China s bears feast on bloated equity markets

It’s been a very eventful few months for Chinese equities as the battle between bulls and bears intensifies. For most of the year Chinese stock […]

It’s been a very eventful few months for Chinese equities as the battle between bulls and bears intensifies. For most of the year Chinese stock […]

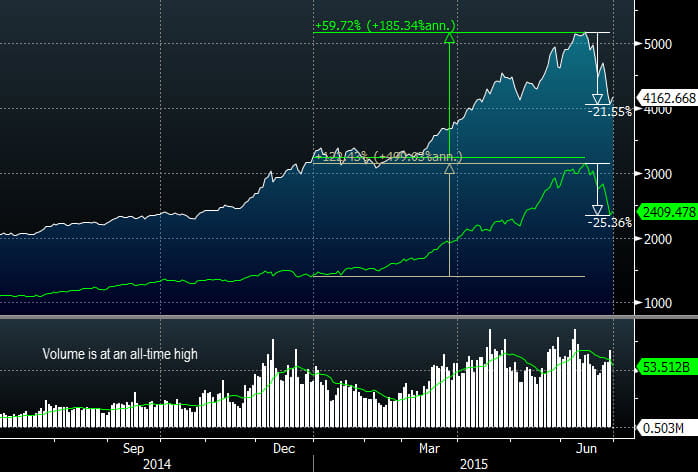

It’s been a very eventful few months for Chinese equities as the battle between bulls and bears intensifies. For most of the year Chinese stock markets have been surging higher due to a reallocation of assets away from cash and property on the back of policy easing from both monetary and fiscal authorities. At one point in mid-June the Shanghai Composite was up around 60% YTD and the tech-heavy Shenzhen Composite was up an even more staggering 120% over the same period.

Since then both markets have pulled back dramatically, with the Shanghai and Shenzhen indices down around 22% and 26%, respectively, from their peaks, leading some commentators to suggest that the bull market is over. Yet, even with their recent losses the aforementioned markets are still around 25% and 65% in the black (see figure 1), respectively, YTD at the time of writing. In fact, the Shanghai Composite is still the fourth best performing primary equity index this year according to Bloomberg.

Figure1: Shanghai Composite (white) and Shenzhen Composite

Source: Bloomberg

The People’s Bank of China (PBoC) has been actively attempting to boost economic growth through numerous cuts to interest rates and a reduction in the amount of cash that banks are required to hold in reserve. Looser policy is making cash less attractive and debt cheaper, pushing investors into equities. At onetime this may have fuelled a push towards China’s property market, and it’s probably helping to stabilise prices this time around, but this isn’t solely the case anymore. China’s property market is still undergoing a severe correction and equites were seen as the less risky option, driven by the naive belief that Beijing will do whatever it takes to sustain the rally. This domestic reallocation of assets represents a major shift in the fundamental structure of the world’s second largest economy; hence the massive gains in equity markets (volumes are at an all-time high).

A rapid rise in an equity index is always going to raise a few alarm bells, and this is especially true for rallies that are fuelled by margin lending, as is the case for Chinese equity markets this year. The PBoC’s easing cycle is accompanied by the belief that Beijing will do whatever it takes to sustain the bull market, resulting in the massive leverage-driven surge into equity markets. This has pushed indices above what many believe is their true fundamental value – at once stage the ChiNext Index was at 70 times earnings. Even with the recent sell-offs, the ChiNext and Shenzhen Composite indices are around 50 and 30 times earnings, which is dangerously high; the Shanghai Composite is relatively cheap at around 15 times earnings.

Given this shaky support, it’s not surprising that it didn’t take much to trigger a full-blown rush for the exit, and a collapse in global risk appetite as Grexit fears mounted greased the floors. Even the PBoC only had limited success in mitigating the damage; the bank recently lobbed 25 basis points off its one-year lending rate – it is its fourth such cut since November 2014 – and cut its RRR by 50 basis points, bringing the former to its lowest ever level. It was the first time the central bank loosened both of China’s main policy rates since the depths of the global financial crisis. The double-cut was aimed at restoring investor confidence in both the economy and equity markets, but it’s clearly not working.

Even if the global marketplace regains its appetite for risk, it’s unlikely we’ll see a return to the conditions experienced early in the year as investors are going to be wary of being stung yet again. In saying that, a complete collapse of the aforementioned Chinese equity markets is unlikely as long as the PBoC keeps loosening monetary policy, which we think it will in the medium-term to boost confidence (it has a lot of room to loosen monetary policy, even with the one-year lending rate at an historical low). It’s more likely that we may see a slow, cautious grind higher over the long-term, with intermitted periods of extreme volatility, especially for the tech-heavy Shenzhen and ChiNext markets. A safer option may be the MSCI China index as it is still much cheaper than its counterparts in China due to an appetite for A-listed shares (shares of Chinese companies listed on mainland indices), making it more durable.

China’s equity markets are more volatile at the moment than other markets in Asia, largely because they are either dominated by retail investors or naturally volatile technology stocks. This means that investors in other parts of Asia can, and have for that matter, largely taken what’s happening in mainland China with a grain of salt. However, if the sell-off were to continue and reach a crisis point for China, it would likely be bad news for equity markets throughout the region, especially for export dominated countries like Australia and New Zealand.