Markets may need to scale yuan risk back up in a hurry

PBOC governor Yi Gang's comments about the yuan are the first pointer from a senior official that Beijing could soon tolerate yuan depreciation beyond typical bounds. Yi spoke broadly, in a Friday TV interview, about the tools at his disposal. He noted “tremendous” room to adjust interest rates, the required reserve ratio and other monetary and fiscal measures if warranted by further trade war deterioration that could hurt the economy.

But foreign exchange participants particularly flagged his comments on the yuan. He dismissed the idea of a line in the sand, widely thought to be ¥7 to the dollar. The rate hasn’t crossed that level for over a decade. Yi said there is no particular number more important than another. Unfortunately, that view contradicts the years of work officials have put in to establish ¥7 as a number with consequences. Those messages explain why the offshore rate reacted with a fall of as much as 0.5% against the dollar on Friday, the most since mid-May, hitting a seven-month low. Onshore, the spot hit ¥6.9171, the highest since 29th May, marking the 14th session out of fifteen when it has been weaker than ¥6.90.

The widely speculated aim of tacit depreciation would be to provide a buffer against rising economic headwinds as new tariffs bite. But as demonstrated by the upsurge of volatility following August 2015’s devaluation, market destabilisation could be the side effect. Now, fear of volatility itself can bring it on. So if the yuan falls below ¥7 a rise in cross-asset volatility is still likely. It would probably hit Chinese shares first whilst echoing around closely tied emerging market FX, which threatened to blow-up for similar reasons last year. The rand broke 15 against the dollar on Thursday for the first time since October, warning of a return to fragility that could worsen if stronger currencies tied by trading relationships slide.

Depreciation is also another incendiary issue with Washington. U.S. officials have repeatedly demanded that an agreement against competitive devaluations be included in any trade deal. Just last week, the White House again skirted dubbing China a ‘currency manipulator’. It’s notable that Yi will meet Treasury Secretary Steven Mnuchin this weekend, ahead of the G-20 summit in Japan which might include a face-to-face between presidents Trump an Xi. So the governor’s yuan talk can’t be seen as entirely neutral. And with the U.S. possibly going ahead with tariffs on Mexico next week, markets, which have priced out some risks towards the end of the week, may have to factor them back in quickly. A sliding yuan could have particularly bad timing.

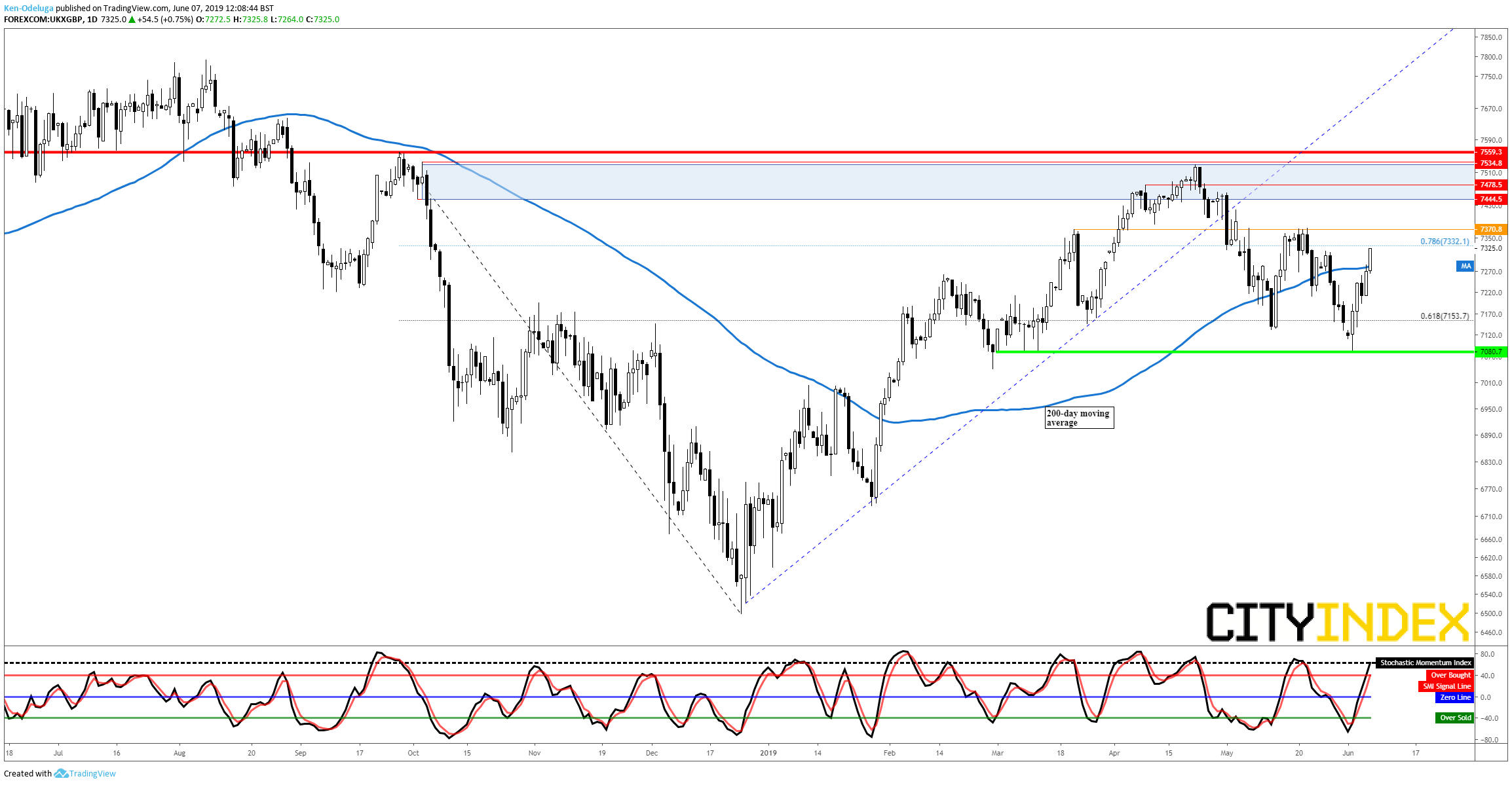

Chart thoughts

The China-sensitive FTSE 100 has put in a fair recovery bid this week. It’s in step with global markets backing off worst-case scenarios, with help from policy signals. Friday’s advance has seen the equivalent UK 100 CFD cross its important 200-day moving average, the threshold over which markets will probably trend higher or lower. It’s early days. UK 100 must now pull clean away to prove it has strengthened. Like all global indices, it’s still negotiating traces of the autumn-winter collapse. The 78.6% Fibonacci (around 7330)—already corroborated as sensitive—is just overhead. Higher still, the 7444-7535 region of 2019 peaks is also a proven resistance zone. It echoes tops in late September and October that presaged the violent correction. The yuan’s approach to ¥7 should flash warnings the FTSE can’t ignore.

Price chart: UK 100 CFD – daily [07/06/2019 12:08:59]

Source: Tradingview/Forex.com

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM