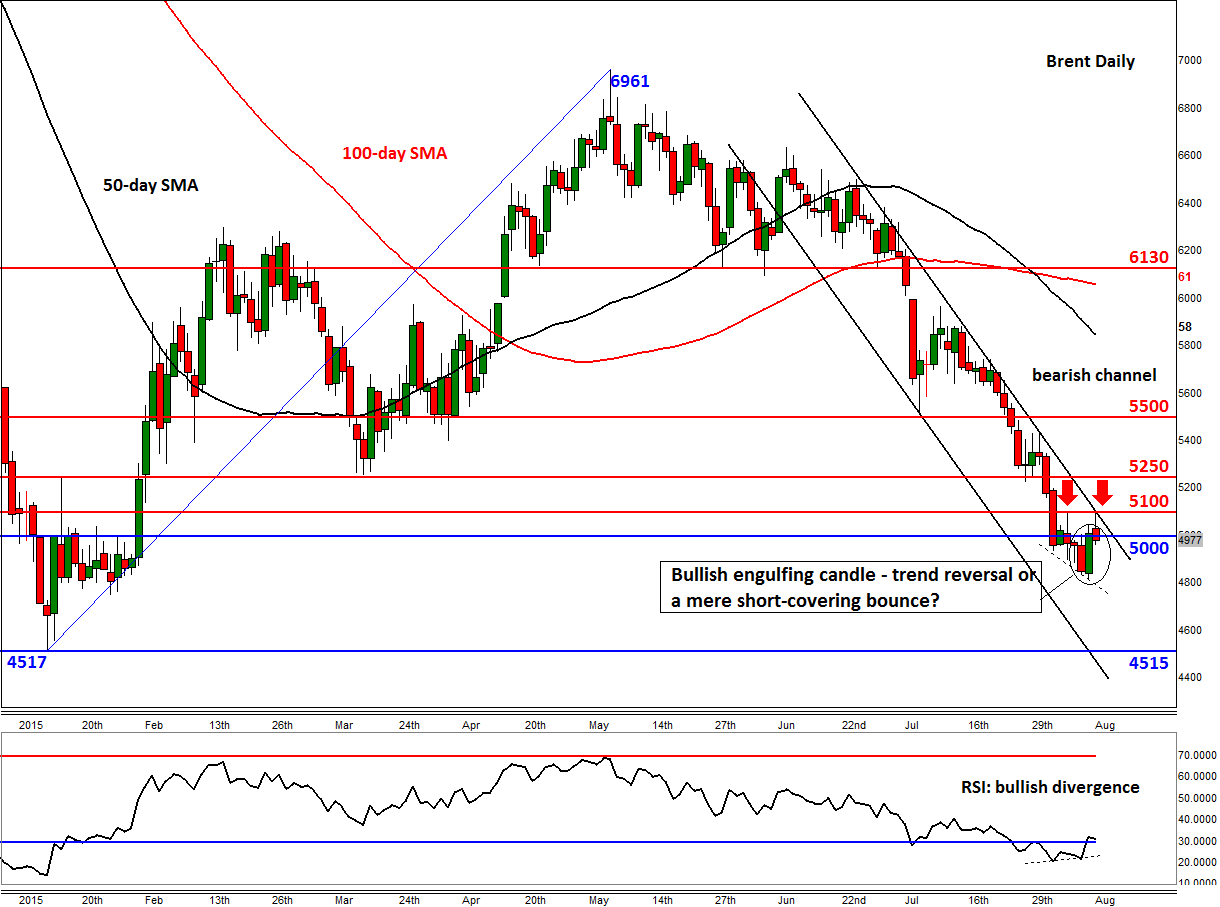

Crude oil’s rally on Monday looks increasingly like a mere short-covering bounce rather than a trend reversal, though things could change yet again as we are only in the first half of today’s session. The London-based oil contract has so far this session dropped by a good $1.30 after earlier rallying to test $51.00. This followed yesterday’s sharp rally which resulted in the creation of a bullish engulfing candle on the daily chart, a pattern which sometimes suggests a change in the trend. The $51.00 level marks a key technical area as not only was it previously resistance but it also ties in with the upper trend of the bearish channel. Only a closing break above $51.00 would invalidate the near term bearish trend. If seen, Brent could easily recover to $52.50 or even $55.00 before deciding on its next move. On the downside, a break below Monday’s low of $48.20 could pave the way for move towards the lower trend of the bearish channel and this year’s low at $45.15.

