China will release its official manufacturing PMI data for Aug compiled by the National Bureau of Statistics on this Sat, 31 Aug at 0100 GMT.

Even thought, most market participants monitor the private Caixin Markit manufacturing PMI (out on Mon, 02 Sep @0145 GMT) as it consists of data surveyed from smaller privately-owned corporates that gives a better gauge on the overall health of the manufacturing sector versus the official one that consists of data from bigger corporations, mostly from state-owned enterprises (SOEs)

Nevertheless, it is still worthwhile to pay attention to the official PMI as the manufacturing activities of the SOEs has started to see 2 consecutive months of contraction below the 50 level; (49.4 in Jun) and (49.7 in Jul) which do not bode well on the health of China economy and the rest of the world. Also, given the on-going trade tension between U.S and China, it will be important to see how such uncertainties impact the manufacturing sector (SOEs) which in turn dictate fiscal and monetary policies from the central government to counter any slowdown.

For the upcoming official manufacturing PMI data for Aug, consensus is set at 49.7, a similar level to the actual data recorded in Jul.

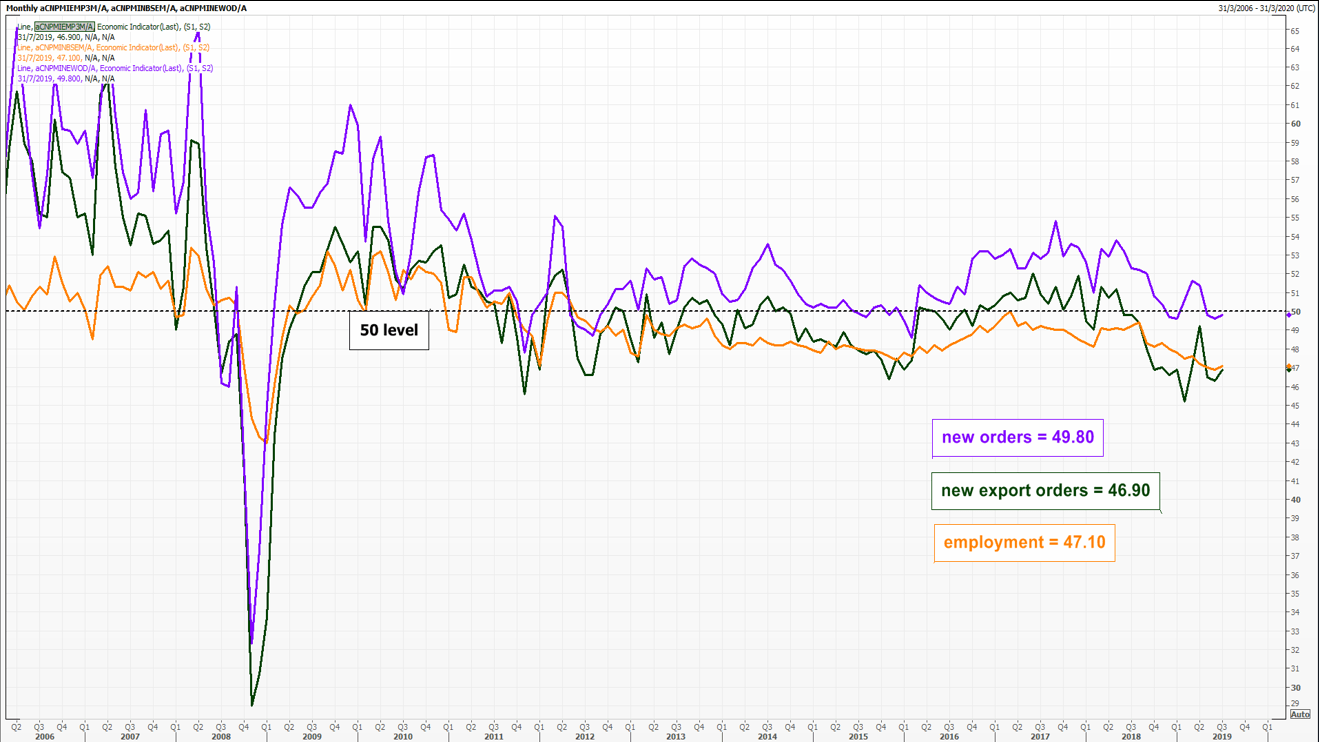

Now, let us look at the breakdown of the various components inside the manufacturing PMI (new orders, new export orders & employment).

China Official Manufacturing PMI Components Breakdown as at Jul 2019

click to enlarge chart

- Employment and new export orders have led the decline.

- Employment has started to contract (below 50) since Apr 2017 and the last data recorded in Jul stood at 47.10 which is at a 7-year low.

