Charting Apple vs the Rest

On March 16 of last year, Apple’s successful release of its iPad 3 dominated the markets as the firm powered further as the world’s most valuable […]

On March 16 of last year, Apple’s successful release of its iPad 3 dominated the markets as the firm powered further as the world’s most valuable […]

On March 16 of last year, Apple’s successful release of its iPad 3 dominated the markets as the firm powered further as the world’s most valuable company.

In March 14 of this year, Apple sits on the sideline, watching Samsung release its successful Galaxy S4.

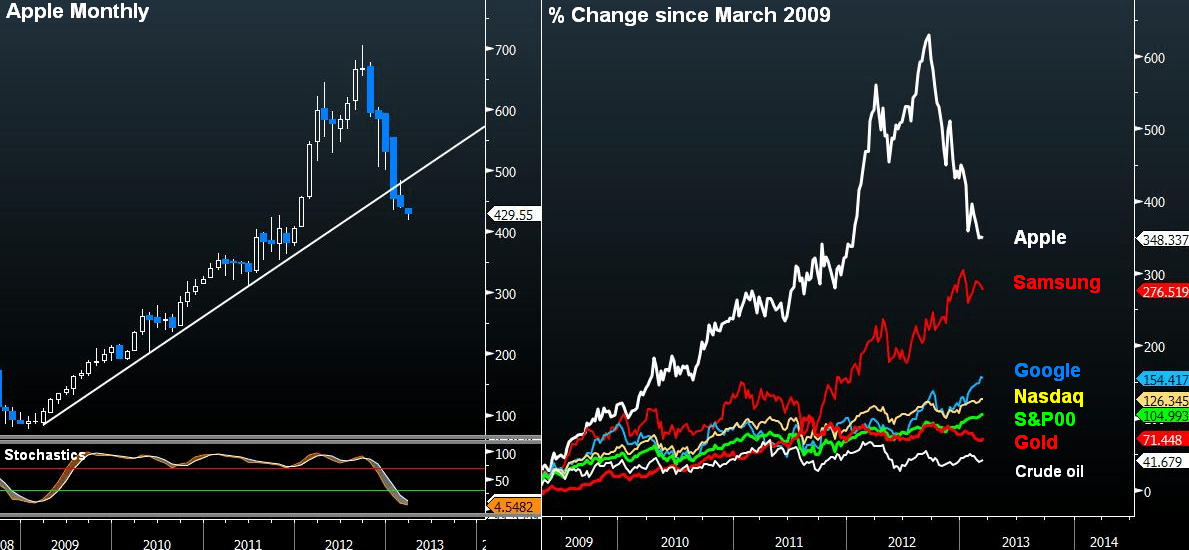

Apple’s share is down 39% from its September high, posting six consecutive monthly declines. Its fundamental woes began surfacing amid worries of insufficient supply of iPhone 5 and iPad, overlapping with reports of slowing demand.

This week’s rumours of cuts in orders have also weighed on the price. But the main fundamental challenge remains competition. While Apple lacks new products, Samsung continues to overcome criticism of lacking innovation by halving the product cycle of its Galaxy S series to 12 months.

Product releases aside, Apple will now have to resort to impacting the stock price via paying their shareholders. Last year’s announcement to return $45 billion in cash over three years may no longer be enough. It may have to give an additional $45bn in the form of dividends and stock buy-backs. The next boost to Apple’s stock price may by combining cash distribution with snappy upgrades to its iPhone and/or iPad mini.

Apple has clearly broken below its four-year trendline. A rally back to 450-460s may seem inevitable, but the key remains whether we’ll see a rebound above the 100-week moving average near 470s. As it stands the weekly and monthly stochastic suggest prolonged consolidation between $400 and $450, before a renewed wave of selling tests the $350 territory. A break above $475 is not expected anytime soon.