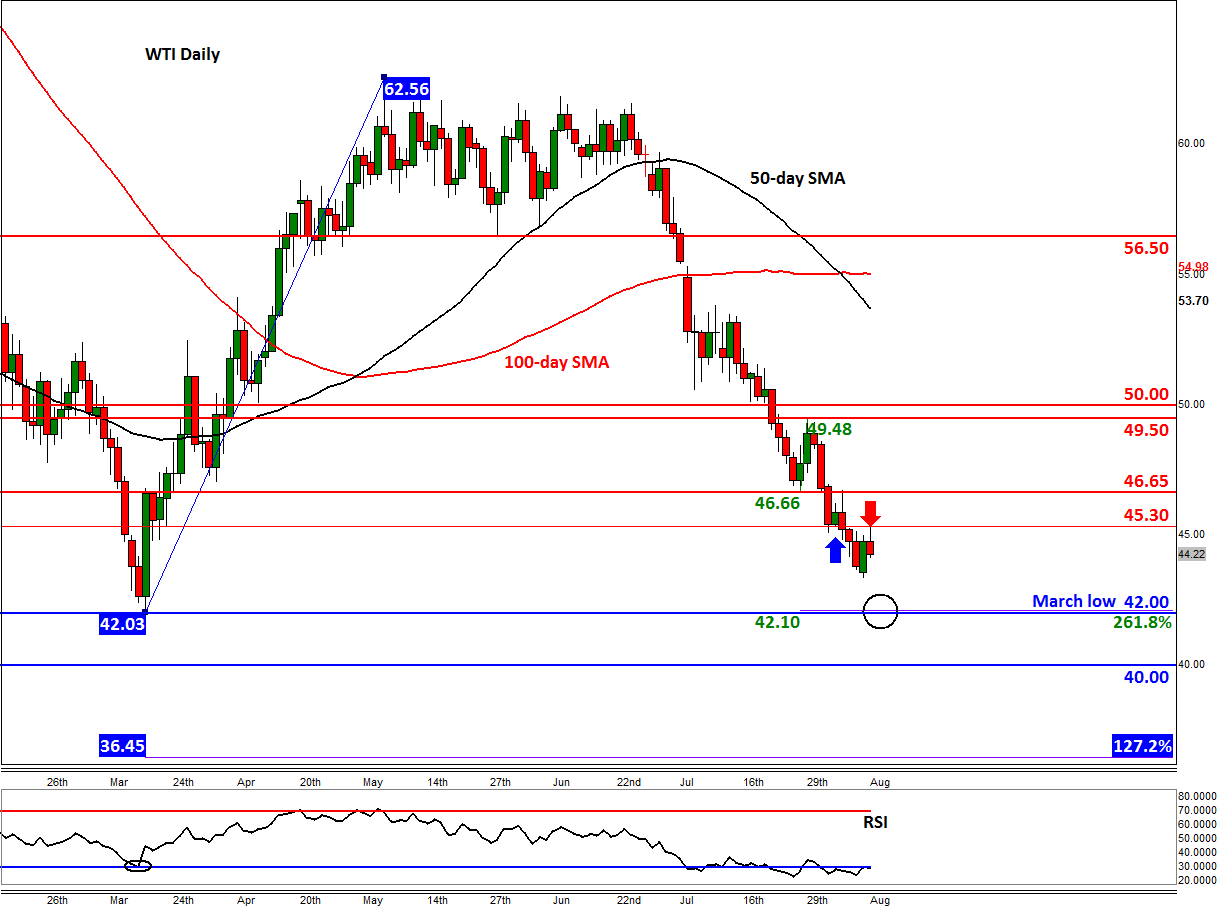

WTI is likewise shedding some of the gains it made during yesterday’s session ahead of the latest weekly crude oil inventories reports from the American Petroleum Institute (API) tonight and the Energy Information Administration (EIA) tomorrow. So far, the bears are managing to defend the key resistance level at $45.30. The short-term bias would turn bullish if this level breaks, which could then see US oil rally towards the next resistances such as $46.65, $49.50 or even $50.00. But like Brent, the path of least resistance remains to the south and this year’s low at $42.00 is clearly now in sight.