- New export orders have contracted since Jun 2018 and the last data recorded in Jul stood at 46.90, a slight improvement from 45.20 (7-year low) seen in Feb 2019.

Therefore, it is paramount to monitor the latest data on employment and new export orders components of the official manufacturing PMI data to have a leading gauge on the health of the manufacturing sector (SOEs).

My colleague has written an article on “The Week Ahead” which has highlighted the various assets that can have a significant movement around the data’s release (click here to read).

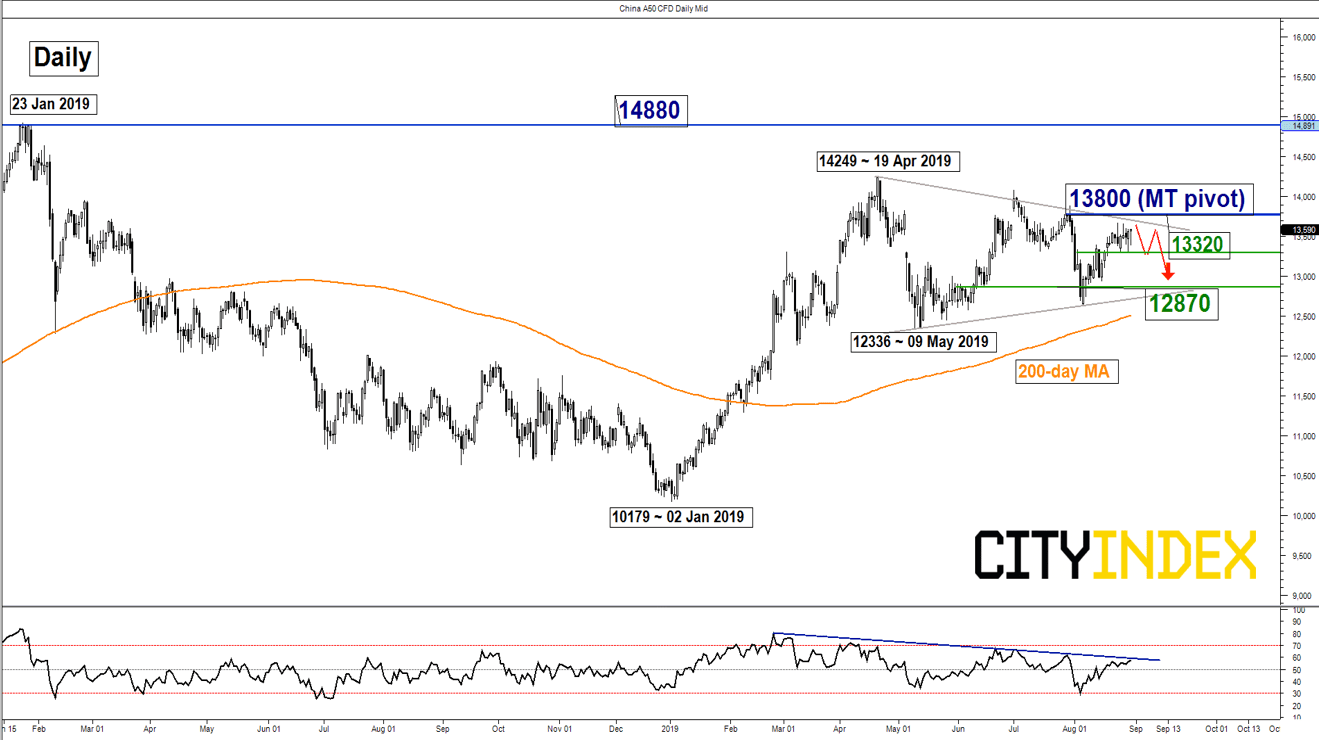

Let’s us now look at the chart of the China A50, one of the assets.

Medium-term technical analysis on China A50

click to enlarge chart

- Since 19 Apr 2019 high of 14249, the China A50 has been evolving within a “Symmetrical Triangle” range configuration.

- The current up move of 8% from its 06 Aug 2019 low of 12637 is now coming close to the upper limit of the “Symmetrical Triangle” at 13800 coupled with the daily RSI right below a corresponding resistance at the 60 level.

- Elliot Wave/fractal analysis suggest a potential downleg sequence to retest the “Symmetrical Triangle” range support at 12870 (also the 76.4% retracement of the recent up move from 06 Aug low to 23 Aug 2019 high & the 200-day Moving Average).

- If the 13800 key medium-term pivotal resistance is not surpassed and a break below 13320 is likely to reinforce a push down to target 12870 next.

- On the other hand, a clearance with a daily close above 13800 invalidates the bearish range scenario for a breakout to retest the major resistance of 14880 (swing high areas of Jun 2015/Jan 2018).

Charts are from Refinitiv & City Index Advantage TraderPro

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM